#vulture capitalism

Text

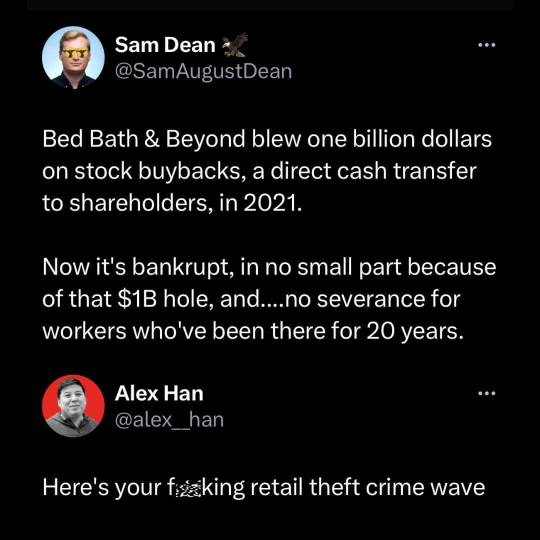

Corporate crime dwarfs retail crime.

1K notes

·

View notes

Text

Private equity plunderers want to buy Simon & Schuster

Going to Defcon this weekend? I'm giving a keynote, "An Audacious Plan to Halt the Internet's Enshittification and Throw it Into Reverse," on Saturday at 12:30pm, followed by a book signing at the No Starch Press booth at 2:30pm!

https://info.defcon.org/event/?id=50826

Last November, publishing got some excellent news: the planned merger of Penguin Random House (the largest publisher in the history of human civilization) with its immediate competitor Simon & Schuster would not be permitted, thanks to the DOJ's deftly argued case against the deal:

https://pluralistic.net/2022/11/07/random-penguins/#if-you-wanted-to-get-there-i-wouldnt-start-from-here

When I was a baby writer, there were dozens of large NY publishers. Today, there are five - and it was almost four. A publishing sector with five giant companies is bad news for writers (as Stephen King said at the trial, the idea that PRH and S&S would bid against each other for books was as absurd as the idea that he and his wife would bid against each other for their next family home).

But it's also bad news for publishing workers, a historically exploited and undervalued workforce whose labor conditions have only declined as the number of employers in the sector dwindled, leading to mass resignations:

https://lithub.com/unlivable-and-untenable-molly-mcghee-on-the-punishing-life-of-junior-publishing-employees/

It should go without saying that workers in sectors with few employers get worse deals from their bosses (see, e.g., the writers' strike and actors' strike). And yup, right on time, PRH, a wildly profitable publisher, fired a bunch of its most senior (and therefore hardest to push around) workers:

https://www.nytimes.com/2023/07/18/books/penguin-random-house-layoffs-buyouts.html

But publishing's contraction into a five-company cartel didn't occur in a vacuum. It was a normal response to monopolization elsewhere in its supply chain. First it was bookselling collapsing into two major chains. Then it was distribution going from 300 companies to three. Today, it's Amazon, a monopolist with unlimited access to the capital markets and a track record of treating publishers "the way a cheetah would pursue a sickly gazelle":

https://pluralistic.net/2023/07/31/seize-the-means-of-computation/#the-internet-con

Monopolies are like Pringles (owned by the consumer packaged goods monopolist Procter & Gamble): you can't have just one. As soon as you get a monopoly in one part of the supply chain, every other part of that chain has to monopolize in self-defense.

Think of healthcare. Consolidation in pharma lead to price-gouging, where hospitals were suddenly paying 1,000% more for routine drugs. Hospitals formed regional monopolies and boycotted pharma companies unless they lowered their prices - and then turned around and screwed insurers, jacking up the price of care. Health insurers gobbled each other up in an orgy of mergers and fought the hospitals.

Now the health care system is composed of a series of gigantic, abusive monopolists - pharma, hospitals, medical equipment, pharmacy benefit managers, insurers - and they all conspire to wreck the lives of only two parts of the system who can't fight back: patients and health care workers. Patients pay more for worse care, and medical workers get paid less for worse working conditions.

So while there was no question that a PRH takeover of Simon & Schuster would be bad for writers and readers, it was also clear that S&S - and indeed, all of the Big Five publishers - would be under pressure from the monopolies in their own supply chain. What's more, it was clear that S&S couldn't remain tethered to Paramount, its current owner.

Last week, Paramount announced that it was going to flip S&S to KKR, one of the world's most notorious private equity companies. KKR has a long, long track record of ghastly behavior, and its portfolio currently includes other publishing industry firms, including one rotten monopolist, raising similar concerns to the ones that scuttled the PRH takeover last year:

https://www.nytimes.com/2023/08/07/books/booksupdate/paramount-simon-and-schuster-kkr-sale.html

Let's review a little of KKR's track record, shall we? Most spectacularly, they are known for buying and destroying Toys R Us in a deal that saw them extract $200m from the company, leaving it bankrupt, with lifetime employees getting $0 in severance even as its executives paid themselves tens of millions in "performance bonuses":

https://memex.craphound.com/2018/06/03/private-equity-bosses-took-200m-out-of-toys-r-us-and-crashed-the-company-lifetime-employees-got-0-in-severance/

The pillaging of Toys R Us isn't the worst thing KKR did, but it was the most brazen. KKR lit a beloved national chain on fire and then walked away, hands in pockets, whistling. They didn't even bother to clear their former employees' sensitive personnel records out of the unlocked filing cabinets before they scarpered:

https://memex.craphound.com/2018/09/23/exploring-the-ruins-of-a-toys-r-us-discovering-a-trove-of-sensitive-employee-data/

But as flashy as the Toys R Us caper was, it wasn't the worst. Private equity funds specialize in buying up businesses, loading them with debts, paying themselves, and then leaving them to collapse. They're sometimes called vulture capitalists, but they're really vampire capitalists:

https://www.motherjones.com/politics/2022/05/private-equity-buyout-kkr-houdaille/

Given a choice, PE companies don't want to prey on sick businesses - they preferentially drain off value from thriving ones, preferably ones that we must use, which is why PE - and KKR in particular - loves to buy health care companies.

Heard of the "surprise billing epidemic"? That's where you go to a hospital that's covered by your insurer, only to discover - after the fact - that the emergency room is operated by a separate, PE-backed company that charges you thousands for junk fees. KKR and Blackstone invented this scam, then funneled millions into fighting the No Surprises Act, which more-or-less killed it:

https://pluralistic.net/2020/04/21/all-in-it-together/#doctor-patient-unity

KKR took one of the nation's largest healthcare providers, Envision, hostage to surprise billing, making it dependent on these fraudulent payments. When Congress finally acted to end this scam, KKR was able to take to the nation's editorial pages and damn Congress for recklessly endangering all the patients who relied on it:

https://pluralistic.net/2022/03/14/unhealthy-finances/#steins-law

Like any smart vampire, KKR doesn't drain its victim in one go. They find all kinds of ways to stretch out the blood supply. During the pandemic, KKR was front of the line to get massive bailouts for its health-care holdings, even as it fired health-care workers, increasing the workload and decreasing the pay of the survivors of its indiscriminate cuts:

https://pluralistic.net/2020/04/11/socialized-losses/#socialized-losses

It's not just emergency rooms. KKR bought and looted homes for people with disabilities, slashed wages, cut staff, and then feigned surprise at the deaths, abuse and misery that followed:

https://www.buzzfeednews.com/article/kendalltaggart/kkr-brightspring-disability-private-equity-abuse

Workers' wages went down to $8/hour, and they were given 36 hour shifts, and then KKR threatened to have any worker who walked off the job criminally charged with patient abandonment:

https://pluralistic.net/2023/06/02/plunderers/#farben

For KKR, people with disabilities and patients make great victims - disempowered and atomized, unable to fight back. No surprise, then, that so many of KKR's scams target poor people - another group that struggles to get justice when wronged. KKR took over Dollar General in 2007 and embarked on a nationwide expansion campaign, using abusive preferential distributor contracts and targeting community-owned grocers to trap poor people into buying the most heavily processed, least nutritious, most profitable food available:

https://pluralistic.net/2023/03/27/walmarts-jackals/#cheater-sizes

94.5% of the Paycheck Protection Program - designed to help small businesses keep their workers payrolled during lockdown - went to giant businesses, fraudulently siphoned off by companies like Longview Power, 40% owned by KKR:

https://pluralistic.net/2020/04/20/great-danes/#ppp

KKR also helped engineer a loophole in the Trump tax cuts, convincing Justin Muzinich to carve out taxes for C-Corporations, which let KKR save billions in taxes:

https://pluralistic.net/2020/06/02/broken-windows/#Justin-Muzinich

KKR sinks its fangs in every part of the economy, thanks to the vast fortunes it amassed from its investors, ripped off from its customers, and fraudulently obtained from the public purse. After the pandemic, KKR scooped up hundreds of companies at firesale prices:

https://pluralistic.net/2020/03/30/medtronic-stole-your-ventilator/#blackstone-kkr

Ironically, the investors in KKR funds are also its victims - especially giant public pension funds, whom KKR has systematically defrauded for years:

https://pluralistic.net/2020/07/22/stimpank/#kentucky

And now KKR has come for Simon & Schuster. The buyout was trumpeted to the press as a done deal, but it's far from a fait accompli. Before the deal can close, the FTC will have to bless it. That blessing is far from a foregone conclusion. KKR also owns Overdrive, the monopoly supplier of e-lending software to libraries.

Overdrive has a host of predatory practices, loathed by both libraries and publishers (indeed, much of the publishing sector's outrage at library e-lending is really displaced anger at Overdrive). There's a plausible case that the merger of one of the Big Five publishers with the e-lending monopoly will present competition issues every bit as deal-breaking as the PRH/S&S merger posed.

(Image: Sefa Tekin/Pexels, modified)

I’m kickstarting the audiobook for “The Internet Con: How To Seize the Means of Computation,” a Big Tech disassembly manual to disenshittify the web and bring back the old, good internet. It’s a DRM-free book, which means Audible won’t carry it, so this crowdfunder is essential. Back now to get the audio, Verso hardcover and ebook:

http://seizethemeansofcomputation.org

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/08/08/vampire-capitalism/#kkr

#kkr#simon and schuster#publishing#penguin random house#ppp loans#looters#plunderers#vampire capitalism#vulture capitalism#debt#private equity#pe#harmful dominance#monopoly#trustbusters#incentives matter#labor#writing#publishing workers#recorded books#overdrive#glam#libraries#toys r us#pluralistic

187 notes

·

View notes

Photo

@tolstoybb

#politics#the left#banking#silicon valley#venture capital#venture capitalism#vulture capitalism#tech industry

100 notes

·

View notes

Text

1 note

·

View note

Text

Come fly with us, August 13 2024.

#books#near future#sciencefiction#glass house#surveillance#smart home devices#vulture capitalism#social media#tor books#whodunnit

1 note

·

View note

Text

1 note

·

View note

Text

Wall Street Journal goes to bat for the vultures who want to steal your house

Tonight (June 5) at 7:15PM, I’m in London at the British Library with my novel Red Team Blues, hosted by Baroness Martha Lane Fox.

Tomorrow (June 6), I’m on a Rightscon panel about interoperability.

The tacit social contract between the Wall Street Journal and its readers is this: the editorial page is for ideology, and the news section is for reality. Money talks and bullshit walks — and reality’s well-known anticapitalist bias means that hewing too closely to ideology will make you broke, and thus unable to push your ideology.

That’s why the editorial page will rail against “printing money” while the news section will confine itself to asking which kinds of federal spending competes with the private sector (creating a bidding war that drives up prices) and which kinds are not. If you want frothing takes about how covid relief checks will create “debt for our grandchildren,” seek it on the editorial page. For sober recognition that giving small amounts of money to working people will simply go to reducing consumer and student debt, look to the news.

But WSJ reporters haven’t had their corpus colossi severed: the brain-lobe that understands economic reality crosstalks with the lobe that worship the idea of a class hierarchy with capital on top and workers tugging their forelacks. When that happens, the coverage gets weird.

Take this weekend’s massive feature on “zombie mortgages,” long-written-off second mortgages that have been bought by pennies for vultures who are now trying to call them in:

https://www.wsj.com/articles/zombie-mortgages-could-force-some-homeowners-into-foreclosure-e615ab2a

These second mortgages — often in the form of home equity lines of credit (HELOCs) — date back to the subprime bubble of the early 2000s. As housing prices spiked to obscene levels and banks figured out how to issue risky mortgages and sell them off to suckers, everyday people were encouraged — and often tricked — into borrowing heavily against their houses, on complicated terms that could see their payments skyrocket down the road.

Once the bubble popped in 2008, the value of these houses crashed, and the mortgages fell “underwater” — meaning that market value of the homes was less than the amount outstanding on the mortgage. This triggered the foreclosure crisis, where banks that had received billions in public money forced their borrowers out of their homes. This was official policy: Obama’s Treasury Secretary Timothy Geithner boasted that forcing Americans out of their homes would “foam the runways” for the banks and give them a soft landing;

https://pluralistic.net/2023/03/06/personnel-are-policy/#janice-eberly

With so many homes underwater on their first mortgages, the holders of those second mortgages wrote them off. They had bought high-risk, high reward debt, the kind whose claims come after the other creditors have been paid off. As prices collapsed, it became clear that there wouldn’t be anything left over after those higher-priority loans were paid off.

The lenders (or the bag-holders the lenders sold the loans to) gave up. They stopped sending borrowers notices, stopped trying to collect. That’s the way markets work, after all — win some, lose some.

But then something funny happened: private equity firms, flush with cash from an increasingly wealthy caste of one percenters, went on a buying spree, snapping up every home they could lay hands on, becoming America’s foremost slumlords, presiding over an inventory of badly maintained homes whose tenants are drowned in junk fees before being evicted:

https://pluralistic.net/2022/02/08/wall-street-landlords/#the-new-slumlords

This drove a new real estate bubble, as PE companies engaged in bidding wars, confident that they could recoup high one-time payments by charging working people half their incomes in rent on homes they rented by the room. The “recovery” of real estate property brought those second mortgages back from the dead, creating the “zombie mortgages” the WSJ writes about.

These zombie mortgages were then sold at pennies on the dollar to vulture capitalists — finance firms who make a bet that they can convince the debtors to cough up on these old debts. This “distressed debt investing” is a scam that will be familiar to anyone who spends any time watching “finance influencers” — like forex trading and real estate flipping, it’s a favorite get-rich-quick scheme peddled to desperate people seeking “passive income.”

Like all get-rich-quick schemes, distressed debt investing is too good to be true. These ancient debts are generally past the statute of limitations and have been zeroed out by law. Even “good” debts generally lack any kind of paper-trail, having been traded from one aspiring arm-breaker to another so many times that the receipts are long gone.

Ultimately, distressed debt “investing” is a form of fraud, in which the “investor” has to master a social engineering patter in which they convince the putative debtor to pay debts they don’t actually owe, either by shading the truth or lying outright, generally salted with threats of civil and criminal penalties for a failure to pay.

That certainly goes for zombie mortgages. Writing about the WSJ’s coverage on Naked Capitalism, Yves Smith reminds readers not to “pay these extortionists a dime” without consulting a lawyer or a nonprofit debt counsellor, because any payment “vitiates” (revives) an otherwise dead loan:

https://www.nakedcapitalism.com/2023/06/wall-street-journal-aids-vulture-investors-threatening-second-mortgage-borrowers-with-foreclosure-on-nearly-always-legally-unenforceable-debt.html

But the WSJ’s 35-paragraph story somehow finds little room to advise readers on how to handle these shakedowns. Instead, it lionizes the arm-breakers who are chasing these debts as “investors…[who] make mortgage lending work.” The Journal even repeats — without commentary — the that these so-called investors’ “goal is to positively impact homeowners’ lives by helping them resolve past debt.”

This is where the Journal’s ideology bleeds off the editorial page into the news section. There is no credible theory that says that mortgage markets are improved by safeguarding the rights of vulture capitalists who buy old, forgotten second mortgages off reckless lenders who wrote them off a decade ago.

Doubtless there’s some version of the Hayek Mind-Virus that says that upholding the claims of lenders — even after those claims have been forgotten, revived and sold off — will give “capital allocators” the “confidence” they need to make loans in the future, which will improve the ability of everyday people to afford to buy houses, incentivizing developers to build houses, etc, etc.

But this is an ideological fairy-tale. As Michael Hudson describes in his brilliant histories of jubilee — debt cancellation — through history, societies that unfailingly prioritize the claims of lenders over borrowers eventually collapse:

https://pluralistic.net/2022/07/08/jubilant/#construire-des-passerelles

Foundationally, debts are amassed by producers who need to borrow capital to make the things that we all need. A farmer needs to borrow for seed and equipment and labor in order to sow and reap the harvest. If the harvest comes in, the farmer pays their debts. But not every harvest comes in — blight, storms, war or sickness — will eventually cause a failure and a default.

In those bad years, farmers don’t pay their debts, and then they add to them, borrowing for the next year. Even if that year’s harvest is good, some debt remains. Gradually, over time, farmers catch enough bad beats that they end up hopelessly mired in debt — debt that is passed on to their kids, just as the right to collect the debts are passed on to the lenders’ kids.

Left on its own, this splits society into hereditary creditors who get to dictate the conduct of hereditary debtors. Run things this way long enough and every farmer finds themselves obliged to grow ornamental flowers and dainties for their creditors’ dinner tables, while everyone else goes hungry — and society collapses.

The answer is jubilee: periodically zeroing out creditors’ claims by wiping all debts away. Jubilees were declared when a new king took the throne, or at set intervals, or whenever things got too lopsided. The point of capital allocation is efficiency and thus shared prosperity, not enriching capital allocators. That enrichment is merely an incentive, not the goal.

For generations, American policy has been to make housing asset appreciation the primary means by which families amass and pass on wealth; this is in contrast to, say, labor rights, which produce wealth by rewarding work with more pay and benefits. The American vision is that workers don’t need rights as workers, they need rights as owners — of homes, which will always increase in value.

There’s an obvious flaw in this logic: houses are necessities, as well as assets. You need a place to live in order to raise a family, do a job, found a business, get an education, recover from sickness or live out your retirement. Making houses monotonically more expensive benefits the people who get in early, but everyone else ends up crushed when their human necessity is treated as an asset:

https://gen.medium.com/the-rents-too-damned-high-520f958d5ec5

Worse: without a strong labor sector to provide countervailing force for capital, US politics has become increasingly friendly to rent-seekers of all kinds, who have increased the cost of health-care, education, and long-term care to eye-watering heights, forcing workers to remortgage, or sell off, the homes that were meant to be the source of their family’s long-term prosperity:

https://doctorow.medium.com/the-end-of-the-road-to-serfdom-bfad6f3b35a9

Today, reality’s leftist bias is getting harder and harder to ignore. The idea that people who buy debt at pennies on the dollar should be cheered on as they drain the bank-accounts — or seize the homes — of people who do productive work is pure ideology, the kind of thing you’d expect to see on the WSJ’s editorial page, but which sticks out like a sore thumb in the news pages.

Thankfully, the Consumer Finance Protection Bureau is on the case. Director Rohit Chopra has warned the arm-breakers chasing payments on zombie mortgages that it’s illegal for them to “threaten judicial actions, such as foreclosures, for debts that are past a state’s statute of limitations.”

But there’s still plenty of room for more action. As Smith notes, the 2012 National Mortgage Settlement — a “get out of jail for almost free” card for the big banks — enticed lots of banks to discharge those second mortgages. Per Smith: “if any servicer sold a second mortgage to a vulture lender that it had charged off and used for credit in the National Mortgage Settlement, it defrauded the Feds and applicable state.”

Maybe some hungry state attorney general could go after the banks pulling these fast ones and hit them for millions in fines — and then use the money to build public housing.

Catch me on tour with Red Team Blues in London and Berlin!

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/06/04/vulture-capitalism/#distressed-assets

[Image ID: A Georgian eviction scene in which a bobby oversees three thugs who are using a battering ram to knock down a rural cottage wall. The image has been crudely colorized. A vulture looks on from the right, wearing a top-hat. The battering ram bears the WSJ logo.]

#pluralistic#great financial crisis#vulture capitalism#debts that can’t be paid won’t be paid#zombie debts#jubilee#michael hudson#wall street journal#business press#house thieves#debt#statute of limitations

129 notes

·

View notes

Text

Last week, the nation’s largest prison and jail telecom corporation, Securus, effectively defaulted on more than a billion dollars of debt. After decades of preying on incarcerated people and their loved ones with exploitative call rates and other predatory practices that have driven millions of families into debt, Securus is being crushed under the weight of its own. In March, the company’s creditors gave the corporation an eight-month extension to pay up, urging its sale to a new owner to stave off an otherwise imminent bankruptcy.

Securus is one of two corporations that dominate roughly 80 percent of the U.S. prison telecom industry, forming an effective duopoly that thrives on the captive markets found inside the nation’s lockups. Both companies are owned by private-equity firms: Securus, by Platinum Equity, and ViaPath (previously Global Tel Link), by American Securities.

The slow death of the largest player in this space is not accidental. It follows six years of intense advocacy to expose the vulnerability of the prison telecom industry’s business model on both ethical and economic grounds. Organizers have waged a strategic war against Securus, educating investors and the public about the company’s predatory practices while successfully advocating for legislation and regulation to rein them in.

With Platinum now on the hook to pay $1.3 billion of Securus debt this year following a series of failed attempts to refinance, bankruptcy seems inevitable. The company’s failure would represent a remarkable victory for advocates—and a potential beginning of the end for the prison telecom industry as we know it.

6 notes

·

View notes

Video

youtube

Peter Boyle | The Rise And Fall Of Blitzscaling!

#politics#the left#economics#capitalism#late capitalism#late stage capitalism#silicon valley#venture capital#vulture capitalism#video#youtube

9 notes

·

View notes

Text

From a thread about how private-equity firms have been buying up hospices. Somebody asked how they can buy out so many private companies whose owners would not willingly put their charges at the mercy of total scum.

Not an expert by any means, but I see nobody else has answered so I'll give it a shot. In the less extreme case, the seller has no choice but to sell or go under, so they'll take the best offer they can get. In the more extreme case, there is no choice because the seller has already taken on some debt under conditions that give the creditors first claim on assets. Then it's easy for the rentiers to buy up the debt and then wait - usually not long - for the company to run out of operating funds and trigger their own effective acquisition.

I once worked at a startup that suffered a similar fate. They had taken on some debt - a small amount really - during desperate times. Later, before the debt was paid off, they ran out of operating funds. Boom. Game over. The company shut down, most employees were immediately let go except for a few charged with liquidating the assets and wrapping up all the IP which went into storage somewhere never to be used again.

It sucked. That creditor probably made a tiny bit more than they had loaned originally, while everyone else lost. And the only way their own business model worked was to do the same thing over and over and over again, destroying enough aggregate value that even the residue they skimmed off the top could pay for their yachts or third vacation homes.

BTW, here's the original story.

1 note

·

View note

Text

So if you don’t follow comics, especially the mostly capewank US variety, there’s still a few independent publishers besides Disney and Warner Bros’ respective IP farms. Oni Press, publisher of Scott Pilgrim, was one of them. I say was, because over the last week they’ve fired almost all of their staff including editors, which is something most might recognize as being a bad thing for a publisher of any sort of media to do if they want to continue to publish media of any quality.

They also fired all of their PR staff which is how they farted out this yesterday without a hint of irony:

Notice that aside from the name Lion Forge Comics they don’t mention the word “comic” anywhere in the release. In addition to the fact they used the word “content” three times in a single paragraph, and call readers “content consumers”.

They had some good comics, and stayed out of the superhero ghetto most of the time, but they also kinda paid like shit, and nothing they did really tugged at me, Scott Pilgrim included. Still, it’s never a good thing when one of the few indy publishers in this industry fails.

From the looks of things they’re getting stripped clean after getting bought out in 2019. This is important since it makes the bit about “25 years in the business” hollow bullshit.

1 note

·

View note

Photo

A quick obituary, if y'all don't mind.

In 2018 my cat Lace died. it was sudden and mysterious and she went to one of her favorite spots to do it alone. She was buried just before a big hurricane at the beginning of summer. a little bit later me and my mom took a road trip to Georgia to see family, and I was inspired by the life and death i saw on the side of the roads to draw the 24/7 Haunted Roadside Diner comics.

In 2022 my cat Coup died. it was a long fight through 7 months of cancer that ended with me holding him at the vet as he took one last big jump after months of losing the ability to do so. he was cremated just before a big hurricane at the end of summer. a little bit later me and my mom took a road trip to Georgia to see family, and I was inspired by the life and death i saw on the side of the roads to draw more 24/7 Haunted Roadside Diner comics after not thinking about them for years.

They were total brats to each other most of the time and they could never agree on anything, but they were my friends for almost half of my life and they called truces to sit on my bed together and comfort me during the Bad Health Times or the Bad Emotions Times. I didn't realize that I was repeating history a little bit until I was almost finished redrawing these first 5 pages, but I think it's funny that even though they tried to go out as they lived, as fussy little opposites, that I started really healing from both of their deaths creatively in the same way. So here's to the prettiest girl in the world and the baby boy. I probably could have gotten weird enough emotionally to write about roadkill ghost stories on my own, but y'all made it way easier to get there.

I redrew the first 5 pages to fit in better with any future 24/7 HRD comics I want to do (and generally flex my improved art/writing skills), so I’ll be posting one of those a day for the next few days. I've got 5 more pages and some illustrations planned for spooky season (October/November) along with some Downtrodden stuff so y'know. Nature is healing.

Hopefully I'll have more to post soon. the future is lookin' lonelier without my small grey guy, but it'll still have bright spots I bet. I hope.

#24/7 haunted roadside diner#the haunted roadside diner#vulture#comic#horror#weird image to put an obituary on but who's gonna stop me?#also don't get used to the capital letters because this is copy pasted from patreon#people have to literally pay me to use the garbage shift key on this laptop

3K notes

·

View notes

Text

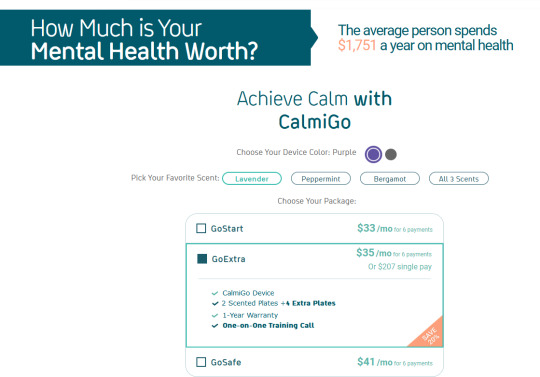

Reminder not to use Better Help because they have sold user data, medical questionares and emails to third party companies.

Their founder is also a IDF veteran (As of 2015 Teladoc Health owns it as a parent company, however, Teladoc Health is the parent company who oversaw it during the 2018 leak of sale of user data.) and is currently peddling another capitalist mental health venture called CalmiGo (it is a 'smelling' divice that is supposed to help with anxiety and panic attacks but has absolutely no studies to back it and they have some very coercive wording on their website to goad people into spending money on something they can get in any other essential oil shop.

#capitalism is evil#don't waste what little money you have going for you on scammy mental health vultures

29 notes

·

View notes

Text

#postapoc#post apocalypse#wasteland#doomsday#larp#fashion#vulture community#vulture culture#nuclear fallout#nuclear winter#capitalism#anarchy#chaos#zombie apocalypse#apocalypse women

37 notes

·

View notes

Text

Is vulture culture mean to animals?

More people need to understand the difference between overconsumption and recycling when it comes to animal products. I am a bone collector and a furs collector but I refuse to buy from a fur farm-as should everybody-yet some people just don't understand how I could collect animal byproducts without doing that.

Pretty much I live in a mountain woods town and there is roadkill everywhere so it isn't hard to find bones. I only get bones from the ground (meaning already decomposed bodies with no flesh left and they are usually already pretty sun-bleached) and I would consider getting them from ethical hunters if I had the need (meaning hunters who kill animals to feed their family and never take more than they need, they usually use all of the animals and have no problem selling the carcass or the bones and fur if they have the time and energy to skin it themselves).

All of the furs (mostly tails) I have are from ethical farmers or roadkill, I only buy from trusted people who I know didn't get them from a fur farm or aren't a fur farm themself. Most of them are taxidermists (who by the way can be ethical about this too) who found roadkill or had to kill a fox that was eating their chickens or something and decided to use most of the body to honour the dead animal. Admittedly some things do go to waste though like the meat and guts, but in my experience, people usually leave them in the woods for the crows and vultures to eat (or small mammals sometimes).

This is how most vulture culture esc people I know do this and the majority of us do not give in to overconsumption of animal products.

It's actually better in my opinion to use all of the animals like our ancestors did rather than throw it out. Soooo next time you see someone wearing a tail on their backpack or who collects bones or something. Please don't just assume they are anti-vegans and hate animals or something because most of us actually love animals. For me, that's why I do this, to honour the poor dear or possum who fell victim to someone's car. And also remember that not everyone who is not a vegan or vegetarian is eating store-bought animal products, even if most of them are.

PS: I also think everyone should educate themselves on the overconsumption of animal products and think about their actions. I live in Canada so most of what I have learned pertains to that and the Hudson's Bay Company. But even just looking up the type of farm that beef you bought from the store came from is a good idea. If you are uncomfortable eating meat from a place like that, you should think about what you buy. This modern human world is full of overconsumption and disrespect for other animals, 'we' justify it by thinking humans are superior. But how can a species be so cruel and superior? The truth is they can't, we are animals just like the rest of them.

#vulture culture#taxidermy#animal bones#vegan#vegetarian#overconsumption#furs#ethical consumption#capitalism#anti-capitilism#no waste#zero waste

16 notes

·

View notes

Text

The tax sharks are back and they’re coming for your home

I'm touring my new, nationally bestselling novel The Bezzle! Catch me TODAY (Apr 27) in MARIN COUNTY, then Winnipeg (May 2), Calgary (May 3), Vancouver (May 4), and beyond!

One of my weirder and more rewarding hobbies is collecting definitions of "conservativism," and one of the jewels of that collection comes from Corey Robin's must-read book The Reactionary Mind:

https://en.wikipedia.org/wiki/The_Reactionary_Mind

Robin's definition of conservativism has enormous explanatory power and I'm always finding fresh ways in which it clarifies my understand of events in the world: a conservative is someone who believes that a minority of people were born to rule, and that everyone else was born to follow their rules, and that the world is in harmony when the born rulers are in charge.

This definition unifies the otherwise very odd grab-bag of ideologies that we identify with conservativism: a Christian Dominionist believes in the rule of Christians over others; a "men's rights advocate" thinks men should rule over women; a US imperialist thinks America should rule over the world; a white nationalist thinks white people should rule over racialized people; a libertarian believes in bosses dominating workers and a Hindu nationalist believes in Hindu domination over Muslims.

These people all disagree about who should be in charge, but they all agree that some people are ordained to rule, and that any "artificial" attempt to overturn the "natural" order throws society into chaos. This is the entire basis of the panic over DEI, and the brainless reflex to blame the Francis Scott Key bridge disaster on the possibility that someone had been unjustly promoted to ship's captain due to their membership in a disfavored racial group or gender.

This definition is also useful because it cleanly cleaves progressives from conservatives. If conservatives think there's a natural order in which the few dominate the many, progressivism is a belief in pluralism and inclusion, the idea that disparate perspectives and experiences all have something to contribute to society. Progressives see a world in which only a small number of people rise to public life, rarified professions, and cultural prominence and assume that this is terrible waste of the talents and contributions of people whose accidents of birth keep them from participating in the same way.

This is why progressives are committed to class mobility, broad access to education, and active programs to bring traditionally underrepresented groups into arenas that once excluded them. The "some are born to rule, and most to be ruled over" conservative credo rejects this as not just wrong, but dangerous, the kind of thing that leads to bridges being demolished by cargo ships.

The progressive reforms from the New Deal until the Reagan revolution were a series of efforts to broaden participation in every part of society by successively broader groups of people. A movement that started with inclusive housing and education for white men and votes for white women grew to encompass universal suffrage, racial struggles for equality, workplace protections for a widening group of people, rights for people with disabilities, truth and reconciliation with indigenous people and so on.

The conservative project of the past 40 years has been to reverse this: to return the great majority of us to the status of desperate, forelock-tugging plebs who know our places. Hence the return of child labor, the tradwife movement, and of course the attacks on labor unions and voting rights:

https://pluralistic.net/2022/11/06/the-end-of-the-road-to-serfdom/

Arguably the most potent symbol of this struggle is the fight over homes. The New Deal offered (some) working people a twofold path to prosperity: subsidized home-ownership and strong labor protections. This insulated (mostly white) workers from the two most potent threats to working peoples' lives and wellbeing: the cruel boss and the greedy landlord.

But the neoliberal era dispensed with labor rights, leaving the descendants of those lucky workers with just one tool for securing their American dream: home-ownership. As wages stagnated, your home – so essential to your ability to simply live – became your most important asset first, and a home second. So long as property values rose – and property taxes didn't – your home could be the backstop for debt-fueled consumption that filled the gap left by stagnating wages. Liquidating your family home might someday provide for your retirement, your kids' college loans and your emergency medical bills.

For conservatives who want to restore Gilded Age class rule, this was a very canny move. It pitted lucky workers with homes against their unlucky brethren – the more housing supply there was, the less your house was worth. The more protections tenants had, the less your house was worth. The more equitably municipal services (like schools) were distributed, the less your house was worth:

https://pluralistic.net/2021/06/06/the-rents-too-damned-high/

And now that the long game is over, they're coming for your house. It started with the foreclosure epidemic after the 2008 financial crisis, first under GW Bush, but then in earnest under Obama, who accepted the advice of his Treasury Secretary Timothy Geithner, who insisted that homeowners should be liquidated to "foam the runways" for the crashing banks:

https://pluralistic.net/2023/03/06/personnel-are-policy/#janice-eberly

Then there are scams like "We Buy Ugly Houses," a nationwide mass-fraud outfit that steals houses out from under elderly, vulnerable and desperate people:

https://pluralistic.net/2023/05/11/ugly-houses-ugly-truth/#homevestor

The more we lose our houses, the more single-family homes Wall Street gets to snap up and convert into slum properties, aslosh with a toxic stew of black mold, junk fees and eviction threats:

https://pluralistic.net/2022/02/08/wall-street-landlords/#the-new-slumlords

Now there's a new way for finance barons the steal our houses out from under us – or rather, a very old way that had lain dormant since the last time child labor was legal – "tax lien investing."

Across the country, counties and cities have programs that allow investment funds to buy up overdue tax-bills from homeowners in financial hardship. These "investors" are entitled to be paid the missing property taxes, and if the homeowner can't afford to make that payment, the "investor" gets to kick them out of their homes and take possession of them, for a tiny fraction of their value.

As Andrew Kahrl writes for The American Prospect, tax lien investing was common in the 19th century, until the fundamental ugliness of the business made it unattractive even to the robber barons of the day:

https://prospect.org/economy/2024-04-26-investing-in-distress-tax-liens/

The "tax sharks" of Chicago and New York were deemed "too merciless" by their peers. One exec who got out of the business compared it to "picking pennies off a dead man’s eyes." The very idea of outsourcing municipal tax collection to merciless debt-hounds fell aroused public ire.

Today – as the conservative project to restore the "natural" order of the ruled and the ruled-over builds momentum – tax lien investing is attracting some of America's most rapacious investors – and they're making a killing. In Chicago, Alden Capital just spent a measly $1.75m to acquire the tax liens on 600 family homes in Cook County. They now get to charge escalating fees and penalties and usurious interest to those unlucky homeowners. Any homeowner that can't pay loses their home.

The first targets for tax-lien investing are the people who were the last people to benefit from the New Deal and its successors: Black and Latino families, elderly and disabled people and others who got the smallest share of America's experiment in shared prosperity are the first to lose the small slice of the American dream that they were grudgingly given.

This is the very definition of "structural racism." Redlining meant that families of color were shut out of the federal loan guarantees that benefited white workers. Rather than building intergenerational wealth, these families were forced to rent (building some other family's intergenerational wealth), and had a harder time saving for downpayments. That meant that they went into homeownership with "nontraditional" or "nonconforming" mortgages with higher interest rates and penalties, which made them more vulnerable to economic volatility, and thus more likely to fall behind on their taxes. Now that they're delinquent on their property taxes, they're in hock to a private equity fund that's charging them even more to live in their family home, and the second they fail to pay, they'll be evicted, rendered homeless and dispossessed of all the equity they built in their (former) home.

It's very on-brand for Alden Capital to be destroying the lives of Chicagoans. Alden is most notorious for buying up and destroying America's most beloved newspapers. It was Alden who bought up the Chicago Tribune, gutted its workforce, sold off its iconic downtown tower, and moved its few remaining reporters to an outer suburban, windowless brick building "the size of a Chipotle":

https://pluralistic.net/2021/10/16/sociopathic-monsters/#all-the-news-thats-fit-to-print

Before the ghastly hotel baroness Leona Helmsley went to prison for tax evasion, she famously said, "We don't pay taxes; only the little people pay taxes." Helmsley wasn't wrong – she was just a little ahead of schedule. As Propublica's IRS Files taught us, America's 400 richest people pay less tax than you do:

https://pluralistic.net/2022/04/13/for-the-little-people/#leona-helmsley-2022

When billionaires don't pay their taxes, they get to buy sports franchises. When poor people don't pay their taxes, billionaires get to steal their houses after paying the local government an insultingly small amount of money.

It's all going according to plan. We weren't meant to have houses, or job security, or retirement funds. We weren't meant to go to university, or even high school, and our kids were always supposed to be in harness at a local meat-packer or fast food kitchen, not wasting time with their high school chess club or sports team. They don't need high school: that's for the people who were born to rule. They – we – were meant to be ruled over.

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/04/26/taxes-are-for-the-little-people/#alden-capital

#pluralistic#chicago#illinois#alden capital#the rents too damned high#debt#immiseration#chicago tribune#private equity#vulture capital#cook county#liens#tax evasion#taxes are for the little people#tax lien certificates#tax sharks#race#racial capitalism#predatory lending

351 notes

·

View notes

Last Seen Blogs

im-captain-basch

Memories of a Time Gone Past

portalnetbe

Portal Netbe.pl

dear-deer-faceart

Fatherless Behavior

divinesrival

𝒍𝒐𝒏𝒈 𝒘𝒂𝒚 𝒉𝒐𝒎𝒆

ikeda-eriza817

池田エライザ