#business accounting Assignment

Text

Are you in a quandary over your business accounting assignments? Fear not, for I have embarked on a quest to unveil the crème de la crème of online resources tailored to assist you in conquering your accounting challenges. From the intricacies of balance sheets to the complexities of financial statements, these platforms offer a beacon of light in the often murky waters of business accounting.

Do My Accounting Assignment - (https://www.domyaccountingassignment.com/) Need someone to do your business accounting assignment for you? Look no further! Do My Accounting Assignment boasts a team of adept professionals ready to tackle your tasks with precision and expertise. With a commitment to quality and timely delivery, they ensure your academic success is never compromised.

Accounting Assignment Help - (https://www.accountingassignmenthelp.com/business-accounting-assignment-help/) Struggling with business accounting concepts? Accounting Assignment Help is your trusted companion in navigating through the labyrinth of financial jargon. Their comprehensive assistance covers everything from cost accounting to financial analysis, guaranteeing stellar grades every time.

Accounting Assignment Helper - (https://www.accountingassignmenthelper.com/) When the intricacies of business accounting leave you perplexed, turn to Accounting Assignment Helper for clarity and guidance. Their team of seasoned experts is dedicated to unraveling the mysteries of accounting, ensuring your assignments are executed with precision and finesse.

Edu Assignment Help - (https://www.eduassignmenthelp.com/) Edu Assignment Help is your one-stop destination for all your academic needs, including business accounting assignments. With a focus on excellence and customer satisfaction, they strive to alleviate your academic burdens, allowing you to excel in your studies effortlessly.

Assignment Pedia - (https://www.assignmentpedia.com/accounting-assignment-help.html) Unlock the secrets of business accounting with Assignment Pedia's unparalleled assistance. Whether it's financial reporting or managerial accounting, their team of experts is equipped to tackle any challenge head-on, ensuring your assignments are nothing short of exemplary.

Live Exam Helper - (https://www.liveexamhelper.com/take-my-accounting-exam.html) Need assistance with your accounting exams? Live Exam Helper offers comprehensive support to ensure you're well-prepared and confident on exam day. From practice questions to exam tips, they've got you covered every step of the way.

Take My Class Course - (https://www.takemyclasscourse.com/take-my-online-accounting-class/) Overwhelmed by your online accounting class? Take My Class Course provides expert assistance to help you navigate through the course material with ease. With their guidance, acing your business accounting assignments has never been more attainable.

Quora Quora serves as a treasure trove of knowledge, where experts and enthusiasts alike share insights and advice on various topics, including business accounting. Engage with the community to glean valuable tips and tricks to excel in your assignments.

Reddit Reddit, the front page of the internet, harbors a plethora of resources and communities dedicated to accounting and academics. Dive into subreddits like r/Accounting or r/HomeworkHelp to seek guidance and support from fellow students and professionals alike.

In conclusion, navigating the realm of business accounting assignments may seem daunting at first, but with the right assistance, success is well within reach. Whether you seek professional help or community support, these top-notch websites are sure to propel you towards academic excellence. So, the next time you find yourself uttering, "Who Can Do My business accounting Assignment for Me," remember, help is just a click away!

#education#pay to do assignment#college#domyaccountingassignment#accounting#domyaccountingassignmentforme#accountingtutor#accounts#Do My business accounting Assignment for Me#business accounting Assignment

0 notes

Text

Dear Tumblr users,

We are excited to offer an exclusive discount on our website Accounting Assignment Help just for you! As a token of our appreciation for your support, we are offering up to 20% discount on all accounting assignment help services.

Whether you need help with accounting homework, essays, dissertations, or any other academic project, our team of expert writers is ready to assist you. We guarantee high-quality work that is plagiarism-free and delivered on time.

To take advantage of this offer, simply use the promo code AccountingAH20 at checkout. Don't miss out on this amazing opportunity to get professional accounting assignment help at a discounted price!

Thank you for choosing Accounting Assignment Help.

Best regards,

Bill Smith

Expert at Accounting Assignment Helper.

#accounting homework help#accounting homework#financial accounting homework help#accounting homework solver#cost accounting homework help#accounting homework help online#help with accounting problems#financial accounting homework solutions#financial accounting homework#financial accounting help#accounting help for students#business accounting assignment#college accounting help#need accounting help#accounting assignment help#accounting assignment help online#managerial accounting homework answers

0 notes

Text

Navigating Depreciation Dilemmas: An Expert's Guide to Business Accounting Assignments with Practical Insights

Welcome to the world of business accounting, where precision and expertise are paramount. As a seasoned professional providing business accounting assignment help online, I understand the challenges students face in mastering complex concepts. In this blog, we delve into a frequently tested question that often perplexes students, offering not just answers but a comprehensive understanding. Let's unravel the intricacies of business accounting together.

Question:

Scenario: XYZ Corporation

XYZ Corporation, a manufacturing giant, recently acquired new machinery to streamline its production process. The machinery's cost is $200,000, with an estimated useful life of 10 years and no residual value. The management is torn between using the straight-line method or the double-declining balance method for depreciation. As an expert in business accounting, explain the implications of each method and recommend the most suitable approach for XYZ Corporation.

Answer:

Understanding the Depreciation Methods:

Straight-Line Method:

This method evenly distributes the cost of the asset over its useful life.

Formula: Annual Depreciation = (Cost - Residual Value) / Useful Life

Applying it to XYZ Corporation:

Annual Depreciation = ($200,000 - $0) / 10 = $20,000 per year

Advantages:

Simplicity and ease of calculation.

Stable and predictable expenses.

Limitations:

May not accurately reflect an asset's actual decline in value.

2. Double-Declining Balance Method:

This method accelerates depreciation, allocating higher expenses in the early years.

Formula: Annual Depreciation = (Book Value at Beginning of Year) × (2 / Useful Life)

Applying it to XYZ Corporation:

Year 1: $200,000 × (2 / 10) = $40,000

Year 2: ($200,000 - $40,000) × (2 / 10) = $32,000

And so on...

Advantages:

Aligns with an asset's actual decline in value.

Front-loads expenses, beneficial for tax purposes.

Limitations:

Complex calculations may pose challenges.

Results in fluctuating and less predictable expenses.

Recommendation for XYZ Corporation:

Considering XYZ Corporation's scenario, the choice between straight-line and double-declining balance methods depends on its financial goals. If stability and predictability are prioritized, the straight-line method is preferable. However, if the corporation seeks to maximize tax benefits and is comfortable with a more nuanced approach, the double-declining balance method may be more suitable.

In conclusion, mastering business accounting involves not just providing answers but understanding the rationale behind them. If you find yourself grappling with such scenarios, our business accounting assignment help online ensures that you not only submit correct solutions but also comprehend the underlying principles. Feel free to reach out for personalized assistance tailored to your academic needs.

#do my assignment#business accounting assignment help#help with assignments#expert guidance#student life#study tips

11 notes

·

View notes

Text

So far:

0.5/2 Discussion posts

3/8 chapters read

3/16 quizzes taken

2/2 short papers done

0.5/1 term papers to complete (5 page minimum)

0/1 study guides for finals

Due by Thursday

Still have to prep for book club tomorrow AND also finish my work-real-life-job-thing wherein actual living organisms depend on me to survive so . . . Someone plz bring me . . . All of the iced caramel coffee . . . And something for the residual tummy ache plz

#yes each chapter has two quizzes#plus extra practice assignments which are worth credits too but I’m just not putting them here because there are usually between 1 and 4#per chapter#askldjfalksjdfaiejfa#next quarter I’m taking soil science tho#so#also business law and accounting and drawing but we won’t think about that until after#this quarter is done#the only future planning I can consider#involves dirt#naturally

7 notes

·

View notes

Photo

Looking for the best Finance Assignment Writing Help?

AHEC provides high-quality Finance Assignment Help for you at affordable prices and we make assignments for every subject. Moreover, we provide our service in every country like Canada, UAE, USA, UK, Australia, and many more countries.

If you are stuck in your task you can contact us on the phone, via WhatsApp, or via Email or send us your first message. Contact details are given below.

We are available 24/7 to help you and to give our 💯%.

Visit here: www.ahecounselling.com

E-mail 📧:- [email protected]

Whatsapp number- +91 96641 82955

#finance#business#financeassignment#accounting#marketing#financetips#financestudents#accounts#students#student#college#university#mba#mbastudent#mbaassignment#collegelife#mbalife#assignment#assignmenthelp#assignments#essay#essaywriting#homework#thesis#dissertation#essayhelp#homeworkhelp#academichelp#studentlife#exam

2 notes

·

View notes

Text

love how i’m probably going to have to spend my entire fall break applying for internships. that is, if i make it through this week.

#have huge assignment due tomorrow (literally a whole ass news site in a class we have not been taught anything and they grade so harshly)#like functional can make an account and login and post articles and comment and shit from scratch using html css php and sql#none of which i had ever used before this class (they don't teach us)#i also have an exam tomorrow i haven't even thought about studying for yet (im gonna need to pull an all nighter fml im so exhausted already#also an exam wednesday (yom kippur) in a class where i am like over 3 weeks behind#a big programming assignment in the class i have an exam in tomorrow that's due friday that i cannot think about until after my exam thurs#not to mention my usual hw assignments in many classes#i did a really shitty job on my hw due this week/weekend#didn't try very hard on my hw due fri because i was so busy and then wanted to go to parties oops (that's not like me huh)#straight up didn't even submit my astrophysics hw due yesterday because i was just so exhausted so i was like fuck it#we get 2 drops i think#i need to do laundry but i don't have time. i have no clean clothes but i haven't had enough time at my apartment to do it#my apartment is such a mess#i need to clean before i leave for fall break on friday but idk if ill have time#i am so overwhelmed#there's absolutely no way ill be able to get even a fraction of all the stuff i need to get done this week done#my anxiety lowkey has not been super bad this weekend in the first time in so long#but at the same time idk if that's a good thing because im not as motivated to do work even tho i don't want to sh as much which is good

2 notes

·

View notes

Text

PůjčkaPlus CZ emerges as the beacon of financial relief. Offering swift and hassle-free loans, it stands as the perfect solution to bridge any monetary gap. Whether facing a sudden medical emergency, car repair, or any unforeseen cost, PůjčkaPlus CZ provides the necessary funds with minimal paperwork and rapid approval.🐘🐘

Instant approval finance features:apply now..🇨🇿🇨🇿

Read.. more..

#czech republic#czech#financial planning#financial#finance and accounting#income#business#financial freedom#finance assignment help#finance news

0 notes

Text

:(

#I have most of the headway done to do an interview with an influencer about their brand & product and now the assignment is a group task.#Fair fine sure. Won’t be able to use my work for this now since we’re doing it on LoL vs DotA but it’s still good to have I guess#It’s just now extra work on top of an essay on businesses and a presentation on goal setting and learning about LoL & DotA.#I’ve made a professional looking side to mimic when/if this account becomes relevant because I don’t think this would fly

1 note

·

View note

Text

Are you struggling with your business accounting assignments? Worry no more, because DoMyAccountingAssignment.com is here to provide you with unparalleled assistance to excel in your academic endeavors. Our team of experts is dedicated to ensuring your success by offering comprehensive business accounting assignment help tailored to your specific needs.

Mechanisms for handling disputes: We understand that disagreements may arise, and that's why we have clear mechanisms in place to address any disputes promptly and fairly. Your satisfaction is our priority, and we strive to resolve any issues amicably.

Compatibility with specific research methodologies: Our experts are well-versed in various research methodologies relevant to business accounting, ensuring that your assignments are crafted with precision and accuracy.

Process for addressing customer complaints: Transparency is key in our operations. We have a structured process for addressing customer complaints, ensuring that your concerns are heard and resolved satisfactorily.

Access to testimonials from repeat clients: Our track record speaks for itself. With glowing testimonials from our repeat clients, you can trust in the reliability and consistency of our services.

Review of academic writing standards: We go beyond just providing solutions; we empower you to enhance your academic writing skills with comprehensive guidance and resources tailored to your needs.

Expertise in specific types of assignments: Whether it's essays, research papers, or dissertations, our experts possess the expertise to tackle any type of business accounting assignment with finesse.

Handling of data analyses and interpretations: Data analysis is a crucial aspect of business accounting assignments. Our team can assist you in conducting thorough analyses and interpretations to elevate the quality of your work.

Partnership with academic professionals: We have forged partnerships with reputable academic professionals and institutions, ensuring that our services adhere to the highest standards of quality and integrity.

Handling of field-specific jargon: Business accounting comes with its own set of jargon and terminology. Rest assured, our experts are adept at handling these nuances to deliver assignments that meet the standards of your field.

In-depth consultations: Your satisfaction is our top priority. That's why we offer in-depth consultations to understand your requirements and expectations thoroughly, ensuring that the final deliverable exceeds your expectations.

With DoMyAccountingAssignment.com, you're not just getting assistance; you're investing in your academic success. Let us help you soar to new heights in your business accounting studies. Reach out to us today and experience the difference firsthand!

#education#pay to do assignment#college#domyaccountingassignment#homework help#accounting#domyaccountingassignmentforme#accountingtutor#accounts#business accounting

0 notes

Text

GAAP vs IFRS

Decoding US Accounting Rules: GAAP vs IFRS | Expert Insights in 2024

Navigate the GAAP vs IFRS debate in US Accounting effortlessly. Gain expert insights, make sense of regulations. Your guide to financial clarity.

The evolving landscape of accounting standards unfolds a nuanced debate between the Generally Accepted Accounting Principles and the International Financial Reporting Standards. These two frameworks, while sharing a common goal of transparent financial reporting, diverge in their approaches, giving rise to a multifaceted discourse with far-reaching implications for the financial world.

1. Introduction

The evolution of accounting standards has witnessed the crystallization of two dominant frameworks – General Accounting Accepted Principles and International Financial Reporting Standards. In the labyrinth of financial reporting, companies grapple with choosing between these standards, each with its unique history, principles, and global relevance. The debate surrounding GAAP vs IFRS is not a mere academic exercise but a pivotal consideration with implications for investment decisions, legal compliance, and the global financial landscape.

1.1. Evolution of Accounting Standards

The journey of accounting standards traces back to the aftermath of the 1929 stock market crash when the need for standardized, transparent financial reporting became glaringly apparent. What emerged were the General Accounting Accepted Principles, designed to restore investor confidence by providing a reliable framework for financial statements. Over time, GAAP has become deeply embedded in the U.S. financial system, shaping the way companies communicate their financial health.

On the global stage, the International Financial Reporting Standards evolved as a response to the growing interconnectedness of economies. The International Accounting Standards Board (IASB) took the reins in developing IFRS, aiming for a standardized global language of financial reporting. This set the stage for a two-pronged approach to financial reporting standards – General Accounting Accepted Principles dominating in the U.S. and International Financial Reporting Standards gaining traction internationally.

1.2. The Crucial Role of GAAP and IFRS

GAAP stands as the bedrock of accounting standards in the United States, overseen by the Financial Accounting Standards Board (FASB). Its principles, rooted in historical cost, revenue recognition, and matching, provide stability and a familiar structure for U.S. businesses. On the other hand, IFRS, under the stewardship of the IASB, operates as a global player, emphasizing fair value, substance over form, and materiality.

The significance of General Accounting Accepted Principles lies in its historical context and its alignment with the unique needs of the U.S. business environment. Its principles have served as a guiding light for American companies, offering a consistent framework for financial reporting. International Financial Reporting Standards, with its global perspective, caters to the interconnectedness of today’s businesses, providing a common language for multinational corporations.

1.3. Navigating the GAAP vs IFRS Dilemma

The choice between General Accounting Accepted Principles and International Financial Reporting Standards is not a one-size-fits-all decision. Companies grapple with a complex decision-making process, considering factors such as their geographical reach, industry nuances, and investor preferences. This debate is not isolated to boardrooms; it resonates in financial markets, legal proceedings, and regulatory landscapes, shaping the very fabric of financial reporting practices.

2. Understanding GAAP

2.1. The Foundation of GAAP

a. Historical Roots and Evolution

GAAP’s roots delve deep into the need for a standardized accounting framework post the 1929 stock market crash. FASB emerged as a response to the chaos that ensued, charged with the responsibility of establishing and improving financial accounting and reporting standards. The journey of GAAP has been one of continuous evolution, adapting to the changing business landscape and regulatory requirements.

b. FASB’s Ongoing Influence

The Financial Accounting Standards Board (FASB) stands as the guardian of GAAP, playing a pivotal role in setting and refining accounting standards. FASB’s mission goes beyond rule-making; it seeks to improve financial reporting, providing transparency and relevance in financial statements. The ongoing influence of FASB ensures that GAAP remains adaptive and responsive to the dynamic nature of business transactions.

2.2. Core Principles Anchoring GAAP

a. Embracing the Historical Cost Principle

One of the cornerstones of GAAP is the historical cost principle, dictating that assets should be recorded at their original cost. This principle provides stability and reliability in financial statements, allowing users to assess the financial health of a company based on the actual cost of its assets at the time of acquisition. While critics argue that this approach may not reflect current market values, proponents emphasize the prudence and consistency it offers.

b. Revenue Recognition as a Cornerstone

GAAP’s approach to revenue recognition centers on the realization and earned criteria. Revenue is recognized when it is realized or realizable and earned. This conservative approach ensures that revenue is not prematurely recognized, aligning with the matching principle. While this method may defer recognizing revenue until later stages in the sales cycle, it safeguards against potential overstatement and presents a cautious picture to investors.

c. The Significance of the Matching Principle

The matching principle is a guiding force in GAAP, emphasizing the alignment of expenses with the revenue they generate. This principle ensures that the costs associated with generating revenue are recognized in the same period as the revenue itself, presenting a more accurate portrayal of a company’s profitability. While adhering to the matching principle might result in lower reported profits during high-revenue periods, it provides a more realistic long-term view.

2.3. Scrutinizing Criticisms and Recognizing Limitations

a. Rigidity vs. Stability

One common criticism leveled against GAAP is its perceived rigidity, particularly regarding the historical cost principle. Critics argue that this approach may not capture the true economic value of assets, especially in industries with rapidly changing market conditions. However, proponents assert that this rigidity provides stability and consistency, allowing for easier comparison across periods and industries.

b. The Balancing Act of Revenue Recognition

The conservative approach to revenue recognition in GAAP has faced scrutiny for potentially understating a company’s immediate financial performance. Critics argue that this caution may not be reflective of a company’s true economic position, especially in industries where revenue realization is instantaneous. However, the balancing act lies in mitigating the risk of premature revenue recognition, ensuring financial statements maintain integrity and accuracy.

c. Challenges in Adhering to the Matching Principle

While the matching principle aligns expenses with revenue, critics contend that it introduces complexities in determining the direct association between costs and specific revenue streams. This challenge becomes more pronounced in industries with diverse revenue sources. Despite these challenges, adhering to the matching principle remains integral in presenting a holistic view of a company’s financial health, helping investors make informed decisions.

3. Embracing IFRS

3.1. IFRS: A Global Framework

a. The Rise of International Financial Reporting Standards

The emergence of IFRS marks a significant shift towards a globalized approach to financial reporting. As businesses expanded internationally, the need for a common accounting language became evident. IFRS, under the stewardship of the International Accounting Standards Board (IASB), rose to prominence as a framework that transcends borders, providing a standardized set of principles for companies operating on the world stage.

b. IASB’s Pivotal Role in Shaping IFRS

The International Accounting Standards Board (IASB) shoulders the responsibility of developing and maintaining IFRS. Unlike GAAP, IFRS operates under a principles-based approach, focusing on broad principles rather than detailed rules. This flexibility allows for easier adaptation to diverse business environments, making IFRS an attractive choice for multinational corporations seeking a harmonized approach to financial reporting.

3.2. Unpacking Core Principles of IFRS

a. Fair Value Measurement: A Paradigm Shift

One of the fundamental differences between GAAP and IFRS lies in the approach to asset valuation. While GAAP predominantly adheres to the historical cost principle, IFRS leans towards fair value measurement. Fair value reflects the current market value of assets, providing a more dynamic and responsive perspective. Critics argue that fair value introduces volatility, but proponents emphasize its relevance in capturing real-time economic conditions.

b. Substance Over Form: Emphasizing Economic Reality

In IFRS, the substance of transactions takes precedence over their legal form. This principle ensures that financial statements reflect the economic reality of transactions, promoting transparency and accuracy. While this approach aligns with the overarching goal of providing relevant information to users, it requires careful judgment and interpretation, potentially introducing subjectivity in financial reporting.

c. Materiality’s Role in Flexibility

IFRS introduces greater flexibility in materiality judgments compared to GAAP. Materiality refers to the threshold at which information becomes relevant to users. The more flexible stance in IFRS allows entities to exercise judgment in determining what information is material, considering both quantitative and qualitative factors. This flexibility, while enhancing the adaptability of IFRS, also raises concerns about potential inconsistencies in financial reporting.

3.3. Weighing Advantages and Drawbacks

a. IFRS Flexibility: A Double-Edged Sword

The flexibility embedded in IFRS is both its strength and weakness. Proponents argue that this adaptability makes IFRS suitable for diverse business environments, allowing for easier integration with various industries and legal systems. However, critics contend that this very flexibility can lead to inconsistencies and a lack of comparability, challenging the reliability of financial statements for investors and stakeholders.

b. Global Appeal vs. Application Challenges

The global nature of IFRS makes it an attractive choice for multinational companies aiming for consistency in financial reporting across borders. The common language of IFRS facilitates international transactions and fosters a seamless global financial landscape. However, the application of IFRS can pose challenges in jurisdictions with varying legal and regulatory frameworks, potentially leading to complexities in implementation and interpretation.

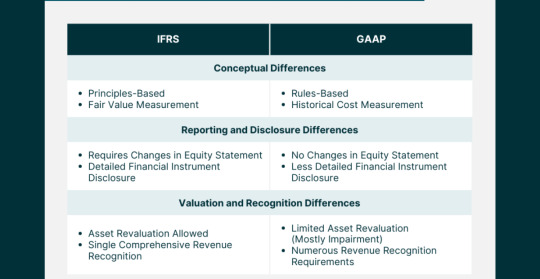

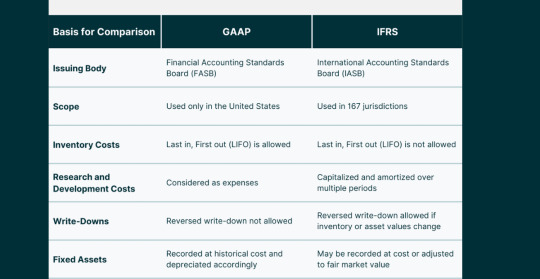

4. Key Differences Between GAAP and IFRS

4.1. Delving into Variances

a. Revenue Recognition: The GAAP-IFRS Divergence

One of the pivotal differences between GAAP and IFRS lies in the recognition of revenue. While both frameworks aim to depict the economic reality of transactions, their approaches diverge in certain key aspects. GAAP tends to be more prescriptive, providing specific guidelines for various industries, whereas IFRS adopts a broader principles-based approach, allowing entities more room for interpretation.

b. Inventory Valuation: Differing Approaches

The treatment of inventory valuation varies significantly between GAAP and IFRS. GAAP typically follows a specific set of rules for valuing inventory, such as the Last In, First Out (LIFO) or First In, First Out (FIFO) methods. In contrast, IFRS permits the use of various methods, including FIFO and weighted average, offering companies more flexibility in choosing an approach that aligns with their specific business dynamics

c. Consolidation Methods: Navigating Complexity

Consolidation methods, particularly in the context of subsidiaries and investments, showcase differences between GAAP and IFRS. GAAP often employs a more rule-based approach, specifying conditions for consolidation. In contrast, IFRS focuses on a principles-based approach, considering the substance of relationships rather than relying on rigid criteria. This variance introduces nuances in financial reporting, influencing how companies present their financial position and performance.

4.2. The Impact on Financial Statements

a. Shaping Investor Perception

The differences in revenue recognition, inventory valuation, and consolidation methods contribute to variations in financial statements produced under GAAP and IFRS. Investors, as key stakeholders, must navigate these differences to gain an accurate understanding of a company’s financial health. The choice between GAAP and IFRS significantly shapes investor perception, influencing investment decisions and risk assessments.

b. Decision-Making Dynamics

Companies, in choosing between GAAP and IFRS, must consider the implications on decision-making dynamics. The framework adopted affects how financial information is presented, potentially influencing strategic decisions, mergers and acquisitions, and capital-raising activities. Understanding the impact of these frameworks on decision-making is crucial for entities operating in dynamic and competitive business environments.

4.3. Global Adoption Trends: A Comparative Analysis

The adoption trends of GAAP and IFRS provide insights into the global dynamics of financial reporting standards. While GAAP maintains dominance within the United States, IFRS has gained traction in numerous jurisdictions worldwide. Understanding the factors influencing these trends, such as regulatory requirements, investor preferences, and global market integration, sheds light on the evolving landscape of accounting standards.

“Accounting isn’t just about profits and losses; it’s about sculpting the financial soul of a company.” Michael Johnson

5. The Evolution of Accounting Standards

5.1. GAAP’s Historical Odyssey

a. Post-1929: A Catalyst for Change

The stock market crash of 1929 served as a catalyst for rethinking the approach to financial reporting. The chaos that ensued prompted the establishment of standardized accounting principles, laying the foundation for what would later become GAAP. The primary goal was to restore investor confidence by providing a reliable framework for financial statements, reducing uncertainty and fostering stability in financial markets.

b. Amendments and Updates: Shaping GAAP’s Trajectory

GAAP’s journey has not been static; it has evolved through amendments and updates to address emerging challenges and align with changing business dynamics. The Financial Accounting Standards Board (FASB) plays a pivotal role in shaping GAAP, ensuring that it remains relevant, transparent, and responsive to the needs of companies and investors. The ongoing commitment to refinement reflects a dedication to maintaining the integrity of financial reporting.

5.2. Internationalization Efforts

a. Pioneering Attempts at Global Standardization

As globalization gained momentum, so did the recognition of the need for global accounting standards. Efforts were made to align U.S. GAAP with international standards, but achieving a universal standard proved challenging. The push for global standardization gained traction with the rise of IFRS, offering a framework that transcends national boundaries and facilitates consistency in financial reporting for multinational corporations.

b. The Challenge of Aligning U.S. Standards Globally

While the concept of global accounting standards gained support, aligning U.S. GAAP with international standards presented formidable challenges. The unique legal, regulatory, and cultural landscape in the United States posed hurdles to seamless integration. Despite these challenges, the pursuit of convergence and harmonization continued, reflecting the recognition of the interconnectedness of global economies.

5.3. Convergence Initiatives

a. The Ongoing Pursuit of Harmonization

Convergence initiatives aimed at harmonizing GAAP and IFRS gained prominence in the early 21st century. The objective was to reduce disparities between the two frameworks, fostering a more standardized global approach to financial reporting. While full convergence remained elusive, progress was made in aligning specific standards, reflecting a commitment to minimizing inconsistencies and facilitating ease of comparison for investors and stakeholders.

b. Prospects and Hurdles in a Unified Global Standard

The prospects of a unified global accounting standard remain a tantalizing goal, promising enhanced comparability and consistency in financial reporting. However, hurdles such as divergent national interests, legal complexities, and varying levels of standard-setting infrastructure continue to challenge the realization of this vision. Navigating these obstacles requires ongoing collaboration and a commitment to the overarching goal of global financial transparency.

6. Regulatory Bodies Influencing GAAP

6.1. FASB’s Pivotal Role

a. GAAP’s Guardian: The FASB Mandate

The Financial Accounting Standards Board (FASB) stands as the guardian of GAAP, wielding influence over the development and refinement of accounting standards. FASB’s mandate goes beyond rule-making; it encompasses a commitment to improving financial reporting, ensuring that standards are not only relevant but also responsive to the evolving needs of businesses and investors.

b. FASB’s Mission in Financial Reporting Improvement

FASB’s mission revolves around the improvement of financial reporting through the development of high-quality accounting standards. The board operates under a due process system, seeking input from various stakeholders, including investors, auditors, and preparers of financial statements. This collaborative approach ensures that GAAP remains a robust and adaptive framework that reflects the intricacies of modern business transactions.

6.2. SEC’s Watchful Eye

a. SEC’s Authority in Recognizing GAAP Standards

The Securities and Exchange Commission (SEC) plays a crucial role in the oversight of financial reporting in the United States. While the FASB sets accounting standards, the SEC has the authority to recognize and prescribe the principles used in the preparation of financial statements for publicly traded companies. This dual-layered system ensures a balance between industry expertise and regulatory oversight in shaping GAAP.

b. SEC’s Contributions to Financial Transparency

The SEC’s contributions to financial transparency extend beyond its recognition of GAAP standards. The commission actively engages in rule-making and enforcement to ensure that companies adhere to accounting principles and provide accurate and timely financial information to investors. The synergy between the SEC and FASB reinforces the integrity of financial reporting in the U.S. capital markets.

6.3. AICPA’s Industry Impact

a. AICPA: Nurturing Professional Standards

The American Institute of Certified Public Accountants (AICPA) plays a vital role in shaping professional standards within the accounting industry. While not directly involved in setting GAAP, the AICPA contributes to the development of ethical and professional standards that guide the conduct of accountants. This commitment to excellence enhances the credibility of financial reporting, reinforcing the trust that stakeholders place in GAAP.

b. Industry-Wide Compliance through AICPA Guidance

The AICPA’s influence extends beyond standards development to encompass industry-wide compliance. The organization provides guidance on best practices, ethical considerations, and emerging issues within the accounting profession. This guidance ensures a cohesive and ethical approach to financial reporting, aligning with the principles embedded in GAAP and contributing to the overall reliability of financial statements.

7. International Bodies Shaping IFRS

7.1. IASB’s Global Mandate

a. IASB’s Significance in IFRS Development

The International Accounting Standards Board (IASB) holds a central role in the development and maintenance of IFRS. Unlike the FASB’s role in the U.S., the IASB operates on a global scale, aiming to set accounting standards that are applicable and relevant to entities worldwide. The IASB’s commitment to a principles-based approach reflects its recognition of the diverse needs of global businesses.

b. A Global Perspective in Standard Setting

The IASB’s global perspective is intrinsic to its standard-setting process. The board considers input from various regions, industries, and stakeholders, ensuring that IFRS reflects the nuances of international business. The principles-based approach allows for adaptability, catering to the diverse legal, economic, and cultural landscapes in which entities operate globally.

7.2. IFRIC’s Interpretative Role

a. Navigating Grey Areas: IFRIC’s Guidance

The International Financial Reporting Interpretations Committee (IFRIC) plays a crucial role in navigating interpretative challenges within IFRS. Given the principles-based nature of IFRS, grey areas may arise, requiring clarification and guidance. IFRIC addresses these challenges by providing interpretations and guidance, ensuring consistent application of IFRS standards across diverse industries and jurisdictions.

b. Consistent Application of IFRS Standards

Consistency in the application of IFRS standards is paramount to ensuring comparability and reliability in financial reporting. IFRIC’s interpretative role contributes to this objective by offering guidance on ambiguous or complex issues. This commitment to clarity and consistency aligns with the overarching goal of IFRS – to provide a common language for financial reporting that transcends geographical and industry-specific boundaries.

7.3. Monitoring Board’s Oversight

a. Ensuring Independence in Standard Setting

The Monitoring Board plays a crucial oversight role in ensuring the independence and effectiveness of the IFRS Foundation, which houses the IASB. Independence is a cornerstone of credible standard-setting, and the Monitoring Board’s role is to safeguard the integrity of the standard-setting process. This commitment to independence reinforces the trust that global stakeholders place in IFRS as a reliable and unbiased framework.

b. The Role of the Monitoring Board in IFRS Integrity

The Monitoring Board’s vigilance extends beyond independence to the broader integrity of the IFRS framework. By overseeing the activities of the IFRS Foundation and IASB, the Monitoring Board contributes to the credibility of IFRS as a global accounting standard. This oversight ensures that IFRS continues to meet the evolving needs of global financial markets and remains a trusted framework for transparent financial reporting.

8. Impact on Financial Reporting

8.1. Side-by-Side Comparison

a. Financial Statement Variances: GAAP vs IFRS

A side-by-side comparison of financial statements prepared under GAAP and IFRS reveals variances arising from differences in principles, approaches, and interpretations. These variances extend to revenue recognition, asset valuation, and consolidation methods, influencing the reported financial position and performance of entities. Investors and analysts must navigate these differences to glean accurate insights into a company’s financial health.

b. Interpretation Challenges for Investors

Investors face interpretation challenges when analyzing financial statements prepared under different frameworks. Understanding the nuances of GAAP and IFRS differences is crucial for making informed investment decisions. The ability to discern how specific accounting choices impact financial metrics empowers investors to evaluate risks, assess potential returns, and navigate the complexities of the global investment landscape.

8.2. Revenue Recognition Dynamics

a. The Nuances of Revenue Recognition

The nuances of revenue recognition under GAAP and IFRS reflect the underlying philosophies of each framework. GAAP, with its prescriptive guidelines, provides specific criteria for recognizing revenue in various industries. In contrast, IFRS adopts a broader approach, emphasizing the substance of transactions over rigid rules. Navigating these nuances requires a deep understanding of industry dynamics and the specific requirements of each framework.

b. Implications for Investor Decision-Making

The implications of revenue recognition dynamics extend to investor decision-making. Differences in when and how revenue is recognized can influence perceptions of a company’s immediate financial performance. Investors must factor in these nuances to make informed decisions, considering the impact on key financial metrics such as earnings per share, profit margins, and return on investment.

8.3. Asset Valuation Approaches

a. Valuation Philosophies: Fair Value vs. Historical Cost

The variance in asset valuation philosophies between GAAP and IFRS introduces complexities in financial reporting. GAAP’s adherence to historical cost provides stability and consistency, albeit potentially understating the current market value of assets. In contrast, IFRS’s emphasis on fair value introduces a more dynamic and responsive approach to asset valuation. Companies must navigate the trade-offs between stability and accuracy in presenting their financial position.

b. Balancing Accuracy and Stability in Asset Reporting

Balancing accuracy and stability in asset reporting requires careful consideration of the trade-offs between fair value and historical cost. Companies must weigh the benefits of presenting current market values against the potential volatility introduced by fair value measurements. Striking the right balance ensures that financial statements accurately reflect the economic reality of a company’s assets while providing stakeholders with a stable and reliable foundation for decision-making.

9. Challenges in Adoption

9.1. Corporate Resistance Factors

a. Unpacking Corporate Hesitations

The decision to adopt new accounting standards, whether transitioning from GAAP to IFRS or vice versa, is met with corporate hesitations. Companies fear the potential disruptions, costs, and uncertainties associated with the transition. Understanding these resistance factors is essential for regulatory bodies, standard-setters, and industry stakeholders to develop strategies that facilitate smoother adoptions and ensure widespread compliance.

b. Overcoming Corporate Resistance Challenges

Overcoming corporate resistance challenges requires a multi-faceted approach. Clear communication on the benefits of the new standards, comprehensive training programs, and support mechanisms can alleviate concerns. Regulators and standard-setters must collaborate with industry representatives to address specific challenges faced by different sectors, fostering a cooperative environment conducive to successful adoptions.

9.2. Implementation Costs

a. Financial and Operational Impacts

The implementation of new accounting standards incurs financial and operational impacts for companies. Costs associated with staff training, system upgrades, and adjustments to internal processes contribute to the overall financial burden. Companies must carefully assess these costs and develop comprehensive implementation plans to mitigate disruptions and ensure a seamless transition to the new standards.

b. Strategies for Mitigating Implementation Costs

Strategies for mitigating implementation costs involve proactive planning, phased adoption approaches, and leveraging technology. Companies can benefit from engaging with industry peers that have successfully navigated similar transitions, learning from best practices and challenges. Collaboration between standard-setters, regulatory bodies, and industry associations plays a crucial role in developing strategies that balance the need for improved standards with the practicalities of implementation.

9.3. Training and Skill Gaps

a. The Need for Specialized Training

The adoption of new accounting standards introduces the need for specialized training to ensure that professionals possess the skills required for compliance. Training programs must address the nuances of the new standards, focusing on changes in accounting principles, reporting requirements, and the application of new methodologies. Bridging skill gaps is crucial for maintaining the integrity and accuracy of financial reporting.

b. Collaborative Approaches to Skill Development

Collaborative approaches to skill development involve partnerships between educational institutions, professional organizations, and industry players. The goal is to create comprehensive training programs that equip professionals with the knowledge and skills necessary for successful compliance. Standard-setters and regulators can play a pivotal role in promoting and endorsing such collaborative initiatives, fostering a culture of continuous learning within the accounting profession.

10. Legal Implications for Corporations

10.1. Legal Challenges in GAAP Compliance

a. Litigation Risks in GAAP Adherence

The legal challenges associated with GAAP compliance include litigation risks arising from alleged non-compliance. Companies adhering to GAAP must navigate the complexities of the legal landscape, ensuring that their financial statements withstand scrutiny. Implementing robust internal controls, engaging in transparent communication, and staying abreast of legal developments are essential strategies for mitigating litigation risks.

b. Strategies for Legal Compliance in GAAP

Strategies for legal compliance in GAAP involve proactive measures to minimize litigation risks. This includes fostering a culture of compliance within the organization, conducting regular internal audits, and seeking legal counsel to ensure alignment with evolving regulations. Companies that prioritize legal compliance contribute to the overall stability and trustworthiness of the financial reporting ecosystem.

10.2. Legal Battles in IFRS Adoption

a. Navigating Legal Challenges in IFRS Transition

The transition to IFRS introduces legal battles that companies must navigate effectively. Disputes may arise over interpretations of IFRS standards, potentially leading to litigation. Companies must engage in comprehensive risk assessments, understanding the legal implications of IFRS adoption, and implementing measures to mitigate potential legal challenges.

b. Legal Safeguards for Companies Adopting IFRS

Legal safeguards for companies adopting IFRS involve proactive steps to minimize legal risks. This includes engaging legal experts in the transition process, conducting impact assessments, and implementing robust governance structures. Companies that prioritize legal safeguards position themselves to navigate the complexities of IFRS adoption with resilience and integrity.

10.3. Risk Mitigation Strategies

a. Legal Safeguards: Mitigating Risks in Regulatory Compliance

Legal safeguards play a pivotal role in mitigating risks associated with regulatory compliance. Companies must implement effective risk management strategies, including regular legal audits, compliance training, and a responsive approach to legal developments. A proactive stance towards legal safeguards enhances a company’s ability to navigate the intricate landscape of financial reporting standards.

b. Strategies for Minimizing Legal Challenges in Reporting Standards

Strategies for minimizing legal challenges in reporting standards involve a holistic approach to risk management. This includes collaboration with legal professionals, staying informed about evolving regulations, and fostering a culture of compliance within the organization. Companies that prioritize these strategies not only mitigate legal challenges but also contribute to the overall reliability and credibility of financial reporting standards.

11. Investor Perspectives

11.1. Investor Preferences

a. Surveying Investor Preferences: GAAP or IFRS?

Understanding investor preferences is crucial in the GAAP vs. IFRS discourse. Surveys play a valuable role in gauging investor sentiment and preferences regarding financial reporting standards. The insights gleaned from such surveys inform standard-setters, regulators, and companies in aligning financial reporting practices with investor expectations.

b. Implications of Investor Preferences on Reporting Standards

The implications of investor preferences on reporting standards are far-reaching. Companies that align with investor preferences enhance transparency and communication, fostering trust and confidence. Standard-setters and regulators, informed by investor feedback, can shape standards that not only meet regulatory requirements but also cater to the information needs of investors in a dynamic and competitive market.

11.2. Impact on Investment Decision-Making

a. Investor Decision Dynamics: GAAP vs IFRS

Investor decision dynamics are influenced by the choice between GAAP and IFRS. Differences in financial reporting standards can impact the comparability of financial statements, influencing investment decisions. Investors must consider the implications of these standards on key metrics, risk assessments, and overall financial analysis to make informed and strategic investment decisions.

b. Strategic Impacts on Investment Choices

The strategic impacts of financial reporting standards on investment choices go beyond compliance. Companies that recognize the link between transparent financial reporting and investor confidence gain a strategic advantage. Similarly, investors who factor in the nuances of GAAP and IFRS differences in their decision-making processes navigate the complexities of the investment landscape more effectively.

11.3. Investor Education Initiatives

a. The Imperative of Investor Education

The imperative of investor education underscores the need for initiatives that enhance investor understanding of financial reporting standards. Educational programs, informational resources, and collaborative efforts between financial institutions and regulatory bodies contribute to a more informed investor community. An educated investor base not only demands higher standards of transparency but also actively participates in shaping the future trajectory of financial reporting.

b. Educating Investors on GAAP vs IFRS Implications

Educating investors on GAAP vs. IFRS implications involves demystifying the complexities of these frameworks. Providing accessible information, conducting investor workshops, and leveraging digital platforms for educational outreach are essential components. Investors empowered with a deeper understanding of financial reporting standards contribute to market efficiency and hold companies accountable for transparent and reliable reporting.

12. Ethical Considerations

12.1. Ethical Dimensions in Financial Reporting

a. Ethics in Financial Reporting Standards

Ethical considerations are integral to the formulation and adherence to financial reporting standards. The principles of integrity, objectivity, and transparency underpin ethical financial reporting. Standard-setters, regulators, and companies must navigate ethical dimensions to ensure that financial reporting serves the interests of investors and the broader public.

b. Upholding Integrity and Objectivity in Reporting

Upholding integrity and objectivity in reporting requires a commitment to ethical conduct. Companies must prioritize accurate representation over short-term gains, fostering a culture that values transparency. Regulators play a crucial role in setting the ethical tone, emphasizing the importance of unbiased and principled financial reporting in maintaining the integrity of capital markets.

12.2. Ethical Challenges for Accountants

a. Common Ethical Dilemmas in GAAP and IFRS

Accountants face common ethical dilemmas in navigating the intricacies of GAAP and IFRS. Issues such as revenue recognition, asset valuation, and disclosure requirements present challenges where ethical considerations intersect with professional responsibilities. Accountants must navigate these dilemmas with a commitment to ethical conduct, considering the broader impact on stakeholders and financial markets.

b. Navigating Ethical Challenges in Reporting Standards

Navigating ethical challenges in reporting standards involves equipping accountants with the tools and guidance needed for principled decision-making. Ongoing professional development, ethical training programs, and mentorship initiatives contribute to a culture of ethical awareness within the accounting profession. Companies, in turn, benefit from the assurance that financial reporting is not only compliant but also aligns with the highest ethical standards.

12.3. Regulatory Measures for Integrity

a. Regulatory Safeguards: Ensuring Ethical Conduct

Regulatory safeguards play a crucial role in ensuring ethical conduct in financial reporting. Regulatory bodies must establish and enforce ethical standards, conduct regular audits, and impose sanctions for non-compliance. A robust regulatory framework promotes integrity in financial reporting, reinforcing public trust in the accuracy and reliability of financial statements.

b. Maintaining the Integrity of Financial Reporting Standards

Maintaining the integrity of financial reporting standards requires a collaborative effort between regulators, standard-setters, and industry stakeholders. Periodic reviews, stakeholder consultations, and responsiveness to emerging ethical challenges contribute to the ongoing refinement of standards. The commitment to upholding ethical principles ensures that financial reporting continues to serve as a cornerstone of trust in the global business landscape.

13. Future Trajectories

13.1. The Evolution of Reporting Standards

a. Anticipating Future Changes

Anticipating future changes in reporting standards involves considering the dynamic nature of global business, technological advancements, and shifts in investor expectations. Standard-setters must adopt a forward-looking approach, engaging in scenario planning and staying attuned to emerging trends. The ability to anticipate future changes ensures that reporting standards remain relevant and adaptive to the evolving needs of the business environment.

b. Technological Innovations and Reporting

Technological innovations are poised to shape the future trajectory of reporting standards. The integration of artificial intelligence, blockchain, and data analytics introduces opportunities for enhanced accuracy, efficiency, and transparency in financial reporting. Standard-setters and companies must embrace these innovations responsibly, balancing the benefits of technology with the imperative of maintaining ethical and transparent financial practices.

13.2. Convergence vs. Divergence

a. Assessing Convergence Prospects

The prospects of convergence between GAAP and IFRS continue to be a topic of consideration. While convergence offers the promise of a more standardized global approach, challenges such as differing legal frameworks and regulatory philosophies persist. Assessing convergence prospects involves a nuanced examination of global trends, regulatory developments, and ongoing efforts by standard-setters to bridge divergences.

b. Navigating Divergences in Global Standards

Navigating divergences in global standards requires a pragmatic approach that acknowledges the unique needs of individual jurisdictions. The coexistence of multiple standards necessitates effective communication, education, and cross-border collaboration. Standard-setters can play a pivotal role in facilitating harmonization efforts, fostering a global financial reporting landscape that balances convergence with the flexibility needed to accommodate diverse economic and regulatory environments.

13.3. Sustainable Reporting Paradigms

a. The Rise of Sustainable Reporting

The rise of sustainable reporting reflects a paradigm shift in the broader understanding of corporate performance. Investors, regulators, and the public increasingly recognize the importance of environmental, social, and governance (ESG) factors. Future reporting standards are likely to integrate sustainable reporting paradigms, providing a more comprehensive view of a company’s long-term value creation and societal impact.

b. Integrating ESG Metrics into Reporting Standards

Integrating ESG metrics into reporting standards requires a collaborative effort between standard-setters, regulators, and industry stakeholders. The development of clear guidelines, standardized metrics, and transparent disclosure requirements enhances the credibility of sustainable reporting. Companies embracing ESG considerations in their financial reporting contribute to a more informed and responsible investment landscape.

14. Conclusion

Financial reporting standards, whether grounded in GAAP or IFRS, serve as the bedrock of transparency, trust, and accountability in the global business landscape. The evolution of these standards reflects a journey of adaptation to changing business dynamics, regulatory landscapes, and investor expectations. While GAAP and IFRS diverge in certain philosophies and approaches, they share a common goal – to provide reliable and relevant information for decision-making.

As we navigate the complexities of GAAP vs. IFRS, it is imperative to recognize the strengths and limitations of each framework. GAAP, with its historical cost emphasis and rule-based approach, offers stability and comparability. In contrast, IFRS, operating under a principles-based approach, provides flexibility and a global perspective. Understanding the variances in revenue recognition, asset valuation, and consolidation methods is essential for investors, analysts, and companies alike.

Looking ahead, the trajectory of reporting standards involves a delicate balance – between convergence and divergence, between technological innovation and ethical considerations, and between traditional financial metrics and sustainable reporting paradigms. The future holds the promise of more standardized, adaptive, and responsible reporting standards that cater to the diverse needs of a dynamic global economy.

In conclusion, as the landscape of financial reporting continues to evolve, stakeholders must remain vigilant, adaptive, and collaborative. Whether one adheres to GAAP or IFRS, the shared commitment to integrity, transparency, and accountability ensures that financial reporting remains a cornerstone of trust in the interconnected world of business and finance.

#cfo#banking#accounting#finance#investment#personal finance#international finance assignment help service#financial management#financial markets#financial modeling#financial planning#financial dominance#financial services#financial literacy#financial drain#management#business#entrepreneur

0 notes

Text

#best computer science homework help#best coursework help#best math homework help#best site for homework help#business law assignment helper#c assignment helper#canadian homework help#cengage accounting homework answers#cengage homework answers economics#cengage microeconomics homework answers#cheapest assignment helper#computer science homework help online#computer science homework helpers

0 notes

Text

#business statistics homework answers#cheap coursework help#statistics 1.1 homework answers#take my wonderlic test for me#accounting hw answers#help me with my algebra homework#elementary statistics homework answers#expert homework help#instant help assignment#homework help for students#pay someone to take my online test for me#need help with accounting assignment#take my proctor

0 notes

Text

I still wonder about the people who double down on communism... and not even like me when I was younger where I got (not the full extent, but got) that the soviet union and such were awful, but just thought that maybe with less terrible people at the helm it could work (later realizing that these kind of things always have power hungry people rise to the top)

Anyway, no I just don't get the "well see, you've admitted your great grandpa owned a chicken, sounds like he deserved to die" people... like the fuck is there even to gain here about being smug while dying on a particularly stupid hill?

#I'm not even gonna try and define what I am with this stuff#cause see; everyone's decided that these terms have super solid cut and dry definitions#when it's like man... people obviously use the same terms to describe wildly different things#you're just being pig headed if you don't accept that and work off what they're saying rather than latching onto a single word#but pig headed they be; so no tossing out single words to latch on to#So what I think is that some level of welfare is both good and also required#and that currency is one of the more effective ways to distribute resources and labor without a whole lot of headache#I want social programs; and if your no details given ask me if I want more or less I'm gonna lean towards more#because apart from the humanitarian point of view; from and economic point of view I think poor people spend money cause they need to#so I think giving benefits; giving health insurance; giving a universal basic income#all end up being good ways to slush money through the system; because things like hospitals benefit from steady use#you want people to have access to them; because that's how they continue to operate#and I think that theft or not taxes are a fact; and I'd rather they go to shit like that#(and I still say senators and the house should only have the healthcare and pay they'd normally qualify for)#(see how long medicaid for all takes to pass if they don't get special insurance; ya dig?)#so that's my point of view; businesses are good; regulation is good; welfare is good; government accountability and transparency are good#I have some terms I could mash together to kinda describe it; but I won't cause that's a fool's errand#so you assign whatever term you want for that in your head; I ain't naming it#but tankies are dumb as shit; I'll say that much; just kinda cruel for the sake of getting a chance to be the one being cruel

1 note

·

View note

Photo

Break the brilliance in auditing code!

Your success in each Auditing Assignment is our exclusive focus as a team of committed professionals. Let us help you handle the complexity and find the right path to excellent scores.

0 notes

Text

Business Law Assignment Help is a website dedicated to providing students with the best possible assistance in completing their business law assignments. Whether you are a student in a business school or a law school, our team of experts can help you with all your business law assignment needs. #BusinessLawAssignmentHelp

https://www.onlinetutorhelps.com/business-law-assignment-help

#Business Law Assignment Help#accounting assignment help#childcare assignment help#xero assignment help#assignment help#finance assignment help#cdr report writing help#nursing assignment help#economics assignment help

0 notes

Text

Unveiling the Legitimacy of Online Business Accounting Assignment Services,DoMyAccountingAssignment.com

Hello all,

Wondering who will Do My business accounting Assignment for Me?

Worry not, we are here for you

In today's digitally-driven academic landscape, students often seek online assistance for their business accounting assignments, aiming to navigate the complexities of this field and excel in their academic pursuits. Amidst the multitude of available services, the legitimacy and credibility of online platforms remain a critical concern. This blog delves deep into the legitimacy and credibility of DoMyAccountingAssignment.com, exploring its worthiness as a leading provider of business accounting assignment services.

Is DoMyAccountingAssignment.com Worth It? DoMyAccountingAssignment.com has garnered a reputation as a trusted platform for students seeking assistance in business accounting assignments. Its worthiness is evident through several key features that distinguish it from others in the industry.

Key Features:

Expertise and Experience: With a team comprising seasoned accounting professionals and tutors, DoMyAccountingAssignment.com boasts extensive expertise in the realm of business accounting. Their experience spanning numerous years showcases a profound understanding of the subject matter and the academic requirements, ensuring top-notch assistance to students.

Tailored and Customized Solutions: The hallmark of DoMyAccountingAssignment.com lies in its commitment to delivering tailored solutions. Each assignment is meticulously crafted to meet the specific needs of individual students. This personalized approach empowers students to grasp concepts thoroughly and achieve academic success.

Academic Integrity and Timeliness: Upholding academic integrity is a core value at DoMyAccountingAssignment.com. They prioritize delivering plagiarism-free content while meeting stringent deadlines. Their commitment to timely delivery ensures that students can submit their assignments punctually, alleviating academic stress.

Comprehensive Support and Accessibility: The platform offers comprehensive support to students, ensuring accessibility and assistance throughout the assignment completion process. Their customer service is responsive and attentive, catering to inquiries and concerns promptly.

Conclusion:

In the realm of online business accounting assignment services, DoMyAccountingAssignment.com emerges as a credible and legitimate platform. Its commitment to academic integrity, personalized solutions, experienced professionals, and timely delivery sets it apart. The platform's dedication to assisting students in navigating the complexities of business accounting assignments positions it as a trustworthy ally in their academic journey. As evidenced by its key features and dedication to student success, DoMyAccountingAssignment.com stands tall as a worthy choice for those seeking reliable assistance in business accounting assignments.

#domyaccountingassignment#pay to do assignment#education#college#homework help#domyaccountingassignmentforme#business accounting homework help#business accounting services#businessaccounting

0 notes

Last Seen Blogs

its-liviosa

Nothing to see here

strawb3rry-sw1ng3

Strawberry Swing

bnhtookmylife

Boku no Hero took my life

sunshines-tt-world

SpreadPositivity