#michael hudson

Text

When you hear "fintech," think "unlicensed bank"

Tomorrow (May 2) I’ll be in Portland at the Cedar Hills Powell’s with Andy Baio for my new novel, Red Team Blues.

In theory, patents are for novel, useful inventions that aren’t obvious “to a skilled practitioner of the art.” But as computers ate our society, grifters began to receive patents for “doing something we’ve done for centuries…with a computer.” “With a computer”: those three words had the power to cloud patent examiners’ minds.

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/05/01/usury/#tech-exceptionalism

Patent trolls — who secure “with a computer” patents and then extract ransoms from people doing normal things on threat of a lawsuit — are an underappreciated form of “tech exceptionalism.” Normally, “tech exceptionalism” refers to bros who wave away things like privacy invasions by arguing that “with a computer” makes it all different.

These tech exceptionalists are the legit face of tech exceptionalism, the Forbes 30 Under 30 set. They’re grifters, but they’re celebrated grifters. There’s a whole bottom-feeding sludge of tech exceptionalists that don’t get the same kind of attention, like patent trolls.

Oh, and the fintech industry.

As Riley Quinn says, “when you hear ‘fintech,’ think: ‘unlicensed bank.’” The majority of fintech “innovation” consists of adding “with a computer” to highly regulated activities and declaring them to be unregulated (and, in the case of crypto, unregulatable).

There are a lot of heavily regulated financial activities, like dealing in securities (something the crypto industry is definitely doing and claims it isn’t). Most people don’t buy or sell securities regularly — indeed, most Americans own little or no stocks.

But you know what regulated financial activity a lot of Americans participate in?

Going into debt.

As wages stagnate and the price of housing, medical care, childcare, transportation and education soar, Americans fund their consumption with debt. Trillions of dollars’ worth of debt. Many of us are privileged to borrow money by walking into a bank and asking for a loan, but millions of Americans are denied that genteel experience.

Instead, working Americans increasingly rely on payday lenders and other usurers who charge sky-high interest rates, on top of penalties and fees, trapping borrowers in an endless cycle of indebtedness. This is an historical sign of a civilization in decline: productive workers require loans to engage in useful activities. Normally, the activity pans out — the crop comes in, say — and the debt is repaid.

But eventually, you’ll get a bad beat. The crop fails, the workshop burns down, a pandemic shuts down production. Instead of paying off your debt, you have to roll it over. Now, you’re in an even worse situation, and the next time you catch a bad break, you go further into debt. Over time, all production comes under the control of creditors.

The historical answer to this is jubilee: a regular wiping-away of all debt. While this was often dressed up in moral language, there was an absolutely practical rationale for it. Without jubilee, eventually, all the farmers stop growing food so that they can grow ornamental flowers for their creditors’ tables. Then, as starvation sets in, civilization collapses:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

As the debt historian Michael Hudson says, “Debts that can’t be paid, won’t be paid.” Without jubilee, indebtedness becomes a chronic and inescapable condition. As more and more creditors attach their claims to debtors’ assets, they have to compete with one another to terrorize the debtor into paying them off, first. One creditor might threaten to garnish your paycheck. Another, to repossess your car. Another, to evict you from your home. Another, to break your arm. Debts that can’t be paid, won’t be paid — but when you have a choice between a broken arm and stealing from your kid’s college fund or the cash-register, maybe the debt can be paid…a little. Of course, digital tools offer all kinds of exciting new tools for arm-breakers — immobilizing your car, say, or deleting the apps on your phone, starting with the ones you use most often:

https://pluralistic.net/2021/04/02/innovation-unlocks-markets/#digital-arm-breakers

Under Trump, payday lenders romped through America. A lobbyist for the payday lenders became a top Trump lawyer:

https://theintercept.com/2017/11/27/white-house-memo-justifying-cfpb-takeover-was-written-by-payday-lender-attorney/

This lobbyist then oversaw Trump’s appointment of a Consumer Finance Protection Bureau boss who deregulated payday lenders, opening the door to triple digit interest rates:

https://www.latimes.com/business/lazarus/la-fi-lazarus-cfpb-payday-lenders-20180119-story.html

To justify this, the payday loan industry found corruptible academics and paid them to write papers defending payday loans as “inclusive.” These papers were secretly co-authored by payday loan industry lobbyists:

https://www.washingtonpost.com/business/2019/02/25/how-payday-lending-industry-insider-tilted-academic-research-its-favor/

Of course, Trump doesn’t read academic papers, so the payday lenders also moved their annual conference to a Trump resort, writing the President a check for $1m:

https://www.propublica.org/article/trump-inc-podcast-payday-lenders-spent-1-million-at-a-trump-resort-and-cashed-in

Biden plugged many of the cracks that Trump created in the firewalls that guard against predatory lenders. Most significantly, he moved Rohit Chopra from the FTC to the CFPB, where, as director, he has overseen a determined effort to rein in the sector. As the CFPB re-establishes regulation, the fintech industry has moved in to add “with a computer” to many regulated activities and so declare them beyond regulation.

One fintech “innovation” is the creation of a “direct to consumer Earned Wage Access” product. Earned Wage Access is just a fancy term for a program some employers offer whereby workers can get paid ahead of payday for the hours they’ve already worked. The direct-to-consumer EWA offers loans without verifying that the borrower has money coming in. Companies like Earnin claim that their faux EWA services are free, but in practice, everyone who uses the service pays for the “Lightning Speed” upsell.

Of course they do. Earnin charges sky-high interest rates and twists borrowers’ arms into leaving a “tip” for the service (yes, they expect you to tip your loan-shark!). Anyone desperate enough to pay triple-digit interest rates and tip the service for originating their loan is desperate and needs to the money now:

https://prospect.org/power/05-01-2023-fintech-ewa-payday-loan-scam/

EWA annual interest rates sit around 300%. The average EWA borrower uses the service two or three times every month. EWA CEOs and lobbyists claim that they’re banking the unbanked — but the reality is that they’re acting as sticky-fingered brokers between banks and young, poor workers, marking up traditional bank services.

This fact is rarely mentioned when EWA companies lobby state legislatures seeking to be exempted from usury rules that are supposed to curb predatory lenders. In Vermont, Earnin wants an exemption from the state’s 18% interest rate cap — remember, the true APR for EWA loans is about 300%.

In Texas, payday lenders are classed as loan brokers, not loan originators and are thus able to avoid the state’s usury caps. EWAs are lobbying the Texas legislature for further exemptions from state money-transmitter and usury limit laws, principally on the strength of the “it’s different: we do it with a computer” logic.

But as Jarod Facundo writes for The American Prospect, quoting Monica Burks from the Center for Responsible Lending, a loan is a loan even if it’s with a computer: “The industry is trying to create a new definition for what a loan is in order to exempt themselves from existing consumer protection laws… When you offer someone a portion of money on the promise that they will repay it, and often that repayment will be accompanied with fees or charges or interest, that’s what a loan is.”

Catch me on tour with Red Team Blues in Mountain View, Berkeley, Portland, Vancouver, Calgary, Toronto, DC, Gaithersburg, Oxford, Hay, Manchester, Nottingham, London, and Berlin!

[Image ID: A stately, columnated bank building, bedecked in garish payday lender signs.]

Image:

Andre Carrotflower (modified)

https://commons.wikimedia.org/wiki/File:30_North_%28former_Pontiac_Commercial_%26_Savings_Bank_Building%29,_Pontiac,_Michigan_-_entrance_and_Chief_Pontiac_relief_sculpture_-_20201213.jpg

CC BY-SA 4.0

https://creativecommons.org/licenses/by-sa/4.0/deed.en

#pluralistic#cfpb#earned wage access#digital armbreakers#loansharks#payday lenders#tech exceptionalism#jubilee#debt#fintech#usury#michael hudson#graeber#debts that can't be paid wont be paid

670 notes

·

View notes

Text

Why all of sudden is France trending…

youtube

youtube

youtube

:

:

France and NATO

:

:

youtube

:

youtube

:

Men in Blue” in Crocus City

:

:

:

3 notes

·

View notes

Text

The National Security Types

I met the national security types when I was at the Hudson Institute. They are crazy. They are filled with hatred [from] the stories they grew up on, of their families suffering in the Holocaust, and they look at the whole rest of the world as being potential enemies who somehow want to put them in the gas chambers. These are twisted people, and indeed this is why people are afraid of the Deep State in the United States. They are nuts.

—Michael Hudson

Mr. Hudson is a Jewish economist writing from an overtly Marxian perspective, yet look at what he has to say (navigate to X for the vid) about the personnel who staff the American Administrative State. Then consider what is happening all around you.

3 notes

·

View notes

Text

Tall Tales Character Introduction: Michael Hudson.

In which TikTok finally lets me upload a video about Michael, but not the one I originally tried to upload.

5 notes

·

View notes

Text

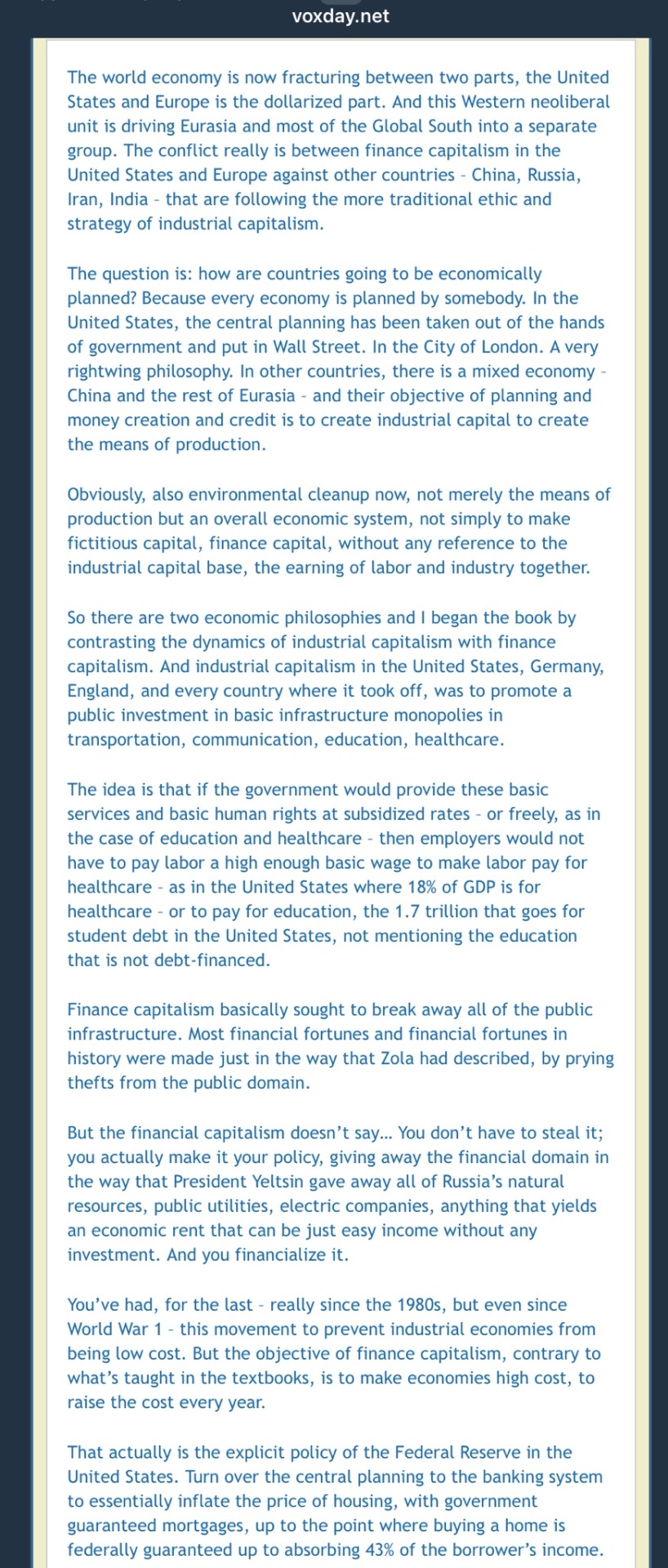

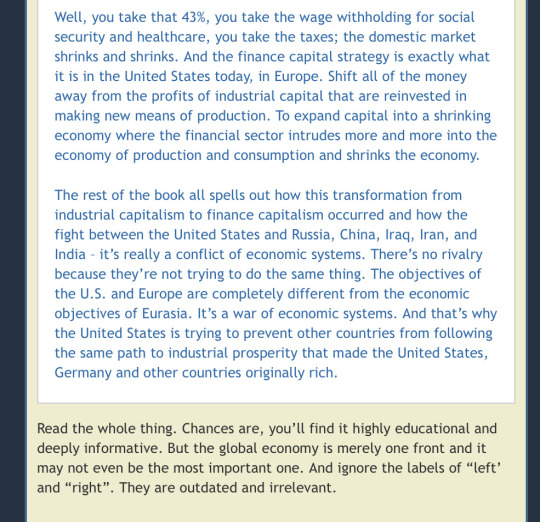

Yves here. One asset America has that most anti-globalists overlook is our legal and court system. The value of foreign exchange transactions due to investment flows was estimated by the Bank of International Settlements at 60 times that of transactions related to trade, although cross border capital flows collapse during financial crises.

Investors greatly prefer transacting though US institutions due to our well-settled precedents. Recall that multinationals investing in Russia as well as some Russian corporations, were often loath to invest directly. They would would go through Cyprus to be subject to English law and a court system run on UK lines. I’ve belatedly come to the view that the reason Cyprus banks blew up in 2013 and were not rescued was the power that be wanted to impede foreign investment in Russia.

That is not to say that US hegemony isn’t past its sell-by date, but that the idea that a new system will come into being soon is way way overdone. I’m of the Gramsci view:

The crisis consists precisely in the fact that the old is dying and the new cannot be born; in this interregnum a great variety of morbid symptoms appear.

By Michael Hudson, a research professor of Economics at University of Missouri, Kansas City, and a research associate at the Levy Economics Institute of Bard College. His latest book is The Destiny of Civilization.

Herodotus (History, Book 1.53) tells the story of Croesus, king of Lydia c. 585-546 BC in what is now Western Turkey and the Ionian shore of the Mediterranean. Croesus conquered Ephesus, Miletus and neighboring Greek-speaking realms, obtaining tribute and booty that made him one of the richest rulers of his time. But these victories and wealth led to arrogance and hubris. Croesus turned his eyes eastward, ambitious to conquer Persia, ruled by Cyrus the Great.

Having endowed the region’s cosmopolitan Temple of Delphi with substantial silver and gold, Croesus asked its Oracle whether he would be successful in the conquest that he had planned. The Pythia priestess answered: “If you go to war against Persia, you will destroy a great empire.”

Croesus therefore set out to attack Persia c. 547 BC. Marching eastward, he attacked Persia’s vassal-state Phrygia. Cyrus mounted a Special Military Operation to drive Croesus back, defeating Croesus’s army, capturing him and taking the opportunity to seize Lydia’s gold to introduce his own Persian gold coinage. So Croesus did indeed destroy a great empire, but it was his own.

Fast-forward to today’s drive by the Biden administration to extend American military power against Russia and, behind it, China. The president asked for advice from today’s analogue to antiquity’s Delphi oracle: the CIA and its allied think tanks. Instead of warning against hubris, they encouraged the neocon dream that attacking Russia and China would consolidate its control of the world economy, achieving the End of History.

Having organized a coup d’état in Ukraine in 2014, the United States sent its NATO proxy army eastward, giving weapons to Ukraine to fight an ethnic war against its Russian-speaking population and turn Russia’s Crimean naval base into a NATO fortress. This Croesus-level ambition aimed at drawing Russia into combat and depleting its ability to defend itself, wrecking its economy in the process and destroying its ability to provide military support to China and other countries targeted as rivals by U.S. hegemony.

After eight years of provocation, a new military attack on Russian-speaking Ukrainians was conspicuously prepared to drive toward the Russian border in February 2022. Russia protected its fellow Russian-speakers from further ethnic violence by mounting its own Special Military Operation. The United States and its NATO allies immediately seized Russia’s foreign-exchange reserves held in Europe and North America, and demanded that all countries impose sanctions against importing Russian energy and grain, hoping that this would crash the ruble’s exchange rate. The Delphic State Department expected that this would cause Russian consumers to revolt and overthrow Vladimir Putin’s government, enabling U.S. maneuvering to install a client oligarchy like the one it had nurtured in the 1990s under President Yeltsin.

A byproduct of this confrontation with Russia was to lock in control over America’s Western European satellites. The aim of this intra-NATO jockeying was to foreclose Europe’s dream of profiting from closer trade and investment relations with Russia by exchanging its industrial manufactures for Russian raw materials. The United States derailed that prospect by blowing up the Nord Stream gas pipeline, cutting off Germany and other countries from access to low-priced Russian gas. That left Europe’s leading economy dependent on higher-cost U.S. Liquified Natural Gas (LNG).

In addition to having to subsidize domestic European gas to prevent widespread insolvency, a large proportion of German Leopard tanks, U.S. Patriot missiles and other NATO “wonder weapons” were destroyed in combat against the Russian army. It became clear that the U.S. strategy was not simply to “fight to the last Ukrainian,” but to fight to the last tank, missile and other weapon being deleted from NATO stocks.

This depletion of NATO’s arms was expected to create a vast replacement market to enrich America’s military-industrial complex. Its NATO customers are being told to increase their military spending to 3 or even 4 percent of GDP. But the weak performance of U.S. and German arms may have crashed this dream, along with Europe’s economies sinking into depression. And with German ‘s industrial economy deranged by the severing of its trade with Russia, German Finance Minister Christian Lindner told the Die Welt newspaper on June 16, 2023 that his country cannot afford to pay more money into the European Union budget, to which it has long been the largest contributor.

Without German exports supporting the euro’s exchange rate, the currency will come under pressure against the dollar as Europe buys LNG and NATO replenishes its depleted weaponry stocks by buying new arms from America. A lower exchange rate will squeeze the purchasing power of European labor, while lower social spending to pay for rearmament and provide gas subsidies threatens to plunge the continent into a depression.

A nationalist reaction against U.S. dominance is rising throughout European politics, and instead of America locking in its control over European policy, the United States may end up losing – not only in Europe but throughout the Global South. Instead of turning Russia’s “ruble to rubble” as President Biden promised, Russia’s balance of trade has soared and its gold supply has increased. So have the gold holdings of other countries whose governments are now aiming to de-dollarize their economies.

It is American diplomacy that is driving Eurasia and the Global South out of the U.S. orbit. America’s hubristic drive for unipolar world dominance could only have been dismantled so rapidly from within. The Biden-Blinken-Nuland administration has done what neither Vladimir Putin nor Chinese President Xi could have hoped to achieve in so short a period. Neither was prepared to throw down the gauntlet and create an alternative to the U.S.-centered world order. But U.S. sanctions against Russia, Iran, Venezuela and China have had the effect of protective tariff barriers to force self-sufficiency in what EU diplomat Josep Borrell calls the world “jungle” outside of the US/NATO “garden.”

Although the Global South and other countries have been complaining ever since the Bandung Conference of Non-Aligned Nations in 1955, they have lacked a critical mass to create a viable alternative. But their attention has now been focused by the U.S. confiscation of Russia’s official dollar reserves in NATO countries. That dispelled the thought of the dollar as a safe vehicle in which to hold international savings. The Bank of England’s earlier seizure of Venezuela’s gold reserves kept in London – promising to donate it to whatever unelected opponents of its socialist regime U.S. diplomats designate – shows how the euro as well as the dollar have been weaponized. And by the way, what ever happened to Libya’s gold reserves?

American diplomats avoid thinking about this scenario. They rely to the one unique advantage the United States has to offer. It may refrain from bombing them, from staging a color revolution to “Pinochet” them by the National Endowment for Democracy, or install a new “Yeltsin” giving the economy away to a client oligarchy.

But refraining from such behavior is all that America can offer. It has de-industrialized its own economy, and its idea of foreign investment is to carve out monopoly-rent seeking opportunities by concentrating technological monopolies and control of oil and grain trade in U.S. hands, as if this is economic efficiency, not rent-seeking.

What has occurred is a change in consciousness. We are seeing the Global Majority trying to create an independent and peacefully negotiated choice as to just what kind of an international order they want. Their aim is not merely to create alternatives to the use of dollars, but an entire new set of institutional alternatives to the IMF and World Bank, the SWIFT bank clearing system, the International Criminal Court and the entire array of institutions that U.S. diplomats have hijacked from the United Nations.

The upshot will be civilizational in scope. We are seeing not the End of History but a fresh alternative to neoliberal finance capitalism and its junk economics of privatization, class war against labor, and the idea that money and credit should be privatized in the hands of a narrow financial class instead of being a public utility to finance economic needs and rising living standards..

#michael hudson#naked capitalism#nato#russia#united states#ukraine#ukraine conflict#the end of history

2 notes

·

View notes

Text

Tarzan by Louis Henry Mitchell

#tarzan#lord greystoke#louis henry mitchell#dark horse comics#dark horse books#modern age#martin powell#michael hudson#diana leto#john clayton

0 notes

Video

youtube

China builds global alternative as US-led financial order decays

0 notes

Text

Get Financial Independence and Crush Your Debt Today!

Are you tired of living under the weight of your debts?

Do you find yourself struggling to make ends meet, despite your best efforts? At Debt Crusher Pro, we understand how difficult it can be to overcome financial difficulties. That’s why we’re here to help you get back on Get Financial Independence and Crush Your Debt Today!

Are you tired of living under the weight of your debts? Do you find yourself struggling to make ends meet, despite your best efforts? At Debt Crusher Pro, we understand how difficult it can be to overcome financial difficulties. That’s why we’re here to help you get back on track and achieve financial independence.

If you’re not sure how to resolve your debt, or if you’re looking for a way to pay less than what you owe, we’re here to help. Our expert team has over 15 years of experience negotiating debt settlement and securing small monthly payment plans for our clients. We can also help you improve your credit score and resolve any issues related to auto loans, mortgages, or business debt.

Don’t let your debt hold you back any longer. By working with Debt Crusher Pro, you can take control of your finances and achieve the financial freedom you deserve. Contact us today to schedule your free consultation and take the first step towards a brighter financial future.

#income inequality#anti capitalism#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters#college debt#wealth inequality#Important#crowfunding#branco#student loans

0 notes

Text

youtube

0 notes

Text

Why the Fed wants to crush workers

The US Federal Reserve has two imperatives: keeping employment high and inflation low. But when these come into conflict — when unemployment falls to near-zero — the Fed forgets all about full employment and cranks up interest rates to “cool the economy” (that is, “to destroy jobs and increase unemployment”).

An economy “cools down” when workers have less money, which means that the prices offered for goods and services go down, as fewer workers have less money to spend. As with every macroeconomic policy, raising interest rates has “distributional effects,” which is economist-speak for “winners and losers.”

Predicting who wins and who loses when interest rates go up requires that we understand the economic relations between different kinds of rich people, as well as relations between rich people and working people. Writing today for The American Prospect’s superb Great Inflation Myths series, Gerald Epstein and Aaron Medlin break it down:

https://prospect.org/economy/2023-01-19-inflation-federal-reserve-protects-one-percent/

Recall that the Fed has two priorities: full employment and low interest rates. But when it weighs these priorities, it does so through “finance colored” glasses: as an institution, the Fed requires help from banks to carry out its policies, while Fed employees rely on those banks for cushy, high-paid jobs when they rotate out of public service.

Inflation is bad for banks, whose fortunes rise and fall based on the value of the interest payments they collect from debtors. When the value of the dollar declines, lenders lose and borrowers win. Think of it this way: say you borrow $10,000 to buy a car, at a moment when $10k is two months’ wages for the average US worker. Then inflation hits: prices go up, workers demand higher pay to keep pace, and a couple years later, $10k is one month’s wages.

If your wages kept pace with inflation, you’re now getting twice as many dollars as you were when you took out the loan. Don’t get too excited: these dollars buy the same quantity of goods as your pre-inflation salary. However, the share of your income that’s eaten by that monthly car-loan payment has been cut in half. You just got a real-terms 50% discount on your car loan!

Inflation is great news for borrowers, bad news for lenders, and any given financial institution is more likely to be a lender than a borrower. The finance sector is the creditor sector, and the Fed is institutionally and personally loyal to the finance sector. When creditors and debtors have opposing interests, the Fed helps creditors win.

The US is a debtor nation. Not the national debt — federal debt and deficits are just scorekeeping. The US government spends money into existence and taxes it out of existence, every single day. If the USG has a deficit, that means it spent more than than it taxed, which is another way of saying that it left more dollars in the economy this year than it took out of it. If the US runs a “balanced budget,” then every dollar that was created this year was matched by another dollar that was annihilated. If the US runs a “surplus,” then there are fewer dollars left for us to use than there were at the start of the year.

The US debt that matters isn’t the federal debt, it’s the private sector’s debt. Your debt and mine. We are a debtor nation. Half of Americans have less than $400 in the bank.

https://www.fool.com/the-ascent/personal-finance/articles/49-of-americans-couldnt-cover-a-400-emergency-expense-today-up-from-32-in-november/

Most Americans have little to no retirement savings. Decades of wage stagnation has left Americans with less buying power, and the economy has been running on consumer debt for a generation. Meanwhile, working Americans have been burdened with forms of inflation the Fed doesn’t give a shit about, like skyrocketing costs for housing and higher education.

When politicians jawbone about “inflation,” they’re talking about the inflation that matters to creditors. Debtors — the bottom 90% — have been burdened with three decades’ worth of steadily mounting inflation that no one talks about. Yesterday, the Prospect ran Nancy Folbre’s outstanding piece on “care inflation” — the skyrocketing costs of day-care, nursing homes, eldercare, etc:

https://prospect.org/economy/2023-01-18-inflation-unfair-costs-of-care/

As Folbre wrote, these costs are doubly burdensome, because they fall on family members (almost entirely women), who have to sacrifice their own earning potential to care for children, or aging people, or disabled family members. The cost of care has increased every year since 1997:

https://pluralistic.net/2023/01/18/wages-for-housework/#low-wage-workers-vs-poor-consumers

So while politicians and economists talk about rescuing “savers” from having their nest-eggs whittled away by inflation, these savers represent a minuscule and dwindling proportion of the public. The real beneficiaries of interest rate hikes isn’t savers, it’s lenders.

Full employment is bad for the wealthy. When everyone has a job, wages go up, because bosses can’t threaten workers with “exile to the reserve army of the unemployed.” If workers are afraid of ending up jobless and homeless, then executives seeking to increase their own firms’ profits can shift money from workers to shareholders without their workers quitting (and if the workers do quit, there are plenty more desperate for their jobs).

What’s more, those same executives own huge portfolios of “financialized” assets — that is, they own claims on the interest payments that borrowers in the economy pay to creditors.

The purpose of raising interest rates is to “cool the economy,” a euphemism for increasing unemployment and reducing wages. Fighting inflation helps creditors and hurts debtors. The same people who benefit from increased unemployment also benefit from low inflation.

Thus: “the current Fed policy of rapidly raising interest rates to fight inflation by throwing people out of work serves as a wealth protection device for the top one percent.”

Now, it’s also true that high interest rates tend to tank the stock market, and rich people also own a lot of stock. This is where it’s important to draw distinctions within the capital class: the merely rich do things for a living (and thus care about companies’ productive capacity), while the super-rich own things for a living, and care about debt service.

Epstein and Medlin are economists at UMass Amherst, and they built a model that looks at the distributional outcomes (that is, the winners and losers) from interest rate hikes, using data from 40 years’ worth of Fed rate hikes:

https://peri.umass.edu/images/Medlin_Epstein_PERI_inflation_conf_WP.pdf

They concluded that “The net impact of the Fed’s restrictive monetary policy on the wealth of the top one percent depends on the timing and balance of [lower inflation and higher interest]. It turns out that in recent decades the outcome has, on balance, worked out quite well for the wealthy.”

How well? “Without intervention by the Fed, a 6 percent acceleration of inflation would erode their wealth by around 30 percent in real terms after three years…when the Fed intervenes with an aggressive tightening, the 1%’s wealth only declines about 16 percent after three years. That is a 14 percent net gain in real terms.”

This is why you see a split between the one-percenters and the ten-percenters in whether the Fed should continue to jack interest rates up. For the 1%, inflation hikes produce massive, long term gains. For the 10%, those gains are smaller and take longer to materialize.

Meanwhile, when there is mass unemployment, both groups benefit from lower wages and are happy to keep interest rates at zero, a rate that (in the absence of a wealth tax) creates massive asset bubbles that drive up the value of houses, stocks and other things that rich people own lots more of than everyone else.

This explains a lot about the current enthusiasm for high interest rates, despite high interest rates’ ability to cause inflation, as Joseph Stiglitz and Ira Regmi wrote in their recent Roosevelt Institute paper:

https://rooseveltinstitute.org/wp-content/uploads/2022/12/RI_CausesofandResponsestoTodaysInflation_Report_202212.pdf

The two esteemed economists compared interest rate hikes to medieval bloodletting, where “doctors” did “more of the same when their therapy failed until the patient either had a miraculous recovery (for which the bloodletters took credit) or died (which was more likely).”

As they document, workers today aren’t recreating the dread “wage-price spiral” of the 1970s: despite low levels of unemployment, workers wages still aren’t keeping up with inflation. Inflation itself is falling, for the fairly obvious reason that covid supply-chain shocks are dwindling and substitutes for Russian gas are coming online.

Economic activity is “largely below trend,” and with healthy levels of sales in “non-traded goods” (imports), meaning that the stuff that American workers are consuming isn’t coming out of America’s pool of resources or manufactured goods, and that spending is leaving the US economy, rather than contributing to an American firm’s buying power.

Despite this, the Fed has a substantial cheering section for continued interest rates, composed of the ultra-rich and their lickspittle Renfields. While the specifics are quite modern, the underlying dynamic is as old as civilization itself.

Historian Michael Hudson specializes in the role that debt and credit played in different societies. As he’s written, ancient civilizations long ago discovered that without periodic debt cancellation, an ever larger share of a societies’ productive capacity gets diverted to the whims of a small elite of lenders, until civilization itself collapses:

https://www.nakedcapitalism.com/2022/07/michael-hudson-from-junk-economics-to-a-false-view-of-history-where-western-civilization-took-a-wrong-turn.html

Here’s how that dynamic goes: to produce things, you need inputs. Farmers need seed, fertilizer, and farm-hands to produce crops. Crucially, you need to acquire these inputs before the crops come in — which means you need to be able to buy inputs before you sell the crops. You have to borrow.

In good years, this works out fine. You borrow money, buy your inputs, produce and sell your goods, and repay the debt. But even the best-prepared producer can get a bad beat: floods, droughts, blights, pandemics…Play the game long enough and eventually you’ll find yourself unable to repay the debt.

In the next round, you go into things owing more money than you can cover, even if you have a bumper crop. You sell your crop, pay as much of the debt as you can, and go into the next season having to borrow more on top of the overhang from the last crisis. This continues over time, until you get another crisis, which you have no reserves to cover because they’ve all been eaten up paying off the last crisis. You go further into debt.

Over the long run, this dynamic produces a society of creditors whose wealth increases every year, who can make coercive claims on the productive labor of everyone else, who not only owes them money, but will owe even more as a result of doing the work that is demanded of them.

Successful ancient civilizations fought this with Jubilee: periodic festivals of debt-forgiveness, which were announced when new monarchs assumed their thrones, or after successful wars, or just whenever the creditor class was getting too powerful and threatened the crown.

Of course, creditors hated this and fought it bitterly, just as our modern one-percenters do. When rulers managed to hold them at bay, their nations prospered. But when creditors captured the state and abolished Jubilee, as happened in ancient Rome, the state collapsed:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Are we speedrunning the collapse of Rome? It’s not for me to say, but I strongly recommend reading Margaret Coker’s in-depth Propublica investigation on how title lenders (loansharks that hit desperate, low-income borrowers with triple-digit interest loans) fired any employee who explained to a borrower that they needed to make more than the minimum payment, or they’d never pay off their debts:

https://www.propublica.org/article/inside-sales-practices-of-biggest-title-lender-in-us

[Image ID: A vintage postcard illustration of the Federal Reserve building in Washington, DC. The building is spattered with blood. In the foreground is a medieval woodcut of a physician bleeding a woman into a bowl while another woman holds a bowl to catch the blood. The physician's head has been replaced with that of Federal Reserve Chairman Jerome Powell.]

#pluralistic#worker power#austerity#monetarism#jerome powell#the fed#federal reserve#finance#banking#economics#macroeconomics#interest rates#the american prospect#the great inflation myths#debt#graeber#michael hudson#indenture#medieval bloodletters

464 notes

·

View notes

Text

Michael Hudson interviewed on his book “The Destiny of Civilization: Finance Capitalism, Industrial Capitalism, or Socialism

youtube

:::

Transcript here:

:::

Excerpt via Vox Day:

3 notes

·

View notes

Link

My old boss Herman Kahn, with whom I worked at the Hudson Institute in the 1970s, had a set speech that he would give at public meetings. He said that back in high school in Los Angeles, his teachers would say what most liberals were saying in the 1940s and 50s: “Wars never solved anything.” It was as if they never changed anything—and therefore shouldn’t be fought.

Herman disagreed, and made lists of all sorts of things that wars had solved in world history, or at least changed. He was right, and of course that is the aim of both sides in today’s New Cold War confrontation in Ukraine.

The question to ask is what today’s New Cold War is trying to change or “solve.” To answer this question, it helps to ask who initiates the war. There always are two sides—the attacker and the attacked. The attacker intends certain consequences, and the attacked looks for unintended consequences of which they can take advantage. In this case, both sides have their dueling sets of intended consequences and special interests.

The active military force and aggression since 1991 has been the United States. Rejecting mutual disarmament of the Warsaw Pact countries and NATO, there was no “peace dividend.” Instead, the U.S. policy executed by the Clinton and subsequent administrations to wage a new military expansion via NATO has paid a 30-year dividend in the form of shifting the foreign policy of Western Europe and other American allies out of their domestic political sphere into their own U.S.-oriented “national security” blob (the word for special interests that must not be named). NATO has become Europe’s foreign policy-making body, even to the point of dominating domestic economic interests.

…

To understand just what U.S. aims and interests are threatened, it is necessary to understand U.S. politics and “the blob,” that is, the government central planning that cannot be explained by looking at ostensibly democratic politics. This is not the politics of U.S. senators and representatives representing their congressional voting districts or states.

It is more realistic to view U.S. economic and foreign policy in terms of the military-industrial complex, the oil and gas (and mining) complex, and the banking and real estate complex than in terms of the political policy of Republicans and Democrats. The key senators and congressional representatives do not represent their states and districts as much as the economic and financial interests of their major political campaign contributors. A Venn diagram would show that in today’s post-Citizens United world, U.S. politicians represent their campaign contributors, not voters. And these contributors fall basically into three main blocs.

Three main oligarchic groups that have bought control of the Senate and Congress to put their own policy makers in the State Department and Defense Department.

…

The FIRE, MIC and OGAM sectors are the three rentier sectors that dominate today’s post-industrial finance capitalism. Their mutual fortunes have soared as MIC and OGAM stocks have increased. And moves to exclude Russia from the Western financial system (and partially now from SWIFT), coupled with the adverse effects of isolating European economies from Russian energy, promise to spur an inflow into dollarized financial securities

…

The dynamic that needs to be traced today is why this oligarchic blob has found its interest in prodding Russia into what Russia evidently viewed as a do-or-die stance to resist the increasingly violent attacks on Ukraine’s eastern Russian-speaking provinces of Luhansk and Donetsk, along with the broader Western threats against Russia.

The rentier “blob’s” expected consequences of the New Cold War

As President Biden explained, the current U.S.-orchestrated military escalation (“Prodding the Bear”) is not really about Ukraine. Biden promised at the outset that no U.S. troops would be involved. But he has been demanding for over a year that Germany prevent the Nord Stream 2 pipeline from supplying its industry and housing with low-priced gas and turn to the much higher-priced U.S. suppliers.

…

So the most pressing U.S. strategic aim of NATO confrontation with Russia is soaring oil and gas prices, above all to the detriment of Germany. In addition to creating profits and stock market gains for U.S. oil companies, higher energy prices will take much of the steam out of the German economy. That looms as the third time in a century that the United States has defeated Germany—each time increasing its control over a German economy increasingly dependent on the United States for imports and policy leadership, with NATO being the effective check against any domestic nationalist resistance.

Higher gasoline, heating and other energy prices also will hurt U.S. consumers and those of other nations (especially Global South energy-deficit economies) and leave less of the U.S. family budget for spending on domestic goods and services. This could squeeze marginalized homeowners and investors, leading to further concentration of absentee ownership of housing and commercial property in the United States, along with buyouts of distressed real estate owners in other countries faced with soaring heating and energy costs. But that is deemed collateral damage by the post-industrial blob.

Food prices also will rise, headed by wheat. (Russia and Ukraine account for 25 percent of world wheat exports.) This will squeeze many Near Eastern and Global South food-deficit countries, worsening their balance of payments and threatening foreign debt defaults.

…

The long-term dream of U.S. New Cold Warriors is to break up Russia, or at least to restore its Yeltsin/Harvard Boys managerial kleptocracy, with oligarchs seeking to cash in their privatizations in Western stock markets. OGAM still dreams of buying majority control of Yukos and Gazprom. Wall Street would love to recreate a Russian stock market boom. And MIC investors at happily anticipating the prospect of selling more weapons to help bring all this about.

Russia’s intentions to benefit from America’s unintended consequences

What does Russia want? Most immediately, to remove the neo-Nazi anti-Russian core that the Maidan massacre and coup put in place in 2014. Ukraine is to be neutralized, which to Russia means basically pro-Russian, dominated by Donetsk, Luhansk and Crimea. The aim is to prevent Ukraine from becoming a staging ground of U.S.-orchestrated anti-Russian moves a la Chechnya and Georgia.

Russia’s longer term aim is to pry Europe away from NATO and U.S. dominance—and in the process, create with China a new multipolar world order centered on an economically integrated Eurasia. The aim is to dissolve NATO altogether, and then to promote the broad disarmament and denuclearization policies that Russia has been pushing for. Not only will this cut back foreign purchases of U.S. arms, but it may end up leading to sanctions against future U.S. military adventurism. That would leave America with less ability to fund its military operations as de-dollarization accelerates.

…

The U.S. confiscation of Russian monetary reserves, following the recent theft of Afghanistan’s reserves (and England’s seizure of Venezuela’s gold stocks held there) threatens every country’s adherence to the Dollar Standard, and hence the dollar’s role as the vehicle for foreign exchange savings by the world’s central banks. This will accelerate the international de-dollarization process already started by Russia and China relying on mutual holdings of each other’s currencies.

Over the longer term, Russia is likely to join China in forming an alternative to the U.S.-dominated IMF and World Bank. Russia’s announcement that it wants to arrest the Ukrainian Nazis and hold a war crimes trial seems to imply an alternative to the Hague court will be established following Russia’s military victory in Ukraine. Only a new international court could try war criminals extending from Ukraine’s neo-Nazi leadership all the way up to U.S. officials responsible for crimes against humanity as defined by the Nuremberg laws.

…

Russia dreamed of creating a new world order, but it was U.S. adventurism that has driven the world into an entirely new order—one that looks to be dominated by China as the default winner now that the European economy is essentially torn apart and America is left with what it has grabbed from Russia and Afghanistan, but without the ability to gain future support.

And everything that I have written above may already be obsolete as Russia and the U.S. have gone on atomic alert. My only hope is that Putin and Biden can agree that if Russia hydrogen bombs Britain and Brussels, that there will be a devil’s (not gentleman’s) agreement not to bomb each other.

With such talk I’m brought back to my discussions with Herman Kahn 50 years ago. He became quite unpopular for writing Thinking about the Unthinkable, meaning atomic war. As he was parodied in Dr. Strangelove, he did indeed say that there would indeed be survivors. But he added that for himself, he hoped to be right under the atom bomb, because it was not a world in which he wanted to survive.

#michael hudson#monthly review#ukraine#germany#military-industrial complex#oil and gas sector#finance insurance and real estate

0 notes

Text

Um actually, its called art.

made by me and @groupieformckagan

#slash#slash gnr#saul hudson x reader#saul hudson#slash x reader#duff#duff gnr#duff mckagan#michael andrew mckagan#duff x reader#duff mckagan x reader#steven adler#steven gnr#steven adler x reader#gnr fanfiction#gnr#gnr x reader#izzy gnr#axl gnr#guns n roses#80s rock#80s music#art#80s bands#i love them#loves of my life

544 notes

·

View notes

Text

"NICE [bleep]ING PROTON PACK!" *honk honk*

#funny pictures#crossover#ghostbusters#beetlejuice#michael keaton#peter venkman#bill murray#ray stantz#dan aykroyd#egon spengler#harold ramis#winston zeddemore#ernie hudson

64 notes

·

View notes

Last Seen Blogs