#Financial Literacy

Text

DO NOT VOLUNTEER TO BE A CO-SIGNER OR GUARANTOR FOR SOMEONE ON TUMBLR.

I just saw a 'mutual aid' post going around where instead of asking for donations, the person was asking someone to be a "guarantor" - also known as a "co-signer" - for their rent.

DO NOT DO THIS.

I am all for mutual aid. I think credit scores are a scam designed to fuck poor people. I get it. I do. BUT. Being a guarantor/co-signer for someone basically means that if they don't pay what they owe, for whatever reason, their landlord, bank, creditors, etc. can and will come after you for the full amount.

It seems like such an easy way to help someone. You don't need to pay any money, just lend them your name and good reputation so they can get permission to borrow and spend their own money. It feels like you're getting one over on the shitty capitalist system and using your privilege of good credit/income to help someone else.

But it is a HUGE risk. Do not do this. All it does is give that shitty system more ways to get their hooks into you and create tons of problems for you down the line.

You can really fuck yourself over in the long run by getting tangled up in a financial situation like this. Even co-signing for someone in your life who you trust, like a sibling or a parent, can be really risky. No matter how much you trust someone not to purposefully leave you holding the bag, now you're on the hook if they end up with financial problems neither of you anticipated.

Do not co-sign for another person's loan, car, rent, etc. unless you are able and prepared to pay the full amount or subject yourself to the mercy of whatever that person gets themselves into.

ESPECIALLY do not do this for someone on the internet, where scams are rife. Do not share your personal information with people online and NEVER allow someone else to use your personal information for their finances.

Here is an article with more information.

19K notes

·

View notes

Text

{ MASTERPOST } Everything You Need to Know about Saving Money and Being Frugal

We’re all in this together. Don’t give up.

On food and groceries:

How to Shop for Groceries like a Boss

Why Name Brand Products Are Beneath You: The Honor and Glory of Buying Generic

If You Don’t Eat Leftovers I Don’t Even Want to Know You

You Are above Bottled Water, You Elegant Land Mermaid

You Should Learn To Cook. Here’s Why.

On entertainment and socializing:

The Frugal Introvert’s Guide to the Weekend

7 Totally Reasonable Ways To Save Money on Cheap Entertainment

Take Pride in Being a Cheap Date

The Library Is a Magical Place and You Should Fucking Go There

Your Library Lets You Stream Audiobooks and eBooks FOR FREEEEEEE!

What’s the Effect of Social Media on Your Finances?

You Won’t Regret Your Frugal 20s

On health:

How to Pay Hospital Bills When You’re Flat Broke

Run With Me if You Want to Save: How Exercising Will Save You Money

Our Master List of 100% Free Mental Health Self-Care Tactics

Why You Probably Don’t Need That Gym Membership

How to Get DIRT CHEAP Pet Medication, Without a Prescription

On other big expenses:

Businesses Will Happily Give You HUGE Discounts if You Ask This Magic Question

Understand the Hidden Costs of Travel and Avoid Them Like the Plague

Other People’s Weddings Don’t Have to Make You Broke

You Deserve Cheap, Fake Jewelry… Just Like Coco Chanel

3 Times I Was Damn Grateful for My Emergency Fund (and Side Income)

When (and How) to Try Refinancing or Consolidating Student Loans

The Real Story of How I Paid Off My Mortgage Early in 4 Years

Season 2, Episode 2: “I’m Not Ready to Buy a House—But How Do I *Get Ready* to Get Ready?”

The Most Impactful Financial Decision I’ve Ever Made… and Why I Don’t Recommend It

On buying secondhand and trading:

Almost Everything Can Be Purchased Secondhand

I Am a Craigslist Samurai and so Can You: How to Sell Used Stuff Online

The Delicate Art of the Friend Trade

On giving gifts and charitable donations:

How Can I Tame My Family’s Crazy Gift-Giving Expectations?

In Defense of Shameless Regifting

Make Sure Your Donations Have the Biggest Impact by Ruthlessly Judging Charities

The Anti-Consumerist Gift Guide: I Have No Gift to Bring, Pa Rum Pa Pum Pum

How to Spot a Charitable Scam

Ask the Bitches: How Do I Say “No” When a Loved One Asks for Money… Again?

On resisting temptation:

How to Insulate Yourself From Advertisements

Making Decisions Under Stress: The Siren Song of Chocolate Cake

The Magically Frugal Power of Patience

6 Proven Tactics for Avoiding Emotional Impulse Spending

On minimalism and buying less:

Don’t Spend Money on Shit You Don’t Like, Fool

Everything I Know About Minimalism I Learned from the Zombie Apocalypse

Slay Your Financial Vampires

The Subscription Box Craze and the Mindlessness of Wasteful Spending

On saving money:

How To Start Small by Saving Small

Not Every Savings Account Is Created Equal

The Unexpected Benefits (and Downsides) of Money Challenges

Budgets Don’t Work for Everyone—Try the Spending Tracker System Instead

From HYSAs to CDs, Here’s How to Level Up Your Financial Savings

Season 2, Episode 10: “Which Is Smarter: Getting a Loan? or Saving up to Pay Cash?”

The Magic of Unclaimed Property: How I Made $1,900 in 10 Minutes by Being a Disorganized Mess

We will periodically update this list with newer articles. And by “periodically” I mean “when we remember that it’s something we forgot to do for four months.”

Bitches Get Riches: setting realistic expectations since 2017!

Start saving right heckin’ now!

If you want to start small with your savings, consider signing up for an Acorns account! They round up your every purchase to the nearest dollar and save and invest the change for you. We like them so much we’ve generously allowed them to sponsor us with this affiliate link:

Start investing today with Acorns

#frugal#saving money#personal finance#money tips#financial tips#financial literacy#financial freedom#money#debt#money management#how to save money

354 notes

·

View notes

Text

How I Built an Emergency Fund, inspiration I deeply hope is helpful

As the blog URL says, this is not financial advice. This is how I did this thing, and I am posting it here, publicly, in hopes that it helps you should you need this information.

In short: Remix this advice to what fits your life + do not sue me if this goes poorly for you. This is for Americans, if you do not live in America and/or your money is not in America, I hope this is a useful base.

None of these links are affiliate links.

I write these things as a mental shift. I like to ramble and I wish I had someone tell me this stuff 20+ years ago. I'm hoping this helps you.

This is an incredibly long post so I'm putting it under a KEEP READING.

This post goes over two stages: "short term + not life-or-death" and "long term + actual life or death"

Part 01: SHORT TERM + NOT LIFE-OR-DEATH FUND

You need to find a high yield savings account that is FDIC insured. Ally is a popular bank for this.

Functionally, the only difference between a "high yield savings account" and "savings account" from the giant conglomerate bank down the street is the interest rate.

I do not know why non-high-yield savings accounts exist. I'm guessing because legally they can, and I hate it.

Moving away from my personal socioeconomic views to return to advice.

"FDIC insured" is not something you pay for. It is nearly universal on savings accounts. If a savings account, or a checking account, does NOT have it, then you should not put your money there. Something is wrong with that bank.

FDIC means if your bank goes out of business, your account is insured up to $250,000, per account, by the government. So if your bank goes out of business, the government makes sure you still have your cash (up to $250k).

A high-yield savings account means your cash is available whenever you need it.

Other products, like CDs, exist, but this ramble is designed to be as simple and starter as possible. Begin with a high yield savings account, build up from there as you do your own research + compare this to your needs.

Do not accept an account that has minimum balances. Do not open an account with monthly fees.

Touch this account as little as possible.

For every $1 you put in, every month, a few pennies will materialize. It's not much, but the main point is at every level, your money works for you.

Rich people do this. You can too.

Touch this account as little as possible.

You can have multiple savings accounts.

I personally have a savings account in the above structure designed for "oh hell I am kinda screwed, but will be okay, just need a buffer."

"How much should I have in there?" you might ask. Common advice says "3-6 months expenses" which is a lot. I say "start with literally $1 and continue as you can until comfortable with what is possible, for you, at this time."

Will $1 make you rich? No.

Will it save your life in a bad situation? Probably not.

Does this $1 essentially become a tiny robot that is making you money for as long as it is docked into its cargo bay? ...weird metaphor but we'll go with it, sure.

Ultimately is it a start? Yes.

You can have multiple savings accounts. You can have a savings account "this is for short term emergencies" and "this is for... slightly less short term" etc.

It costs you nothing to have multiple. They all operate in the same way. It's handy to have them all at the same bank because it can make transferring cash easier.

Part 02: LONG TERM + ACTUAL LIFE-OR-DEATH FUND WITH RISK SO BE CAREFUL

Once you have your savings account set up, and it's being funded on a regular basis (every week, every paycheck, every month, every quarter -- whatever works for you), look into creating a second, bigger, more dangerous-term cash reserve.

I like my Roth IRA. This is a link to a proper finance blog that has a lot of details. I am trying to make this handy/simple to get started.

401ks and (non-Roth) IRAs are funded with pre-tax dollars, frequently in conjunction with your job.

Normally, cash goes from job -> government takes a slice -> you.

Pre-tax retirement accounts, cash goes from job -> retirement takes the percentage you decide -> government takes a slice of what is left -> you

Roth IRAs, job -> government takes a slice -> you -> Roth IRA

The benefit to pre-tax retirement accounts being, because the cash going in is pre-tax, there is more of it.

It can grow faster in the stock market or other places your particular fund allows you to put cash into.

The taxes come out when you withdraw -- usually retirement -- because if you withdraw before you retire, you are heavily penalized with extra fees.

That's why Part 02 is a ROTH IRA. Your money has already been taxed -- job -> government's slice -> you -> Roth IRA.

This means the money is yours, already taxed. If you withdraw the gains, those get taxed, but the base, that's yours.

If you invest $100 and it grows to $105, you can withdraw $100 without paying fees or taxes. If you withdraw that extra $5, that is when taxes start to come into play. If you withdraw $100, and leave the $5, the $5 continues to grow, and that extra growth is taxed if withdrawn. So try not to touch it (ideally you leave all of it until retirement).

This is why this is an emergency, life-or-death only, account. You tap it only when you need to when all other choices are wretched and ruinous.

There is an annual limit as to how much money you can put into a Roth IRA (several thousand bucks).

You can start them very small. Like $20 or maybe less.

Look for a bank or institution that does not charge fees to open and maintain one.

AT EVERY STEP YOU SHOULD BE AVOIDING FEES

Here are smart people talking about ideas on how to get started.

Okay, so, what do we do now with this fancy roth thing.

Here is where things get... uncomfortable.

A Roth IRA is an account type.

You need to do something with your money.

The reason you have this in addition to, and secondary to, your high-yield savings account is because this is an investment vehicle, the balance is going to go up and down, and may reach $0.00.

For my Roth IRA, I like "exchange traded funds" -- ETFs.

There are a lot of options -- you can invest in most anything

Because my Roth IRA is built for "help me I'm dying" emergencies, I invest in a mix of S&P 500 index funds and small-cap funds.

SO MANY WORDS.

Let's break this down what this means.

S&P 500 index funds: This is an index fund of giant, giant, giant companies.

An index fund is like a stock. But instead of a single company, it tracks (owns shares of) an index -- like the DOW or Nasdaq. Or countries. Or... the entire market for oil. Etc.

The metaphor isn't completely accurate, but I like to think of it as "an index fund is a company that owns tiny bits of other companies."

Like, okay, say you have SlimeIndexFund and a share price is $40.

In this example, SlimeIndexFund owns $10 worth of "BardCo" and $10 of "ThiefCo" and $10 of "MermaidCo" and $10 of "EvilCo".

Let's say EvilCo does a lot of evil and is now worth $15, and MermaidCo does a lot of mermaid stuff and is now worth $15, and BardCo sings out of tune so is now worth $5. ThiefCo is oddly at the same $10 but we're scared so we're leaving ThiefCo to stay at $10.

A share in SlimeIndexFund is now worth $45. ($5 BardCo + $10 ThiefCo + $15 EvilCo + $15 MermaidCo)

This is diversification

Because I bought an index fund, instead of just buying BardCo, my risk is less.

Had I bought all MermaidCo, my return would be higher -- but this is a much bigger risk.

The entire purpose of this set up of a Roth IRA is TO MINIMIZE RISK.

Your Roth IRA should allow you to buy "fractional shares" and if it doesn't fuck that bank, go somewhere that does.

In the above example, SlimeIndexFund is $40/share and at that price you are getting the full benefit of 1 share.

Let's say you have $10.

You buy a fractional share of SlimeIndexFund for $10, which is 25% of 1 share.

So when SlimeIndexFund shares raise from $40 -> $45, your fractional share goes from $10 -> $12.50.

Not all funds and stock shares (etc) have fractional shares, most do.

It's a great way to start and build.

Small-cap funds: These operate in literally the same way. The difference is the companies are (in comparison) much smaller. They tend to be more nimble.

So I am diversifying between "here is a fund, it has a lot of large companies" and "here is a fund, it has a lot of small companies."

Let's say Big Office Building real estate goes down, but the sale of Small Company Making waffles goes up. This mixes together and I'm less in danger of losing money, or losing much money.

You can pick individual stocks.

The reason it is not recommended, by nearly everyone, is because the market has incredible tools and power over individual stocks.

By using any kind of fund that bundles things together, you are thereby automatically using these tools by proxy

It is critical to understand this is the stock market. Your account will go up and down. It may go down A LOT, like 25%, and take years to recover. Maybe it goes down 100% to literally $0.00.

That's why this is the LAST RESORT EMERGENCY FUND.

So why are we doing this.

This feels... wrong?

The potential for growth is significantly higher than a savings account. Adjusted for inflation, somewhere in between 6-7%.

At this rate, if you can leave your initial deposit alone for somewhere between 10 - 13 years, it has doubled.

This equation recalculates every time you make a deposit. So if you can deposit $20 every pay check, it has the potential to grow very quickly.

As above, this is the stock market, so it can also get wiped out.

But given the stock market has historically always recovered, though it may take several years, the risk is worth it to me + a lot of other people.

The reason this is built as a last-resort cash bucket is because of this risk. Before moving into this arena, you should have other cash buckets as a buffer.

Your RISK is it goes down. Which it will frequently.

Your REWARD is if it goes up. Which historically it has far more than it went down.

The PURPOSE of using funds as described above is so you don't have try to guess who the next Amazon is and wind up picking the next Pets.com (which went out of business, like, a long... long time ago).

The people making the funds figure out who is Amazon and who is Pets.com and work, day and night, to make your money grow and/or protect it when outside influences are hurting the market.

They are incredibly equipped to do this and their literal livelihood is on the line when they do it poorly.

Which is a polite way of saying, they are continuously incentivized above all else to work for the fund you're investing in.

The reason you're doing this in a Roth IRA specifically is you're hoping to keep as much of it intact, as possible, until you retire, at which point -- if you've followed fairly simple rules -- you withdraw the base and gains tax-free.

Whereas money in a normal stock account? Those gains are taxable every year.

"I have literally $20 I can save per pay check! Can I put in $15 into a high-yield savings account and $5 into a Roth IRA to get started?!"

Yes!

Also, congrats! You're diversifying already!

Your Roth IRA broker should allow you to invest a minimum of $1 at a time, and buy fractional shares. If they don't, don't sign up with them!

Lean heavily into your high-yield savings account until that is very comfortable and thick, then push money into the Roth IRA.

Your goal is to build a system that works for you -- both literally (money working for you) and emotionally ("this is comfortable")

"Should I pay off debt before proceeding? A lot of people say to pay off excess debt first."

This is up to you.

Most financial blogs etc. do say "focus on paying off debt first" -- it's good advice, your returns are risk-free and permanent, since the lower your debt is, the less you have to pay over time.

Interest -- working for you or against you -- is continuous and eternal.

Personally, I like to diversify everything, so I not-financial-advice ramble "do all three -- pay down debt, throw a little cash into a high-yield savings, throw a little cash into a Roth IRA"

The problem with "pay off debt first" is that it misses out any occasional giant gains the stock market makes (Roth IRA) and introduces the risk of "I have paid this credit card on time for 5 years, I'm short on change for 3 months due to a situation that gets resolved quickly, and now I have a late payment fee, and a higher interest rate."

Look at your life, finances, and potential future and make decisions!

And also:

Always be on the look out for deals with banks. Sign up bonuses, referral links from friends, etc. Think of it as a money sale.

If you are not comfortable with the idea of a Roth IRA hitting $0.00 potentially, do not do step 02. These are ideas, not directives.

All financial tools can be used for different purposes. All of them. Thus -- these are ideas, not directives.

I am listing a few examples of banks, funds, etc. These are not recommendations nor are they affiliate links. They are listed because I want to maximize your start on this path, but caution, in strongest possible terms, you must do your own research and figure out what makes sense for you.

There are a lot of nuances I am paving over for the sake of simplicity, which is why I am continually saying...

...c'mon say it with me...

...you must do your own research before continuing

Smart, free sites that cover this + a lot of other stuff:

NerdWallet

Bank Rate

One final note about Roth IRAs:

Robinhood currently is offering a 1% match on an IRA. Considering the strict limits of how much an IRA can intake per year, it's not much, but it doesn't cost you anything. Money on sale!

As a final note -- always feel comfortable asking people handling your money for help. They are working for you. Your money works FOR YOU.

If you are uncomfortable, leave, immediately, without concern.

At the retail level, there are hundreds of banks and financial institutions clamoring for your business. If someone makes you uncomfortable for not knowing something, or getting a term wrong, or asking "too many" questions -- go somewhere else.

It doesn't matter if your account is literally worth $20.

They are working for you.

This is a business transaction, and if they make you feel like your time isn't worth their business, I promise you there is someone else who will gladly take care of you.

I end with -- whenever someone is giving you financial advice, always ask why. It helps ensure they aren't scamming you, it's just a good business practice.

I like to ramble, it helps me mentally

I like to be useful, I want the world to be significantly more balanced in terms of who is doing okay

I like to write, this is all good practice for me in doing Various Other Things I do

I fucking hate predatory financial practices. I was gatekept out of financial literacy for decades and so every time I help someone else figure out how to set up their own life and protect themselves it is a giant "fuck you" to the systems and directly to the people who stood in my way.

562 notes

·

View notes

Note

Can you give an example of what you write for your goals? I want to start, but I'm not exactly sure how to write it

For example:

~FINANCIAL GOALS~

(Short term 1-3 months)

1. Get promoted at work & negotiate a 50% raise

2. Cut any excess spending (gym membership/phone bill/etc.)

3. Increase emergency fund to X,XXX

(Medium term 3-6 months)

4. Refinance car loan

5. Make more money —> Launch side hustle

6. Open another line of credit (discover/capital one?)

(Long term 6-12 months)

7. Pay down private student loans AGGRESSIVELY

8. Increase emergency fund to $XX,XXX

9. Grow social media fan base —> sponsors

10. Contribute max amount to 401k & Roth IRA

Etc. Etc.

Hope this helps you get started, honey!

405 notes

·

View notes

Text

"Fuel your financial journey with the power of US stocks! 🚀 Don't just watch, be a part of the wealth revolution! 📈 Join my dynamic stock investment group, where opportunities ignite, insights flourish, and success awaits. Seize the moment, let's rewrite the story of your financial triumph together! 💪💼

#financial literacy#financialfreedom#finance#financial#economy#ecommerce#investors#investing#invest#stock market#stocks#stock#real estate#investor#self love#encouragement#encourage#selfworth#manifest#growth#grow#improvement#motivation#motivatedmindset#mindset#growthmindset#improve#quote#quotes#inspirational quotes

48 notes

·

View notes

Text

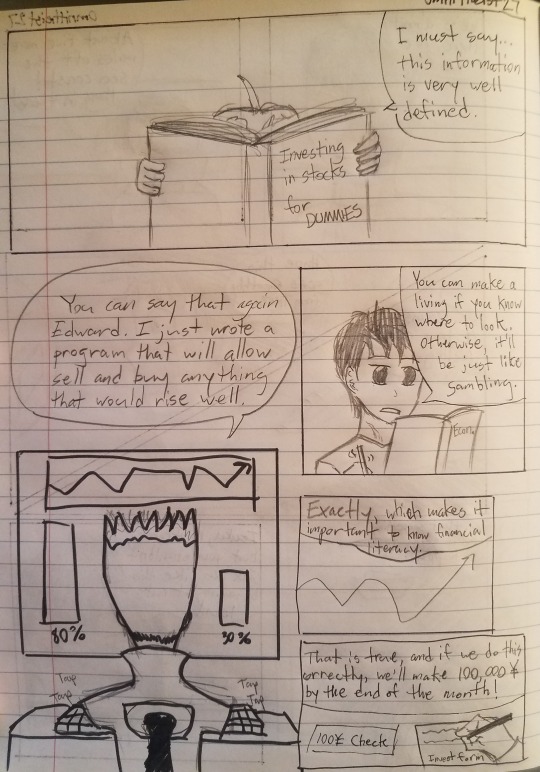

The 40 - A good investment

----

@the-ravenclaw-werewolf and @purplemochi20055

----

"An investment in knowledge pays the best interest." - Benjamin Franklin

----

I'm back again with another daily drabble of The 40. (Encouraging the completion of the final chapter of Main Character Syndrome (With Exceptions))

After going through some investments I made in Robinhood.com while trying to find a job, I decided to apply my woefully illiterate financial knowledge to the characters of The 40 by having an OC give them a challenge involving a loan of a ¥100 check.

The challenge? Use the ¥100 check and raise up to ¥100,000 in the stock trade by the end of the month.

Edward and Haruhi are woefully unknown to the Japanese stock trade, they are hitting up the books in the library regarding business and economics, and learning at a fast pace while simultaneously interested in the financial subjects. While Senku and Kobayashi started investing the ¥100 check into stocks.

To raise ¥100,000 in such a short time, the four members of The 40 traded like crazy. Many days went by as they loaded themselves with free caffeine to keep their eyes glued to the rise and fall of the stock trade, adding a certain level of stress.

To help ease things, Senku and Kobayashi both wrote their own computer programs using the library's computers that can track trends, analyze data, and automatically invest in something that would profit.

By the end of the month, the four of them managed to earn themselves good fortune that not only paying back the ¥100,000 and having a good amount of paper currency for themselves, but also gaining some great financial experience and literacy.

----

Speaking of money, I think it's a good time for me to start doing the "tipping" feature of Tumblr to earn some side income for my artwork.

Just click on the "tip" icon below for more of my drawings!

#the_40#fan comic#crossover#stock market#investing stocks#financial literacy#fullmetal alchemist#dr. stone#ouran high school host club#miss kobayashi's dragon maid#edward elric#ishigami senku#haruhi fujioka#kobayashi#daily encouragement#monetization

11 notes

·

View notes

Text

Time gone never returns.

#financial freedom#financial literacy#moneyquotes#personal finance#budgeting#finance#money mindset#money management#financial education#happylife#moneytips#financial independence#financial tips#financialfreedom

110 notes

·

View notes

Text

Hello friends! I'm curious about how many of us (Queer and Trans) individuals feel they are with their budgeting and financial literacy skills - please share the poll for larger reach!

I have a background in the accounting and finance world and have worked to improve my financial habits over years. I want to help others with things my brain understands pretty easily, so I would love to see if there are people who would be interested!

12 notes

·

View notes

Text

I'm not an influencer, not wealthy, and not USAmerican.

Nonetheless, here's my much better "Reset that Will Transform Your Life" tips than many I see from US-based influencers:

Simplify your financial scheme. Ensure that it accomplishes exactly what it needs to do - nothing less or more - and prioritize the stability and customer service quality of involved firms.

Prioritize becoming debt-free above all but living and employment necessity expenses.

Quality > Quantity in every regard.

Every default should be professional.

Tea, not coffee.

Force proper posture and movement, ergonomics if / when you're able.

Wait until your credit statement is generated to pay your dues - in full, as often as is possible. Maintain utilization rate below 30% and define an appropriate schedule upon which to apply for credit limit raises.

Women and girls pursuing higher education and strong careers in the United States, this primarily concerns you.

#women in tech#studyblr#studyspo#mine#financial literacy#anyone with ideas to persuade more women to enter tech business and policy please share ideas#the entry barrier (globally) is especially difficult for women and girls from backgrounds with low social capital

11 notes

·

View notes

Text

Why financial literacy education in the US sucks

youtube

#finances#economics#capitalism#budgeting#us history#cold war#home economics#schooling#education#literacy#financial literacy#Youtube

7 notes

·

View notes

Note

hii eve i’ve been loving all the fics lately! I was wondering if you could write something ab remus teaching regulus some financial literacy? like reg is in college and is trying to budget and remus helps him

This is SUCH an important step for so many college students and I'm really glad you asked this! Regulus and Remus bonding is something I'm really excited to see in the future. Character credit goes to @lumosinlove <3

TW taxes

“Hello?”

“Bon—uh, hi, Remus?”

It wasn’t like Remus hadn’t been expecting a call from Regulus when he went to college. In truth, he had been quite excited to see Sirius and Regulus navigate their weird pseudo-estranged, sibling-parent-child relationship and come out of it stronger and more secure. That growth and intentional distance would be good for them. He just wasn’t expecting Regulus to call him.

Oh, he thought, still holding the phone to his ear. Alright, then. “Uh, yeah, I’m here. Did you—are you okay?”

“Ouais, I’m good. College is—it’s good.”

Remus nodded slowly before remembering Regulus couldn’t see him. “Good. Good, I’m glad to hear it. Classes are going well?”

“Yeah, no, they’re…great.”

What the fuck, what the fuck, what the fuck—“Sirius is in the shower right now, sorry. I can let him know you called?”

“Ah.” A beat of uncomfortable silence crackled between them; it seemed even a couple hundred miles couldn’t stop Remus from making a fool of himself around Regulus Black. Somehow, he always managed to stick his foot in his mouth when they spoke for more than ten minutes at a time. Regulus cleared his throat. “Uh, well, I wanted to talk to you, actually.”

Remus went cold. “Oh my god, are you okay?”

“Should I buy a car?”

The adrenaline kicking in his stomach quieted. He could hear the faint sound of shuffling feet, like Regulus was pacing around his dorm. Remus paused, then shook himself from his stupor and leaned against the kitchen counter. “Why the hell would you do that?”

“So…no?”

“In Manhattan?” A laugh escaped before he could bring it back down to the line of distant friendliness he and Regulus toed on a regular basis, and he shook his head. “Yeah, that wouldn’t be a great investment. They’re expensive, they take up space, and you’d never use it.”

“D’accord.” Relief clung to every syllable and Remus heard him exhale softly. He could picture Regulus running a hand through his hair clear as day. “Great, merci.”

“Why were you going to buy a car?”

“It—honestly, I don’t know,” Regulus half-laughed. There was a creak, as if he had settled down at his desk or on his bed. “It seemed like the right thing to do, I guess.”

Remus blinked. “Reg, you live in New York.”

“People have cars here. I see them every day.”

“I—” He tilted the phone away so Regulus wouldn’t hear his sigh. “Okay, college students in New York don’t have cars unless they drive home, like, every weekend. What would you use it for, anyway?”

A long stretch of quiet followed and Remus bit the inside of his cheek. “…going…places?”

“I can guarantee you’ll get there faster on the subway.” And it’ll be cheaper, he added silently. Not that money was an issue for Regulus, though that brought a new question to mind. “Hey, by the way, and you can totally tell me to fuck off here: how’s your budget look this year? Sirius mentioned something about your contract getting cut. You don’t have to tell me, but I know he was worried.”

“My budget?” More silence followed. “Yeah, I’m all set.”

Remus knew he should let it lie. He knew he should say a cordial goodbye and leave the real conversations to someone Regulus trusted further than he could chuck him. But the voice at the back of his head that sounded suspiciously like his mother couldn’t let curiosity go unanswered, and he blurted, “you do have a budget, don’t you?” before he could stop himself.

“Yes,” Regulus scoffed, as good of a liar as his brother.

Oh my god, you’ve never had to do that in your entire life. Sudden visions of Sirius’ general obliviousness to the cost of groceries, bedsheets, and everything that cost less than four digits rose to his mind and he covered his mouth for a moment, letting the initial shock run its course. It wasn’t Regulus’ fault in the same way Sirius couldn’t be blamed too much for simply not understanding the value of a dollar. Living on a budget was, quite literally, not even in their universe for the first 18 years of their lives.

“Okay,” Remus said after a few charged seconds, making his way to the kitchen table where his laptop was still open. Not how I planned on spending my Saturday, but someone’s got to do it. “Alright. You got half an hour to spare?”

The mattress creaked. Regulus sighed. “Yeah.”

“You got a computer?”

“In my lap.”

“Great. First step: open up Excel.”

--

The last thing Sirius expected when he came downstairs was to find his boyfriend at the table with a spreadsheet open and his attention fully tuned to the phone. “Hey, no, you’re doing awesome,” Remus soothed. “This is tough the first time.”

He frowned. That was a tone generally reserved for Jules or, on rare occasions, a panicking teammate. He padded down the hall and draped his arms over Remus’ shoulders with a kiss to the top of his head; Remus leaned back into him with a long exhale, then tilted the phone up until the screen brightened.

Caller: Regulus Black

Duration: 45:23

Alarm jolted in Sirius’ stomach and must have shown on his face, because Remus reached up to cup in his cheek in one palm with an encouraging smile. It’s okay, he mouthed, then leaned up for a chaste, upside-down kiss. “Yeah, Reg, I’m still here,” he said as he settled back into the chair, hand coming down to rest on Sirius’ wrist. “Your brother says hi. No, we’re not making out while you’re working on this, I promise.”

Sirius rolled the soft fabric of Remus’ sweater between his fingertips while he scanned the spreadsheet. Regulus Monthly had been typed neatly at the top, followed by several categories of varying mundanity. There was a Total section at the bottom corner, and dollar amounts in each corresponding cell… “Are you budgeting?”

Remus made a shushing motion, but nodded.

“Why are you budgeting with my baby brother?” That got him an eye roll and Sirius huffed, reaching to unplug Remus’ earbuds from his phone.

“—and because of that I’m not super worried about—”

“Why are you making Remus do a budget for you?” he interrupted.

“Sirius!”

“I’m not!” Regulus protested at the same time. “He offered!”

He was well aware that Regulus couldn’t see him through the phone, but that didn’t stop him from gaping. “You haven’t had a budget this whole time?”

“I didn’t think I needed one!”

“Your contract got cut in half, idiot!” And mom and dad aren’t going to pay your bills after everything we’ve done.

Remus was still glowering at him a little. “Cut it out, he’s doing really well,” he repeated before facing the phone again. “Anyway, Reg, that sounds like a good plan for now. Though I still think reaching out to Logan would be smart.”

“Why Logan?” Sirius was sure he had never been more thoroughly baffled in his entire life.

He could feel Remus’ physical exasperation under his hands. “Who else do you know that has lived in Canada and the U.S., done taxes for both, and has a Harvard business degree, baby?”

Fair point. Sirius bit back the admission and rested his chin on top of Remus’ head instead. “You’re making Reg do most of the work, right?”

“He’s done it all himself so far.” Remus sounded so proud; it was funny to hear that after the months of tentative friendship they had managed before Regulus moved out. Then again, Sirius figured he had been a bit too preoccupied with scraping together the remnants of their childhood bond to notice any excess awkwardness between his boyfriend and his brother. It certainly couldn’t have been easy for them. He had years of knowing Regulus at his truest self, but Remus only knew the worst.

“This looks fantastic,” he said. “Nice job, Reg.”

The hand on his wrist gave a light squeeze. “Merci,” Regulus answered. His voice was tinny over the phone, but Sirius could still hear the spark of excitement. “I’m lucky to have Remus helping me.”

“Aren’t we all.” He buried his nose in caramel curls and closed his eyes, lacing their fingers together. Thank you, he thought fervently. Thank you, thank you, I love you.

Remus tilted his head enough to rest it against Sirius’ shoulder. “We’re just wrapping up here,” he said. “We can go for a walk if you want to grab Hattie’s harness?”

“Comme tu veux, mon loup.” He bumped his nose against Remus’ temple once before turning to the phone. “Have fun, Reg. À plus tard, call if you need anything.”

“Your boyfriend knows more than you do,” Regulus snorted. “I’ll be calling him.”

“Steal him away from me and I’ll flay you!” Sirius called over his shoulder as he headed out of the kitchen. A walk sounded nice; it was overcast, not too snowy and not too bright. Maybe they could coax Hattie into wearing her booties for the ice.

“Okay,” Remus said, dragging the word out. “No flaying until you figure out transportation costs. Where were we?”

#remus lupin#regulus black#sirius black#coops#sweater weather#vaincre#lumosinlove#my fic#fanfic#financial literacy#bonding#college reg#budgeting

194 notes

·

View notes

Text

Make the money work

don’t leave it in a savings account

#art#generationalwealth#mansorus#mental health awareness#philly#financial literacy#finacialfreedom#cash#cash out

38 notes

·

View notes

Text

{ MASTERPOST } Everything You Need to Know about Repairing Our Busted-Ass World

On poverty:

Starting from nothing

How To Start at Rock Bottom: Welfare Programs and the Social Safety Net

How to Save for Retirement When You Make Less Than $30,000 a Year

Ask the Bitches: “Is It Too Late to Get My Financial Shit Together?“

Understanding why people are poor

It’s More Expensive to Be Poor Than to Be Rich

Why Are Poor People Poor and Rich People Rich?

On Financial Discipline, Generational Poverty, and Marshmallows

Bitchtastic Book Review: Hand to Mouth by Linda Tirado

Is Gentrification Just Artisanal, Small-Batch Displacement of the Poor?

Coronavirus Reveals America’s Pre-existing Conditions, Part 1: Healthcare, Housing, and Labor Rights

Developing compassion for poor people

The Latte Factor, Poor Shaming, and Economic Compassion

Ask the Bitches: “How Do I Stop Myself from Judging Homeless People?“

The Subjectivity of Wealth, Or: Don’t Tell Me What’s Expensive

A Little Princess: Intersectional Feminist Masterpiece?

If You Can’t Afford to Tip 20%, You Can’t Afford to Dine Out

Correcting income inequality

1 Easy Way All Allies Can Help Close the Gender and Racial Pay Gap

One Reason Women Make Less Money? They’re Afraid of Being Raped and Killed.

Raising the Minimum Wage Would Make All Our Lives Better

Are Unions Good or Bad?

On intersectional social issues:

Reproductive rights

On Pulling Weeds and Fighting Back: How (and Why) to Protect Abortion Rights

How To Get an Abortion

Blood Money: Menstrual Products for Surviving Your Period While Poor

You Don’t Have to Have Kids

Gender equality

1 Easy Way All Allies Can Help Close the Gender and Racial Pay Gap

The Pink Tax, Or: How I Learned to Love Smelling Like “Bearglove”

Our Single Best Piece of Advice for Women (and Men) on International Women’s Day

Bitchtastic Book Review: The Feminist Financial Handbook by Brynne Conroy

Sexual Harassment: How to Identify and Fight It in the Workplace

Queer issues

Queer Finance 101: Ten Ways That Sexual and Gender Identity Affect Finances

Leaving Home before 18: A Practical Guide for Cast-Offs, Runaways, and Everybody in Between

Racial justice

The Financial Advantages of Being White

Woke at Work: How to Inject Your Values into Your Boring, Lame-Ass Job

The New Jim Crow, by Michelle Alexander: A Bitchtastic Book Review

Something Is Wrong in Personal Finance. Here’s How To Make It More Inclusive.

The Biggest Threat to Black Wealth Is White Terrorism

Coronavirus Reveals America’s Pre-existing Conditions, Part 2: Racial and Gender Inequality

10 Rad Black Money Experts to Follow Right the Hell Now

Youth issues

What We Talk About When We Talk About Student Loans

The Ugly Truth About Unpaid Internships

Ask the Bitches: “I Just Turned 18 and My Parents Are Kicking Me Out. How Do I Brace Myself?”

Identifying and combatting abuse

When Money is the Weapon: Understanding Intimate Partner Financial Abuse

Are You Working on the Next Fyre Festival?: Identifying a Toxic Workplace

Ask the Bitches: “How Do I Say ‘No’ When a Loved One Asks for Money… Again?”

Ask the Bitches: I Was Guilted Into Caring for a Sick, Abusive Parent. Now What?

On mental health:

Understanding mental health issues

How Mental Health Affects Your Finances

Stop Recommending Therapy Like It’s a Magic Bean That’ll Grow Me a Beanstalk to Neurotypicaltown

Bitchtastic Book Review: Kurt Vonnegut’s Galapagos and Your Big Brain

Ask the Bitches: “How Do I Protect My Own Mental Health While Still Helping Others?”

Coping with mental health issues

{ MASTERPOST } Everything You Need to Know about Self-Care

My 25 Secrets to Successfully Working from Home with ADHD

Our Master List of 100% Free Mental Health Self-Care Tactics

On saving the planet:

Changing the system

Don’t Boo, Vote: If You Don’t Vote, No One Can Hear You Scream

Ethical Consumption: How to Pollute the Planet and Exploit Labor Slightly Less

The Anti-Consumerist Gift Guide: I Have No Gift to Bring, Pa Rum Pa Pum Pum

Season 1, Episode 4: “Capitalism Is Working for Me. So How Could I Hate It?”

Coronavirus Reveals America’s Pre-existing Conditions, Part 1: Healthcare, Housing, and Labor Rights

Coronavirus Reveals America’s Pre-existing Conditions, Part 2: Racial and Gender Inequality

Shopping smarter

You Deserve Cheap Toilet Paper, You Beautiful Fucking Moon Goddess

You Are above Bottled Water, You Elegant Land Mermaid

Fast Fashion: Why It’s Fucking up the World and How To Avoid It

You Deserve Cheap, Fake Jewelry… Just Like Coco Chanel

6 Proven Tactics for Avoiding Emotional Impulse Spending

Join the Bitches on Patreon

#poverty#economics#income inequality#wealth inequality#capitalism#working class#labor rights#workers rights#frugal#personal finance#financial literacy#consumerism#environmentalism

82 notes

·

View notes

Text

we ain’t just teaching our shorty metaphysics, ancient history etc..

we teaching Her financial literacy and how to invest and make money in the market.

21 notes

·

View notes

Text

“Each one of your expenses is someone else’s income, and each one of your liabilities is someone else’s asset. Every time you spend money, you are adding to someone else’s income instead of augmenting your own” - Robert T. Kiyosaki

#financial literacy#financialfreedom#finance#financial#economy#ecommerce#investors#investing#invest#stock market#stocks#stock#real estate#investor#self love#encouragement#encourage#selfworth#manifest#growth#grow#improvement#motivation#motivatedmindset#mindset#growthmindset#improve#quote#quotes#inspirational quotes

90 notes

·

View notes

Text

7 Success Sabotaging Habits You Need to Ditch

Written by Delvin

Success is often hindered by self-sabotaging habits that we may not even be aware of. In this post, we’ll explore seven common habits that can derail your path to success and provide strategies to overcome them.

1. Procrastination: Putting off important tasks can prevent you from reaching your goals. Combat procrastination by breaking tasks into smaller, manageable steps and…

View On WordPress

#Breaking Bad Habits#dailyprompt#Financial#Financial Education#Financial Literacy#knowledge#money#Money Habits#Personal Development#Personal Finance#Success Habits

3 notes

·

View notes

Last Seen Blogs

knowlesdavis83

The Love of Miles 333

nann-the-explorer

Follow curiosity, seek knowledge, find wisdom

greysmobility

Untitled

gardenkeeper

The garden of the gods is flowering

jiminnieeeee

우린 달의 아이