#student insurance

Text

What are Insurance Coverage that Indian Students get in the UK?

Some of the oldest universities in the world are located in the United Kingdom. Its outstanding academic reputation, greater employment rate, wide selection of courses encompassing almost all subject areas, and shorter time when compared to other international learning programmes all contribute to its broad acceptance by students for their higher studies.

A lot of students from India every year migrate to the UK for their higher education. With exemplary education and various other benefits for international students, the UK government also provides students with access to free medical treatment through the national health insurance, called the National Health Service (NHS).

Now you may wonder why I am talking about student insurance in UK, as you don't have to take it compulsorily in India. The reason is that you cannot get treated if you do not have health insurance in the UK. Even for the slightest problem with your body, you need to have UK health insurance.

Now there are certain norms you need to fulfill for availing of government insurance in UK:

You are qualified for the NHS if you own a tier 4 student visa and thereby will be studying in the UK for more than six months.

And during the application for your UK visa, you have to pay the immigrant health surcharge (IHS), which costs around £500 a year in addition to the cost of the visa application, to get yourself insurance in UK.

The NHS covers accidents and emergencies, hospital treatments, family planning, and contraceptive services, for which you need not pay any amount of money.

Once you have landed in the UK, as part of the NHS, you will have to register yourself with a general practitioner. After registering with the GP, you will indeed be given an NHS number. Not waiting until you become ill is advised; register with a general practitioner as soon as possible.

Now, if you're traveling for studies, you will most certainly be eligible for getting the NHS, but suppose if you're traveling for less than 6 months in the UK. You will not get the National Health Service.

Now the question arises: how will you get treatment in the UK then? The answer to this question is "private health insurance." To begin with, there are a lot of private health insurances you can pick from, and if you want the best or are indecisive about which private Indian student insurance for UK, you need to pick for yourself, reach out to Remigos. Remigos is a cross-border payment platform that simplifies not just your payment methods from India to the UK but also provides services like assisting you in getting a UK SIM card or insurance in the UK, banks to choose from, and a lot more.

Now here are the reasons why you should opt for private health insurance:

When the overall waiting period for NHS care is longer than six weeks, you might use private health insurance to shorten the time you would wait.

You get a private room for yourself under the private health insurance, unlike in the NHS.

In contrast to the NHS, you can select a doctor and a facility that work with your schedule.

Those who have private health insurance can avoid having to spend a long time waiting for non-urgent operations.

So if you have planned your migration and are to fly to the UK, make sure that you are prepared for everything you need, and don't forget to get yourself health insurance, whether private or on the NHS. For further help managing your monetary transfers, you can always reach out to Remigos.

2 notes

·

View notes

Text

arguing with a friend over not all zoomers abandoning normal wallets. i love my george costanza oversized dad wallet. how could you not love a pocket office...

let me hear your wisdom in notes!!!

#so sick of these god damned single nonfold wallets#and especially these super shitty metal clip wallets#all your money showing to the world#two card capacity#i want to carry EVERYTHING#my driver's license my občanka my 3 debit cards my 2 insurance cards my student id my public transport cards my#poll

7K notes

·

View notes

Text

vimeo

International Student Insurance helps you save your hard earned money in case your child needs medical assistance while studying in Canada. International students studying in Canada are not covered by any provincial or territorial insurance and their native insurance will not cover them as well.

Avoid heavy medical bills with International Student Insurance. Insurance Gully is one of the reputed and trusted insurance brokers across Canada. We provide the best coverage at the best rates and specialize in the claim filling process. Get in Touch Now!

For more information:

Visit our website - Student insurance Canada

0 notes

Photo

Student insurance

Raizing One travel insurance was founded with the intent of serving the globetrotters worldwide. We provide travel insurance packages for thousands of business leisure travellers, as well as, international scholars to protect them and their families from any miss happenings or incidents.

0 notes

Text

Retirement Meditation - Should I take an in-service withdrawal from my retirement plan?

Author: Paul A. Carl, CHSA, CPFA™ Vice President, Retirement Plan Consulting, Registered Representative

The plan administrator called with a dilemma. A critically important employee stood in her office holding a foreclosure notice. Because the company’s retirement plan permitted neither participant loans nor hardship withdrawals, the employee threatened to quit to get a 401(k) distribution. Additionally, as a matter of policy, the company itself did not make loans or payroll advances to employees. The plan administrator wanted to know what other plan options might be available. A little investigating and it turned out that the 401(k) plan did allow in-service withdrawal of rollover money. The employee had rolled over a previous employer’s 401(k) plan into this company’s plan. The questions now became: How much to withdraw? What would be the tax effects? Did the employee want to permanently remove funds from his accumulated retirement savings?

Some plans offer no in-service withdrawal options while others offer three or more. The most popular in-service withdrawal types are:

Hardship withdrawals

Age 59-1/2 in-service withdrawals

Contribution-source specific withdrawals, such as in the example above

Plans offering hardship withdrawals most often adopt the IRS safe harbor standards for allowing participants to take a hardship withdrawal. By following the IRS safe harbor standards, the plan administrator is limiting hardship withdrawals to certain reasons and creating a fiduciary safety-net in the administration of the hardship provisions.

Plans offering age 59-1/2 in-service withdrawals permit participants aged 59-1/2 or older to take distributions from their retirement plan while they continue employment. These distributions can be rolled over into an IRA or taken as taxable. The key factor? At age 59-1/2, the 10% excise tax penalty on early withdrawal no longer applies. However, personal income taxes can and will apply to taxable distributions.

Contribution-source specific withdrawals are most often related to the rollover source. These are plan assets the participant electively rolled into the employer’s plan from an IRA or a former employer’s plan. Most often, but not always, the plans designed to permit incoming rollovers will also allow those rollover funds to be withdrawn at any time. They can be distributed into an IRA with no tax consequences, or they can be taken as taxable. If the participant taking the taxable in-service withdrawal is younger than age 59-1/2, the 10% tax penalty (and personal income taxes) will apply.

Regardless of the type of in-service withdrawal, the biggest issue for most participants is the permanent removal of accumulated retirement savings. In-service withdrawals, especially those taken as taxable, are effectively removed from the participant’s retirement savings, which could cause a later hardship especially as the participant nears or enters retirement. Remember, these funds taken as taxable distributions are no longer available to earn future growth and no longer available at retirement.

Will you let your retirement savings success be hampered by an in-service withdrawal?

For more details, Contact us today

HORAN

7475 Paragon Rd

Dayton OH 45459

937-610-3700

https://horanassoc.com/

#Employee benefits consulting#wealth management#retirement plan consulting#life and disability insurance#individual health insurance#medicare#student insurance

0 notes

Note

Are you still active on tumblr?

YES I am!! Sorry friends for dropping off the face of the earth, I got a job and I had to move and it was a lot. But I am less stressed now and I hope I can get back to posting more regularly!! I really missed it (ノ^ヮ^)ノ*:・゚✧

I will never leave tumblr because there is no other place on the internet where I can tell people that 80% of the time when I try to introduce myself to someone in the office that I haven’t met yet I get so focused on smiling and holding eye contact that I forget the part where I actually have to introduce myself (°□°)

#HELLO FRIENDS#how are you!! I missed you! ᕕ( ᐛ )ᕗ#I hope you all had a good summer!!#mine was very nice even though there was a lot of stress and new things happening#suddenly there were so many adult things in my life that at the end of the day I just sat on the couch and watched decorating shows#I love decorating shows but today they showed this decorating competition and one woman had to decorate her whole bedroom coral#and then I knew it was time to go back#friends I've done so many new things the past few weeks!! I've really underestimated what this new chapter of my life would be like#it's very nice and I'm glad but I've never thought about things like insurance and taxes and parallel parking before#and I'm in a new apartment and everything!! ✧⁺⸜(●′▾‵●)⸝⁺✧#it is a very good apartment but the landlord left us so many of their chairs#this does not sound like a problem but we also owned chairs before#so our chair number is doubled now#the kitchen is full of chairs the balcony is full of chairs#I've hidden two chairs behind the TV but I can still see their chair heads and then I feel bad because they do not deserve this#they should be roaming free#also rode a BIKE#they say you never forget how to ride a bike#but my secret is that I never really knew how to ride one#in Germany all students have to do a bicyle test in fourth grade and I was so bad that my teacher asked me#afterwards if I had tried to confuse the other students#I just said 'uh yes' and then he said ok and I passed with the worst bicyle grade of the whole school#I hade made 8 bicyle mistakes#I hope you're doing well friends!! see you soon!!#have a nice day :)

2K notes

·

View notes

Text

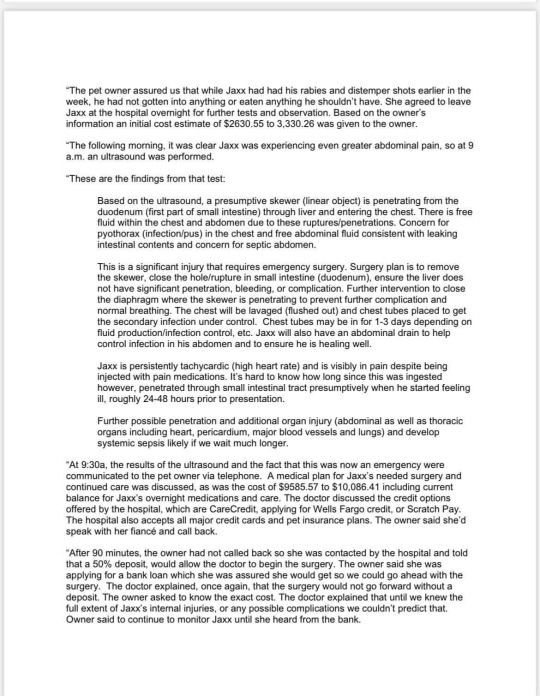

This could be me. This could be one of my colleagues, one of my classmates, one of my friends. It’s understandable that the original owner is upset over losing her pet, but what she’s done in retaliation is despicable, as is the news station that ran this story smearing our profession. Veterinary professionals should be able to go to work without facing graphic threats of violence against them and their families in return for saving a life in an impossible situation. You wonder why veterinarians and their support staff have such obscenely high rates of depression and suicide? This is why.

If you have a pet, I’m begging you to come up with a financial plan for their veterinary care. Get pet insurance (especially if you’re getting a new puppy or kitten). Start an emergency fund. Have a credit card set aside specifically for this kind of situation. Apply to CareCredit or a charitable fund like the University of Tennessee’s AlignCare if you find yourself unable to cover a bill. Most people don’t have immediate access to $10,000 (which is a reasonable price for the intense level of care this puppy required), so you have to have a plan. And don’t go buy an expensive purebred puppy and then claim you don’t have any money for vet care.

Be kind to your veterinarian. We are hundreds of thousands of dollars in debt from our education while making far less than our human healthcare counterparts. If we were in it for the money, we would have chosen any other career.

#I cannot recommend pet insurance enough#not one more vet#maine veterinary medical center#vet bills#veterinary#vet med#veterinarian#emergency vet#vet tech#vet nurse#vet student#vetblr#pets#pet owners#pet health#dogs#cats

3K notes

·

View notes

Text

When you’re burnt out from working 80 hours a week and on the edge of losing your damn mind from sleep deprivation but then someone gives you a small snack or you have time to sit down and drink a cup of water:

Today I had the chance to drink a whole cup of water between OR cases and I almost cried of happiness. When the highlight of your day is that you had the chance to pee once, something is wrong.

Residents like me work 80 hours a week (sometimes more) for what calculates out to be less than minimum wage because this is how residencies are structured and because we are the last line between patients and unsafe care. You didn’t hire enough nurses? Have the resident remove/place foleys and NG tubes. You didn’t hire enough transport staff? Have the resident transport patients. I can’t in good conscience let my patients have less than the standard of care, but it becomes unsustainable when you don’t have enough staff. To top this all off, my hospital CEO got a raise of millions of dollars this year, but my raise to next year doesn’t even keep up with inflation. People justify this treatment of residents by saying that oh well we will be rich when we’re attendings, as if having a higher salary in the future justifies this kind of exploitation. I know residents right now who are struggling to afford healthcare for their children, who struggle to find affordable housing within the area we are required to live because of home call. There is simply no justification for the amount of work we do compared with our pay (or the hours we work period).

Maybe this is just a long way of saying please be kind to residents in the hospital. We work really hard within a really broken system and care a lot about our patients.

#medical school#residency#medstudent#medschool#medicine#medicalstudent#medical student#healthcare#resident doctors#physician#covid 19#covid19#doctor#surgery#burnout#insurance#health insurance

297 notes

·

View notes

Text

I'm so proud of myself about finances in the past couple months. I still struggle with money but I did enough meditation and journaling and practicing about it to make myself able to actually face my loans and credit cards and savings and bills and start really truly organizing and addressing them for the first time in years instead of just flying by the seat of my pants.

Like. This is a huge deal for me. I've felt like I'm in deadly danger every time I've tried to think about money for years and years. I'm finally able to look it in the face and stare it down and start to organize and plan on purpose instead of just keeping up with the minimum to stay afloat. I'm so proud of myself.

It's still a refrain of "GUILT (funny link)" every time I think about money but I'm able to actually make spreadsheets and face the numbers and monthly tracking again, and even make a new full budget which I haven't been able to do in ages.

still feel guilt, overwhelm, and helplessness, but no longer feel as much deep elemental shame and terror. that's progress baby

#we don't need to talk about how many months and months of therapy visits and doctor appointments I put on credit cards#among other things#but I had to put my foot down about it a couple months ago and shout at myself a little saying HEY#I AM SHAKING YOU BY THE SHOULDERS I AM SHOUTING FOR YOU TO HEAR#OF COURSE IT WAS A TERRIBLE FINANCIAL DECISION BUT YOU WEREN'T EVEN EXPECTING TO BE ALIVE#THE CREDIT CARD DEBT WAS NECESSARY TO KEEP YOU ALIVE AND IT DID AND EVERYTHING ELSE IS WAY LESS IMPORTANT THAN THAT#why the FUCK are you feeling SO ASHAMED for making the best decision you knew how to make at the time???#just because you know NOW that you could have tried some other options doesn't mean you did THEN#you may have known enough to feel shame and guilt yes but you would never in a million years have gotten the help you needed fast enough#by attempting to go another route#you didn't trust anyone besides a very few handfuls of people and even them it wasn't fully#and the stress of running it through parental insurance was so terrifying to you bc you didn't know what that would do#and you never had cosigners for anything your whole adult life. it's OKAY#you fucking DID YOUR BEST#YOU HAVE LEARNED. YOU HAVE MADE CHANGES. YOU HAVE ALREADY DONE BETTER#YOU WILL CONTINUE TO LEARN AND IMPROVE OVER TIME#it is not the end of the world. even the utilities sending you to debt collections etc etc#YOU ARE FIGURING IT OUT ONE PIECE AT A TIME#MORE PEOPLE ARE ASHAMED AND AFRAID OF THEIR OWN FINANCES THAN YOU THINK#if the people who fought and argued with and shamed you for considering student loans much less taking them out#had wanted you to actually be financially safer and healthier#they could have just fucking helped out or cosigned your loans or actively helped you find other solutions#instead of spending months and months telling you it was the worst decision ever and would ruin you financially for decades and such#you made the best decisions you could with the level of terror and knowledge that you had. it was enough to keep you alive.#isn't that enough?#isn't it a victory to survive?? isn't that enough??????#god i'm cringing at sharing this but if it's been this hard for me surely at LEAST one of you has also made financial mistakes or regrets#and seeing me be honest that I fucked it all up too and it's a mess and I'm just climbing back through it as best as I can as I go#will hopefully make at least one of you feel a tiny bit less alone

37 notes

·

View notes

Text

like, I'm old school web comic culture, I like handmade zines that are stapled, I just want to make comics and tell stories and the ranking system of the popular webcomic sites exhaust me to my core, which is why I like tumblr. I want to draw sulla wound fingering crassus and not think about the metrics.

#that said i'm a pretty avid reader of korean webcomics and chinese webnovels when i have the money for it#unfortunately i have not had the money for that kind of thing in like. six years RIP#its part of why i dont really plan to paywall my stuff. i want to like. connect somehow. and thinking about a historical fiction comic#in terms of 'is this something someone will pay for?' over 'this is something i FELT in my BONES' kills me#and i do not mean that as an exaggeration. for like two years i was an art industry artist and it did serious critical infrastructure damag#to me. i do commissions and freelance gigs to pay the bills but all i want to do is draw comics#and hopefully! i will make comics that people will want to support through patreon or something like that!#because i would love to not think about trying to pay my bills with this but unfortunately i have student loans#also eventually i would like health insurance. tbh. or actually. dental insurance.

91 notes

·

View notes

Text

getting school emails during summer break is so evil like. begone dragon i will vanquish you in the autumn

67 notes

·

View notes

Text

truly humbling to go from gifted kid and top of my high school class to only kid accepted to ivy league school to graduating with honors and one of two students to go onto a PhD program to president of your field’s professional association to the idiot who took eight years to graduate and the only graduate you know to be unemployed with zero job prospects after finishing said PhD program

#i have lost track of how many students have come and gone through my lab but i do remember every. single. one. of them had a job lined up#and here i am#having one of those nights where i feel like a total loser with a capital L don’t mind me#also all my friends are saying things like ‘trust the process’ and ‘enjoy the time off’#like i’m sorry i’m stressed but i have bills to pay and have a major medical procedure coming up that i’m barely insured for#i’ve been making grad student wages for EIGHT YEARS. i do not have a nest egg. i don’t want to ‘trust the process’#anyway i’ve gone from complaining about school to complaining about not school but that’s what happens when you’re feeing like a Loser#tbd

12 notes

·

View notes

Text

#student loans#war#israel#palestine#free palestine#end occupation#genocide#ethnic cleansing#gaza strip#Gaza#free Gaza#Wedt Bank#occupied palestine#occupied west bank#apartheid#healthcare#health insurance#reality#United States#silence is complicity#war crimes#America#amerikkka#United States of America#USA#they got money for wars#money for war#holy land#holy wars#palestinians

20 notes

·

View notes

Text

HORAN offers Personalized Health Insurance Options for Students

College students today face growing challenges, many of them related to physical and mental health. The COVID-19 pandemic has brought students’ mental health issues into the spotlight, with many students facing anxiety and depressive symptoms to worrying degrees.

To help students across the country live healthier lives, colleges and universities have a chance to enact lasting change by offering a personalized health insurance experience.

Our team at HORAN Campus Health Solutions can help you evaluate your plan offering and determine if you are providing the most meaningful coverage and value for your students.

Contact us:

HORAN

7475 Paragon Rd

Dayton OH 45459

937-610-3700

https://horanassoc.com/

1 note

·

View note

Text

Just went in to take the toughest anatomy test of the semester (multiple choice, for lecture) that I only kinda prepared for and have like 7/10 migraine type headache pain and somehow managed an 82. I will take it and run thank you very much.

Somehow I'm going to survive this semester, although not unscathed. This pain is unreal lately.

#spoonie#chronic illness#my post#disability#disabled student#insurance can feel free to approve my pain management procedure ANY DAY NOW#hashtag suffering for no reason squad#fibro

34 notes

·

View notes

Text

if you are 1) currently in a university where your student healthcare covers hormone therapy, and 2) in a good financial, emotional, and social position to start hormone therapy, i would recommend pursuing it. because in my experience, it's a huge pain in the ass to get an endocrinologist once you're on your own

#unless you live near a planned parenthood or another equivalent to that#but in general you might as well take advantage of the mandatory student health insurance while you have it#it's also cheaper than you might expect. my vials cost $40 CAD for 4 months and then the injection materials are like a couple dollars each#for me i got a therapist with the university and asked them to recommend me to one of the uni's doctors#so i got to skip some of the waitlisting process yay#and then even after getting access to hormones i went to the clinic maybe 5 or 6 times because i needed a nurse to help me with injections#all of which was 'free' because it was with the university#now that i'm graduated though i need to find a new endocrinologist and it turns out the process is WAY more complicated on your own 🤡#of course your mileage may vary depending on how based your school is but it's definitely worth checking imo 🤷#beepbeep.txt#wanted to say this because i basically didn't use the uni health services until my last year and i was like 'wow#'i'm actually getting so much shit for free right now'#like i was seeing a therapist and a dietician and the endocrinologist and a nurse simultaneously at one point#and i might've missed out on all that if i didn't have someone tell me how easy it was to get help if you ask the right questions#so there's my word of wisdom for anyone who might benefit from it.......#also going to post tips about injections later because i think that would also help people out 👍

27 notes

·

View notes

Last Seen Blogs

letmeseeintothefuture

♡Let me see into the future♡

heatheaders

book headers.

catgnawdotcom

CATGNAW

being-a-bitch-is-mykink

I just want to be thin

scotlong-blog

50x Their Weight