#Pell Grant recipients

Link

0 notes

Text

I’m in this special scholarship program my university offers for low-income/first-gen students and I feel like. legitimate pride in that organization and I’m glad I have the help. they have these logos that they print on stuff for students in the program and a lot of us wear them, and why not tbh? it’s me and a bunch of other smart poor kids. I’m glad we all got here

#bolo speaks#I have one of their stickers on my laptop and I am Waiting for someone to notice#I feel kind of like a faker saying ''poor'' to refer to myself bc I know other people have it worse but I was Literally on food stamps#bestie.... stop lying to yourself#anyway I feel this genuine sense of camaraderie with the other students there. like yesssss we all did it besties !!#the scholarship office has its own staff and I believe most of them used to be in the program/something similar so they Get it#not to support an institution but#thanks <3#anyway federal pell grant recipients stand up we r slaying out here

7 notes

·

View notes

Text

yeah having to pick up used condoms (yes multiple lmao) off the dormitory floor because my roommate’s hookups missed the trashcan turned me off of having roommates forever

#idc if i live at home for forever as a result#people are Disgustang#going to school with rich people as a pell grant recipient is WILD

0 notes

Text

oh? real shit?

#IM A PELL GRANT RECIPIENT.#THE 20K COVERS ALL OF MY LOANS!#IM FEELIN DIZZY HHOOHHHDFGHDHGHH#link#article#us politics#us education

1 note

·

View note

Text

I am literally crying. There are tears on my face.

This is the first time in my entire adult life I’ve felt like I wasn’t running away from an avalanche.

You’ve gotta read it, guys. The whole thing, not just the headline. (DailyKOS is free.) The ten grand in forgiveness is only the start. HE’S FREEZING INTEREST ACCRUAL. WHAT YOU OWE IS WHAT YOU OWE. The requirements for debt repayment are changing so more people are eligible for $0 monthly payments. There are some interest changes for current students that I admittedly kind of skimmed because I’m not a current student, but if you are or you work in education there’s some important stuff for you too.

AND PELL GRANT RECIPIENTS GET $20K IN FORGIVENESS. If you don’t know why that’s important: one of the criticisms of the original $10k plan was that a lot of Black students graduate with greater amounts of debt due to generational poverty and, probably, a dose of discrimination. THE MAJORITY OF PELL GRANTS GO TO BLACK RECIPIENTS. He can’t legally say “oh, and Black students get more,” but he can say “this program for people in dire need gets more, and because of the racial history of our country, most of the people in that program are Black.” And he did. It’s not a perfect solution, unfortunately I don’t think there is a perfect solution, but it’s pretty damn good. I’ll take “80% right” over “100% wrong.”

Also…he didn’t SAY anything about lowering college costs….but he sounds like it’s on his radar.

I now have $31k in student loans, thanks to Biden, and it’s not going to grow anymore. I would like my nieces to not need any—or at most, as the last generation used to say, “you can pay it off with a summer job.”

So let’s keep it on his radar. Until college is simply a step, not a pipe dream, for everyone.

7K notes

·

View notes

Text

On Wednesday, Senate Health, Education, Labor and Pensions (HELP) Chair Bernie Sanders (I-Vermont) and Rep. Pramila Jayapal (D-Washington) reintroduced a proposal to make higher education free at public schools for most Americans — and pay for it by taxing Wall Street.

The College for All Act of 2023 would massively change the higher education landscape in the U.S., taking a step toward Sanders’s long-standing goal of making public college free for all. It would make community college and public vocational schools tuition-free for all students, while making any public college and university free for students from single-parent households making less than $125,000 or couples making less than $250,000 — or, the vast majority of families in the U.S.

The bill would increase federal funding to make tuition free for most students at universities that serve non-white groups, such as Historically Black Colleges and Universities (HBCUs). It would also double the maximum award to Pell Grant recipients at public or nonprofit private colleges from $7,395 to $14,790.

If passed, the lawmakers say their bill would be the biggest expansion of access to higher education since 1965, when President Lyndon B. Johnson signed the Higher Education Act, a bill that would massively increase access to college in the ensuing decades. The proposal would not only increase college access, but also help to tackle the student debt crisis.

“Today, this country tells young people to get the best education they can, and then saddles them for decades with crushing student loan debt. To my mind, that does not make any sense whatsoever,” Sanders said. “In the 21st century, a free public education system that goes from kindergarten through high school is no longer good enough. The time is long overdue to make public colleges and universities tuition-free and debt-free for working families.”

Debt activists expressed support for the bill. “This is the only real solution to the student debt crisis: eliminate tuition and debt by fully funding public colleges and universities,” the Debt Collective wrote on Wednesday. “It’s time for your member of Congress to put up or shut up. Solve the root cause and eliminate tuition and debt.”

These initiatives would be paid for by several new taxes on Wall Street, found in a separate bill reintroduced by Sanders and Rep. Barbara Lee (D-California) on Wednesday. The Tax on Wall Street Speculation would enact a 0.5% tax on stock trades, a 0.1% tax on bonds and a 0.005% tax on trades on derivatives and other types of assets.

The tax would primarily affect the most frequent, and often the wealthiest, traders and would be less than a typical fee for pension management for working class investors, the lawmakers say. It would raise up to $220 billion in the first year of enactment, and over $2.4 trillion over a decade. The proposal has the support of dozens of progressive organizations as well as a large swath of economists.

“Let us never forget: Back in 2008, middle class taxpayers bailed out Wall Street speculators whose greed, recklessness and illegal behavior caused millions of Americans to lose their jobs, homes, life savings, and ability to send their kids to college,” said Sanders. “Now that giant financial institutions are back to making record-breaking profits while millions of Americans struggle to pay rent and feed their families, it is Wall Street’s turn to rebuild the middle class by paying a modest financial transactions tax.”

#us politics#news#truthout#sen. bernie sanders#progressives#progressivism#Democrats#senate health education labor and pensions committee#College for All Act of 2023#tax Wall Street#tax the rich#tax the 1%#tax the wealthy#college for all#student debt#student loan debt#tuition-free college#Historically Black Colleges and Universities#pell grants#Higher Education Act#Rep. Barbara Lee#rep. pramila jayapal#2023

466 notes

·

View notes

Text

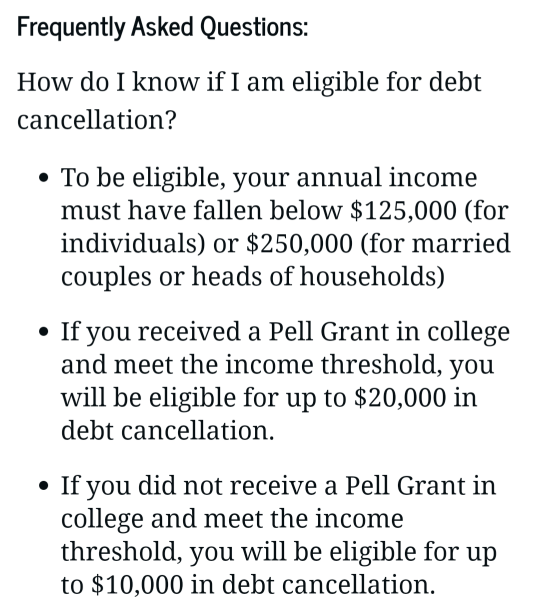

Biden is canceling between 10 to 20k in student loans for any borrower with individual income under 125k or married 250k.

And he is fully restructuring how loan processing works.

There's more at the link but

I think

My student loans might be about to disappear bc I was a Pell grant recipient and my total is under 20k.

I'm gonna cry at my fucking desk.

ALSO THAT LAST BULLET POINT, THAT THE INTEREST WILL BE COVERED EVEN IF YOU CAN ONLY PAY 10$ A MONTH

yep yep yep I'm crying

THE DEBT FORGIVENESS PERIOD BEING SHORTENED BY TEN FUCKING YEARS

gonna just sit at my desk and sob

1K notes

·

View notes

Text

HOLY FUCKING SHIT THIS IS ACTUALLY MASSIVE

so okay the biden administration is cancelling either $10k or $20k in federally-held student debt (i.e. if you've been getting letters from the department of education about the loan pause you're probably in that category) for people making under $125k a year while single or $250k a year as a household

you get the $20k forgiveness amount if you had pell grants, which for instance i did (for my non us based peeps these are the main non-loan way that poor people get college/university cost help here, so doing a higher amount for pell grant recipients is an efficient way of saying "you were / probably still are extra poor, have some more help"), and the $10k amount if you didn't have pell grants

if you're already on an income based repayment plan and fit the other qualifications, they're just gonna go ahead and do the thing, no extra action from you needed. if you're in default like me, or if you're not sure if the department of education currently has the proof of income paperwork they'll need (probably either your latest tax return or, if you didn't file taxes recently, some pay stubs or, if you don't have an income, a notarized affidavit stating that you don't), then there's going to be a government website to upload that information and apply to the program. you can subscribe to dept of education emails about student loans (link is at the bottom of the page when you follow my link to the fact sheet at the top of this post) to be notified when the webpage goes up.

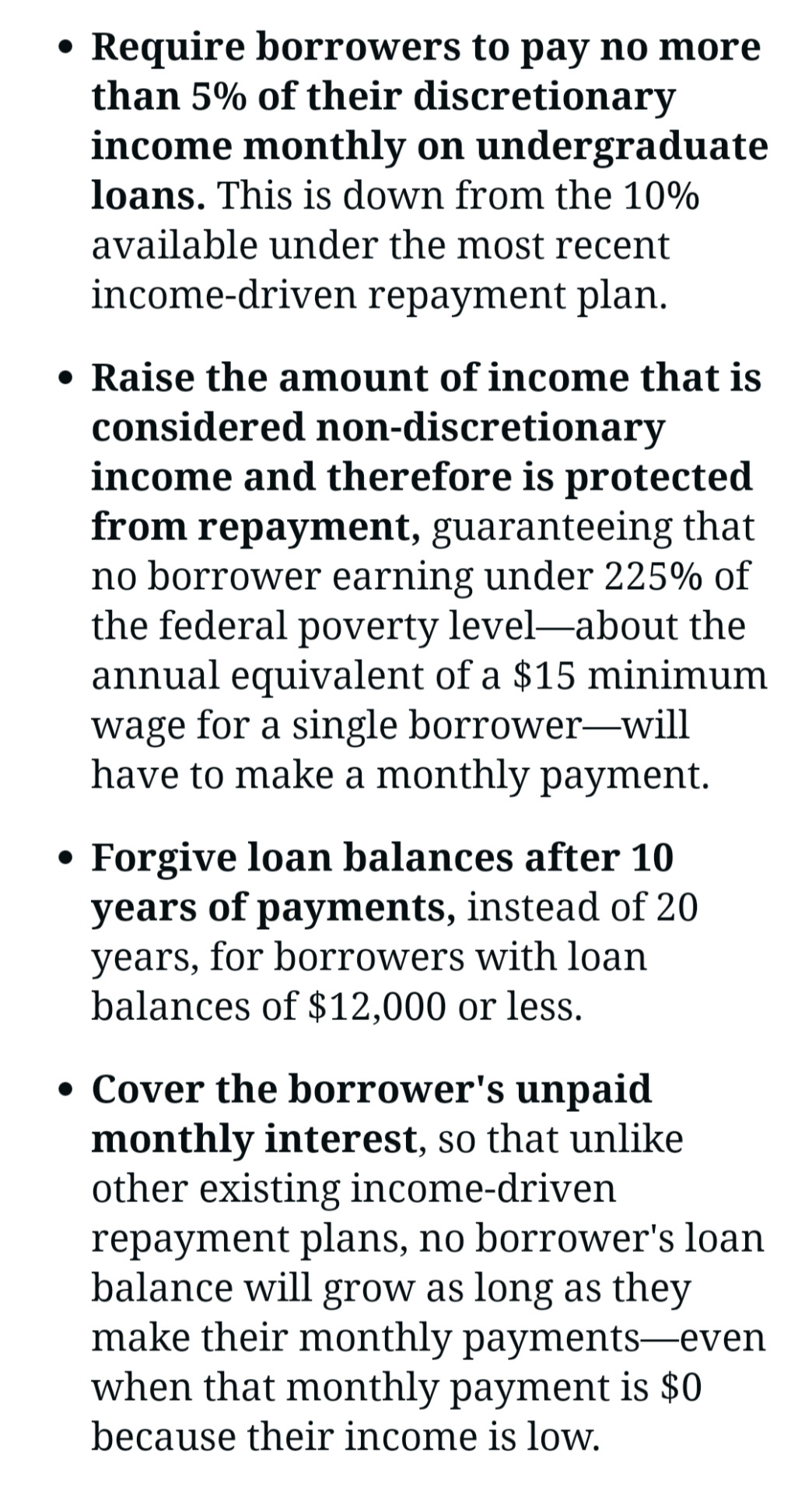

FURTHERMORE, though, and to my mind this is actually bigger -- they're making major changes to how student loan payments and forgiveness are calculated going forward! for income based repayment plans, they're adjusting the income qualifications so that (roughly) no one making under $15 an hour will have to make payments, anyone who makes above that amount will only have to pay half the percentage of their income above the amount that they used to (5% of the amount you make over $31k instead of 10% of the amount over $19k, rounded and slightly sloppily calculatd, but which ADDS UP), you can get your remaining amount forgiven in 10 years instead of the previous 20/25 if you make your payments on time (including if the payments you're making "on time" are $0), and. AND AND AND.

NO MORE INTEREST IF YOU'RE MAKING YOUR PAYMENTS.

I borrowed about $12k for college. I owe about $20k now, because of student loan interest. I haven't been arsed to get out of default for five years, because the interest every month would still have been accruing if I was on an income based payment plan, so my amount owed would actually go *up* every month. NO MORE. If I'm reading this right, and I think I am, the government is going to cover your interest for as long as you make your payments -- again, even if the "payment" you're making on your repayment plan is $0.

This is the biggest fucking thing for poor people's finances since, I don't know, I literally don't even fucking know. The friggin New Deal maybe, I literally don't know. $10k/$20k is eyedropper amounts compared to the sea of student debt, yeah (although for me personally it might knock out my entire amount owed), but this? Having payments that are both halfway affordable AND ACTUALLY LOWER YOUR REMAINING DEBT? I... I don't know what to fucking say. I didn't even imagine -- it did not enter my head that they might cover interest on more than the tiny piddly amount you can get in "subsidized" loans. And for the life of the loans if you make your payments? And for that being 10 years max instead of 25? *falls over*

Anyway you can read all the official verbage at that link up there in case I'm misreading anything. but HOLY FUCK *runs in circles and falls over again*

383 notes

·

View notes

Text

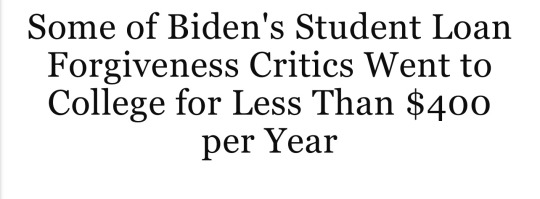

When the Biden Administration announced Wednesday that it would cancel $10,000 of federal student loans for Americans making under $125,000 per year, and $20,000 for Pell Grant recipients at the same income level, the backlash was predictable. Critics, often older people who had gone to college before the 1980s, called the policy a giveaway to the college educated, and unfair to those who had paid their way through school.

While I was reporting my book, The Ones We’ve Been Waiting For, I spent months researching why the student debt crisis has hit younger generations so hard— and why many older Americans don’t seem to understand the unique financial predicament of millennials and Gen Z. One key reason is that college affordability has radically transformed over the last 50 years. Many of the older conservatives who are angry at the idea that taxpayers might pay for student loan forgiveness went to school at a time when the government was heavily subsidizing higher education, and therefore tuition was far less expensive. For them, working their way through school without debt was feasible; for modern millennials and Gen Z, it’s often financially impossible.

Senate Minority leader Mitch McConnell called Biden’s loan forgiveness plan “student loan socialism” and said it was a “slap in the face to every family who sacrificed to save for college.” But when McConnell graduated from the University of Louisville in 1964, annual tuition cost $330 (or roughly $2,500 when adjusted for inflation); today, it costs more than $12,000, a 380% increase. When House Minority Leader Kevin McCarthy, who called the policy a “debt transfer scam,” graduated from California State University, Bakersfield in 1989, tuition was less than $800; today, it’s more than $7,500, a 400% increase when adjusted for inflation. Nevada Senator Catherine Cortez Masto, a moderate Democrat who is running for re-election this year, told Axios she disagreed with the policy because “it doesn’t address the root problems” of college affordability; when Cortez Masto graduated from the University of Nevada in 1986, tuition was a little more than $1,000— today, it’s roughly three times as expensive.

And don’t forget Republican Senator Chuck Grassley, who called the policy “UNFAIR” on Twitter. He graduated from the University of Northern Iowa in 1955, when annual tuition cost roughly $159, or between $40 and $53 per quarter. Today, it costs more than $8,300, a nearly 500% increase even when adjusted for inflation.

Younger generations might say what’s really “unfair” is that many Baby Boomers and the Silent Generation had access to highly subsidized higher education with affordable tuition, while some millennials and Gen Z get just $10,000 of student loan forgiveness. Those calling Biden’s new policy “socialism” would do well to remember this: In 1987, a student at the University of Kansas could pay her tuition with a part-time minimum wage job and still have some left over for books and food. In 2016, a student working a minimum wage job would come up $38,000 short.

👉🏿 https://time.com/6208484/biden-student-loan-critics-college/

#politics#republicans#education#college should be free#cancel student loan debt#student loan debt#college#mitch mcconnell#kevin mccarthy#chuck grassley#catherine cortez masto

351 notes

·

View notes

Text

Student loan forgiveness--my take

8/27/2022: By the way, if you’re like me, and the $10K student loan forgiveness is a tiny pebble compared to your vast mountain of debt, this article offers a reality check.

Out of the 43 million Americans with student debt, 15 million owe less than $10,000, and will have their debt entirely eliminated.

The higher cap of $20K for Pell Grant recipients is estimated to completely eliminate student debt for another 5 million people.

That’s almost half of borrowers who will have their debt eliminated. That half will also include many of the poorest student loan borrowers--the people who went into debt for an education but then did not see much or any improvement in their earning potential.

So there’s a good reason why this program--which can be thought of as a pilot for across-the-board student debt relief--is targeted the way it is. For a mid-priced plan, it’s delivering life-changing benefits to a lot of people.

And for everyone else, there’s a good chance of it reducing your payments and/or the total amount you’ll pay over the life of the loan.

Decreasing your balance will mean an immediate drop in monthly payments for people on standard repayment plans (the ones based on the amount you owe, rather than your income). They’re estimating the average reduction will be $250 a month. (These borrowers will also have the option of keeping the same payment and being debt-free sooner.)

It’s harder to figure out what will happen if you (like me) have a mountain of debt and are on an income-based repayment plan. Chopping $10K off your balance will not have any immediate effect on your payment, but the changes in how IBR payments are calculated may reduce your payment. (However, there’s a lot less information available about those--I haven’t been able to find much of anything about the criteria to qualify. I’m hoping I do, but not counting on it.)

Also, if you’re on track to pay off your loans through IBR before the end of your loan term, reducing the total will mean that you’re paid off sooner. (All income-based repayment plans have built-in forgiveness after 20 or 25 years, so if your debt is seriously disproportionate to your income--mine is!--the $10K may not make a difference in how long you have to pay. But in that case, you’ll be getting another chunk forgiven at the end of your loan term.)

TL:DR: I’m not sure if the new program is going to do anything for me, but looking into it, I realize that A) I’m kind of an edge case, and B) the main reason it won’t do anything is because any benefit I would get from it is swamped by what I’m already getting from my IBR plan.

242 notes

·

View notes

Text

Y'know what, that honestly is better than I expected, tbh. The $20k for pell grant recipients is nice.

Obviously wish 1) there wasn't an income cap (I can't believe so few people make the connections to the high cost of health care to how much student debt Doctors have) and fully universal, 2) the amount was higher if not forgiving all of it, and 3) make public higher education free or at bare minimum affordable for people who aren't wealthy so that we don't walk into this crisis again in another 10-15 years.

But, still, I genuinely didn't think it would happen.

123 notes

·

View notes

Photo

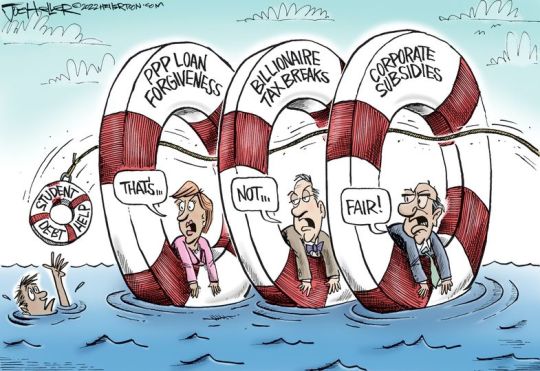

Today's Cartoon- Lifesavers :: [Joe Heller]

* * * *

August 24, 2022 :: Letters From An American :: Heather Cox Richardson

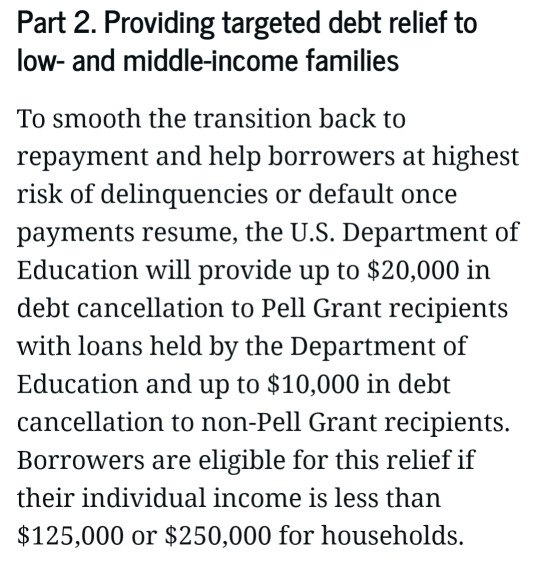

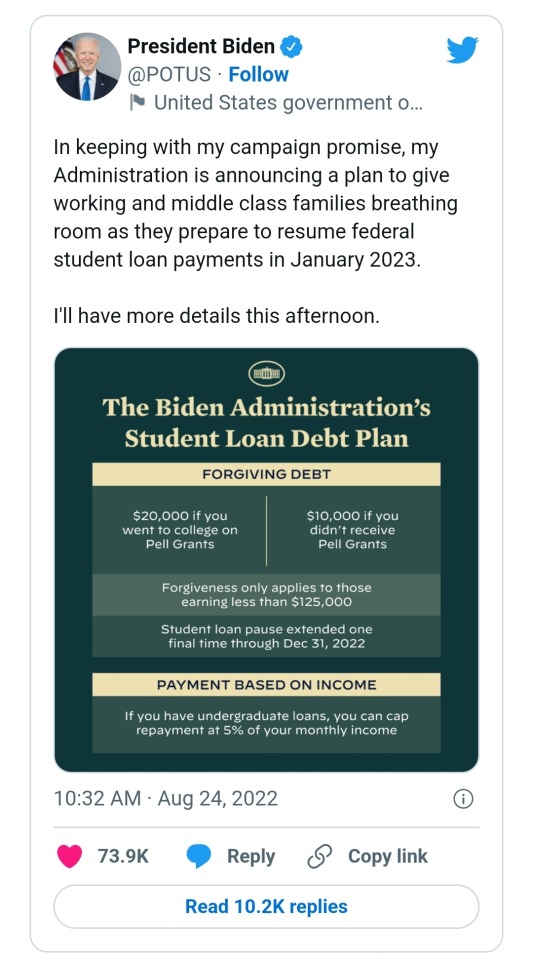

Today, Biden announced another key change in American policy, this time in education. The Department of Education will cancel up to $20,000 of student debt for Pell Grant recipients with loans held by the federal government and up to $10,000 for other borrowers. Pell Grants are targeted at low-income students. Individuals who make less than $125,000 a year or couples who make less than $250,000 a year are eligible. The current pause on federal student loan repayment will be extended once more, through the end of 2022, and the Education Department will try to negotiate a cap on repayments of 5% of a borrower’s discretionary income, down from the current 10%.

The Department of Education estimates that almost 90% of the relief in the measure will go to those earning less than $75,000 a year, and about 43 million borrowers will benefit from the plan.

Opponents of the plan worry that it will be inflationary and that it will not address the skyrocketing cost of four-year colleges. But its supporters worry that the education debt crisis locks people into poverty. They also note that there was very little objection to the forgiveness of 10.2 million Paycheck Protection Program (PPP) loans issued as of July 2022, with $72,500 being the average dollar amount forgiven.

The administration’s plan is a significant pushback to what has happened to education funding since the 1980s. After World War II, the U.S. funded higher education through a series of measures that increased college attendance while also keeping prices low. Beginning in the 1980s, that funding began to dry up and tuition prices rose to make up the difference.

A college education became crucial for a high-paying job, but wages didn’t rise along with the cost of tuition, so families turned to borrowing. Many of them choose the lowest monthly repayment amounts, and some put their loans on hold, meaning their debt balances grow far beyond what they originally borrowed. The shift to “high-tuition, high-aid” caused a “massive total volume of debt,” Assistant Professor of Economics Emily Cook of Tulane University told Jessica Dickler and Annie Nova of CNBC in May. Today, around 44 million Americans owe about $1.7 trillion of educational debt.

Because of the wealth gap between white and Black Americans—the average white family has ten times the wealth of the average Black family—more Black students borrow to finance their education.

Canceling a portion of student debt is a resumption of the older system, ended in the 1980s, under which the government funded cheaper education in the belief it was a social good. In his explanation of the plan, White House National Economic Council Director Bharat Ramamurti told reporters today that “87% of the dollars…are going to people making under $75,000 a year, and 0 dollars, 0%, are going to anybody making over $125,000 in individual income.” He told them it was “instructive” to compare this plan “to what the Republican tax bill did in 2017. It’s basically the reverse. Fifteen percent of the benefits went to people making under $75,000 a year, and 85% went to people making over $75,000 a year. And if you zoom in even more on that, people making over $250,000 a year got nearly half of the benefits of the GOP tax bill and are getting 0 dollars under our [plan].”

#Joe Heller#Student Loan debt#Letters From An American#Heather Cox Richardson#education#student debt#college education

81 notes

·

View notes

Note

Although I decidedly do not need student loan forgiveness (my parents were able to pay for my entire college tuition so I didn’t have to take loans or even work during college, which should tell you all you need to know about my financial background) I stand in solidarity with y’all and I hope Biden comes through on this. I’d much rather my tax dollars go to loan forgiveness than blowing up people abroad.

In this case, it's not Biden we need to worry about; it is, and as ever, the fucking Supreme Court. If some asshole Republican AG sues the administration over this (which they will) and if it reaches the Supreme Court (which it might), then you can absolutely 100% guarantee that it will be struck down in a 6-3 decision along ideological lines. As I said before in all my other posts about this issue, that was the shortcoming with Biden doing this as an executive order (though I'm glad he did anyway). Of course the usual suspects are bitching and whining about how cancelling $10k outright ($20k for Pell Grant recipients, aka the poorest/low-income bracket of students) isn't enough and he should have just done it all, but the plan also contains major structural improvements that will have much longer-term ramifications apart from just outright cancellation, including:

As long as you're making payments (which can include $0 monthly payments if you're on an Income-Driven Repayment plan), NO INTEREST will be added to the principal balance of your loan. That is huge. I probably have at least 10K more in debt than I did when I graduated with my masters, because of the fucking interest. This is one of the things that make student loans so predatory: even if you pay the minimum amount, and if you pay it steadily, you just can't get out of debt because it keeps compounding and increasing. This means your balance will be frozen, and paying it down (even, again, if you don't actually pay anything!) will make a difference!

Full cancellation in 10 years if you've made qualifying payments (which again might be $0 if your income is low)! Also huge! People can spend DECADES paying, so capping it at only 10 years and then they're gone either way is major!

IDR plans are now capped at 5% of your discretionary monthly income, instead of 10%, which again goes a long way to making payments affordable.

If you made payments up/past March 2020 (the start of the first pandemic pause) you can actually get that money back!

Cancelling 20K in debt for the lowest earners/Pell Grantees is legitimately fucking game-changing, and will fully erase student debt for an estimated 20 million people, predominantly Black and Latino with no generational or family wealth to speak of. Even if I get 10k knocked off my student loans, I'll still have upward of 50K left over from my undergraduate/graduate degrees; I also have separate UK-based loans from my PhD which I have had to continue paying this whole time (even though Britain is literally on the verge of becoming a failed state due to economic collapse, but I digress). Of course I wish that I, personally, qualified for more forgiveness or that it would all go away. However, I absolutely recognize that this policy is going to help a lot of people who are considerably worse off than me (and I'm broke, so there you go).

Anyway, there's a lot of good stuff in this policy, and I expect further reform if the Democrats can hold/increase their Congressional majorities. But like I said, the problem isn't Biden; the problem is fucking SCOTUS. So let's see what happens.

75 notes

·

View notes

Text

Young Americans are piling the blame for their student debt balances on conservatives, according to a poll by Generation Lab provided exclusively to Axios.

Why It Matters: The high court's recent decisions on education, including student loans and affirmative action, could drive young voters to the polls.

• Tens of millions of borrowers in the U.S. collectively owe more than $1 trillion.

Catch Up Quick: The Supreme Court's six conservative Justices recently killed President Biden's historic forgiveness plan — and the coming payment resumption carries significant economic and political implications.

• Under Biden's plan, qualifying borrowers would have been forgiven for loans up to $10,000 if they made under $125,000 per year or $20,000 for Pell Grant recipients. Its announcement last summer incited immediate GOP backlash.

• Republicans drove the lawsuits challenging it, criticizing it as a "bailout for the wealthy," and GOP presidential candidates immediately praised the Supreme Court's decision.

By the numbers: Most respondents blamed SCOTUS and the GOP for student debt going unforgiven:

• 47% said the Supreme Court was responsible.

• 38% said the Republicans were responsible.

• 10% said Biden was responsible.

• 5% said Democrats were responsible.

More than half of respondents did not agree with the court's ruling last month, according to Generation Lab.

• 17% agreed with the decision, and 21% were unsure.

• ¾ of people polled said they were aware of the SCOTUS ruling prior to the poll.

Driving The News: Meanwhile, Biden has begun rolling out his plan B and aims to appeal to young voters.

• The administration said Friday it would alleviate $39 billion of debt for 804,000 borrowers.

The Biden re-election campaign could lose voters who care about student debt forgiveness if it doesn't clearly align with them, said Analilia Mejia, co-executive director of the Center for Popular Democracy Action.

• "They obviously need to ensure that there is high enthusiasm across the voting bloc to secure victory" in 2024, she said.

Of Note: Public confidence in the Supreme Court has been staggeringly low in recent months, particularly since it overturned Roe v. Wade.

• "Young people are right. It's a radicalized Supreme Court," Mejia said.

The Big Picture: The coming student loan cliff is the latest in a string of withdrawals of pandemic-era supports.

• Federal student loan payments will resume in October after years of COVID-related pauses.

• Americans with student loan debt tend to be younger, with lower incomes — they're spending a higher share of their income already, so an additional monthly payment will hurt.

Methodology: The Generation Lab, which measures youth trends and perspectives, polled 783 college students and recent graduates nationwide July 12–17 about who's responsible for student loans not being forgiven.

Go Deeper: Who owes the most in federal student loans

#us politics#news#axios#polling#polls#2023#scotus#us supreme court#biden v. nebraska#student loan debt#studen loans#student debt forgiveness#student debt#debt forgiveness#Generation Lab#biden administration#president joe biden#Analilia Mejia#Center for Popular Democracy Action#gen z

55 notes

·

View notes

Text

I saw this headline and had to dig deeper.

Holy shit.

I mean I get it. Our children look around and see what’s happening. Why would they want to go into unfathomable debt for a worthless degree?

But holy shit. The ramifications of this are massive. Maybe someone will come along and tell me why this isn’t as bleak as it sounds, but I can’t imagine how.

Image IDs under the cut.

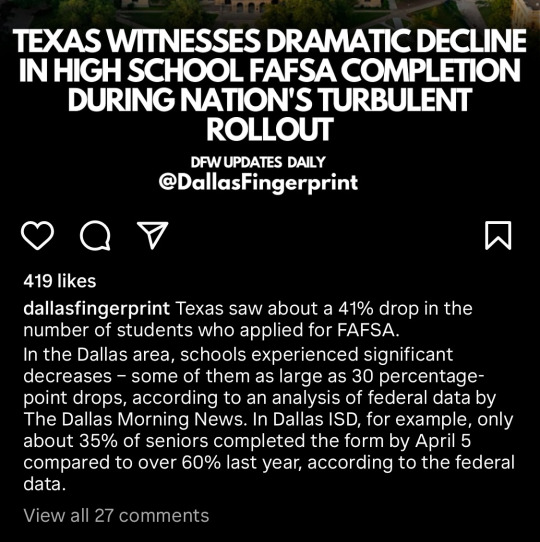

[Instagram post from @DallasFingerprint]

TEXAS WITNESSES DRAMATIC DECLINE IN HIGH SCHOOL FAFSA COMPLETION DURING NATION'S TURBULENT ROLLOUT

Texas saw about a 41% drop in the number of students who applied for FAFSA.

In the Dallas area, schools experienced significant decreases - some of them as large as 30 percentage-point drops, according to an analysis of federal data by The Dallas Morning News. In Dallas ISD, for example, only about 35% of seniors completed the form by April 5 compared to over 60% last year, according to the federal data.

[snippets from an article]

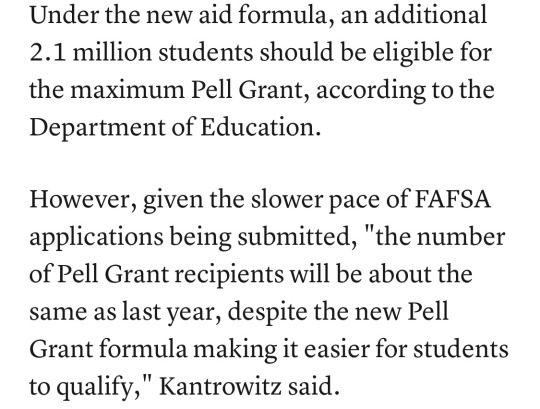

In ordinary years, high school graduates missed out on billions in federal grants because they didn't fill out the FAFSA. The plan to simplify the 2024-25 form was meant to improve college access.

This year's rollout has not achieved that, Kantrowitz said. "This is a complete mess."

Under the new aid formula, an additional 2.1 million students should be eligible for the maximum Pell Grant, according to the Department of Education.

However, given the slower pace of FAFSA applications being submitted, "the number of Pell Grant recipients will be about the same as last year, despite the new Pell Grant formula making it easier for students to qualify," Kantrowitz said.

"We are getting to a point where kids are just giving up on it," said Anne Zinn, a school counselor at Norwich Free Academy in Norwich, Connecticut. "They are so extremely frustrated; they just don't know what to do."

"There's also a psychological aspect of this," Kantrowitz added. "Students have no confidence that they are going to get the financial aid they need to make college affordable and they are opting out."

The FAFSA serves as the gateway to all federal aid money, including loans, work study and grants, the latter of which are the most desirable kinds of assistance because they typically do not need to be repaid.

3 notes

·

View notes

Last Seen Blogs

vypersketches

uhhh

lominsanfog

Lominsan Fog

iptvm3u8

Untitled

anishjitech

Untitled

anishjitech

Untitled